|

|

|

|

|||||

|

|

|

The 2025 Q4 earnings season is pretty much over following the highly-awaited NVIDIA release. The period has so far been positive, with growth remaining strong and a solid number of companies exceeding quarterly expectations.

Concerning some big winners of the cycle so far, Boot Barn BOOT, Palantir PLTR, and Cardinal Health CAH all posted robust results.

Boot Barn had a rock-solid release, with sales climbing 16% year-over-year alongside a 5.7% charge higher in same store sales. The same store sales growth is particularly notable, telling us that its existing stores are seeing strong performance while it also continues to open new locations.

Concerning store openings, the company opened 25 new locations throughout the period, bringing its overall tally up to 514 at the quarter's end.

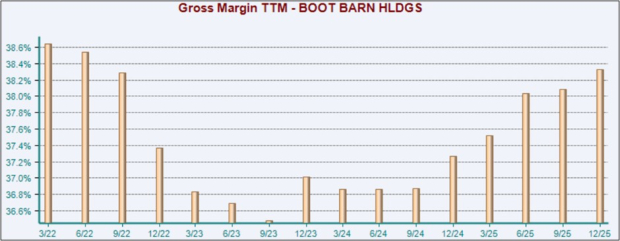

BOOT also enjoyed an improved profitability picture, with its gross margin growing to 39.9% vs. a 39.3% print in the same period last year. Consumer-focused stocks, particularly retail, are often highly sensitive to margin performance, helping explain the strong post-earnings reaction and guide higher.

BOOT’s margins picture has remained positive for several periods now, seeing nice expansion off 2023 lows. Please note that the chart below is on a trailing twelve-month basis.

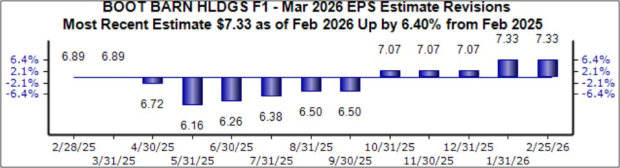

And to top it off, the stock sports the highly-coveted Zacks Rank #1 (Strong Buy), with EPS expectations notably bullish for the above-mentioned FY26.

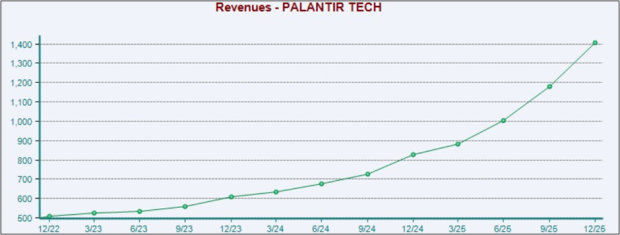

Palantir again continued to fire on all cylinders throughout the period, with overall sales of $1.4 billion flying 70% year-over-year. U.S. results were rock-solid again, underpinned by both commercial and government strength. Specifically, U.S. sales totaled $1.1 billion, growing 93% year-over-year and an even more impressive 28% sequentially.

Further, Palantir closed more than $4.2 billion of total contract value (TCV) overall, up more than 130% from the year-ago period. And its consumer base keeps snowballing, with customer count surging 34% from the year-ago period.

Below is a chart illustrating the company’s sales on a quarterly basis.

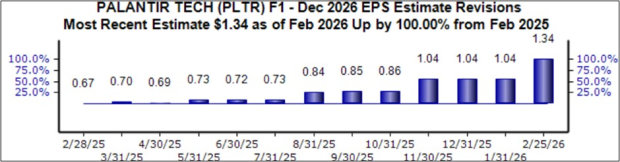

While price action hasn’t been ideal, the company’s current fiscal year EPS outlook remains very bullish, as shown below. The stock sports a Zacks Rank #2 (Buy).

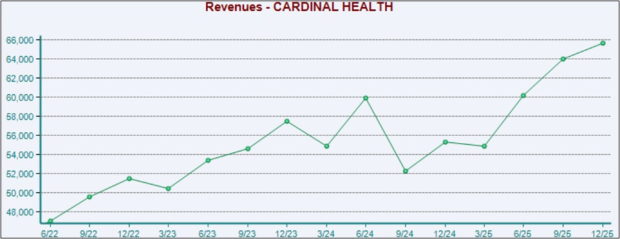

Cardinal Health posted a double-beat relative to our consensus expectations, with sales soaring 18.8% from the year-ago period alongside a sizable 36.3% year-over-year growth rate in adjusted EPS.

Cardinal Health’s sales have seen great growth over recent periods after some stagnation throughout 2024, as shown below in the chart that illustrates CAH’s sales on a quarterly basis.

Strength was primarily broad-based across its segments, with sales in Pharmaceuticals and Specialty Solutions climbing 19% year-over-year. It’s worth noting that its Pharmaceuticals and Specialty Solutions accounts for the vast majority of its sales, contributing roughly 90%.

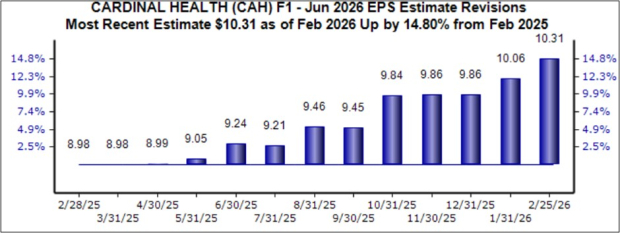

Cardinal Health raised its FY26 outlook following the strong quarter, now expecting adjusted EPS in a band of $10.15 - $10.35, with the midpoint suggesting 24.5% year-over-year growth. The updated outlook is reflected in positive earnings estimate revisions for its current fiscal year, as shown below. The stock sports a favorable Zacks Rank #2 (Buy).

Putting Everything Together

All three stocks above – Boot Barn BOOT, Palantir PLTR, and Cardinal Health CAH – posted robust quarterly results this earnings cycle while simultaneously sporting favorable Zacks Ranks.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-09 | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Nvidia Earnings: Turn A $265 Profit Trading Around The AI Chipmaker's Report

PLTR +10.32%

Investor's Business Daily

|

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite