|

|

|

|

|||||

|

|

|

Sensata Technologies has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 11.6% to $37.41 per share while the index has gained 7.2%.

Is now the time to buy Sensata Technologies, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

We don't have much confidence in Sensata Technologies. Here are three reasons you should be careful with ST and a stock we'd rather own.

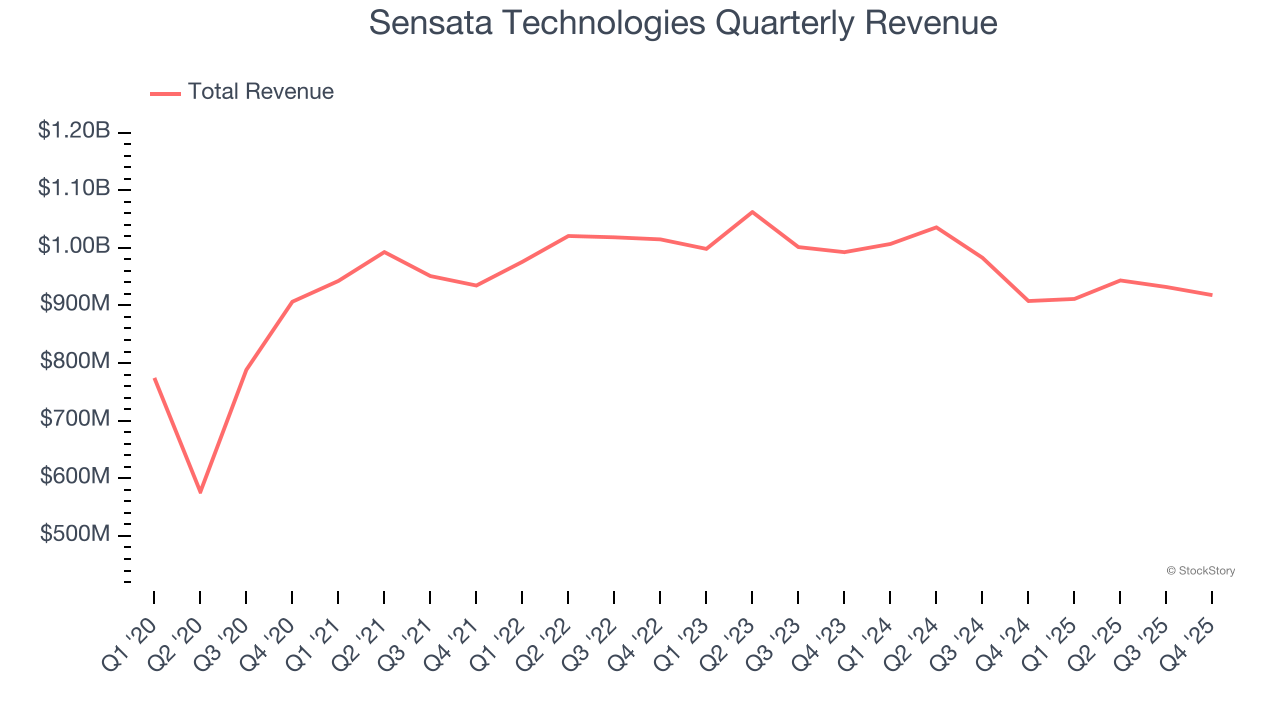

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Sensata Technologies grew its sales at a mediocre 4% compounded annual growth rate. This was below our standard for the semiconductor sector. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Sensata Technologies’s revenue to rise by 2.9%. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below the sector average.

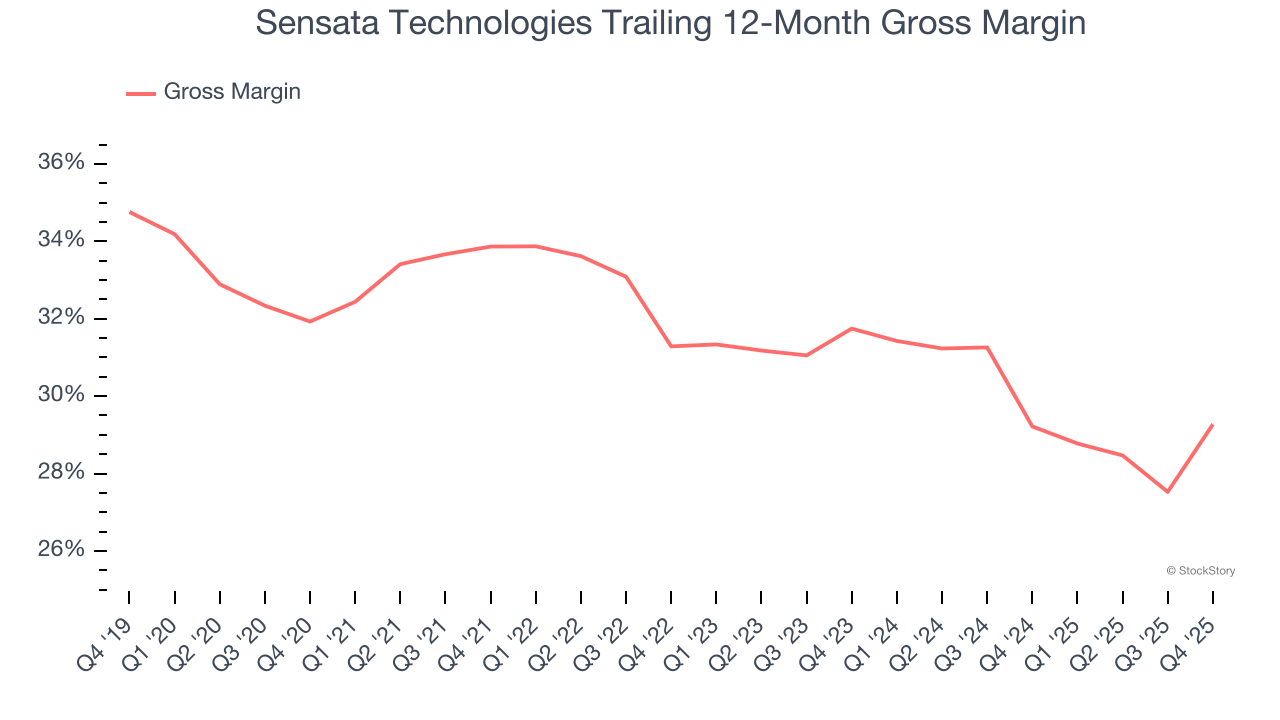

In the semiconductor industry, a company’s gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Sensata Technologies’s gross margin is one of the worst in the semiconductor industry, signaling it operates in a competitive market and lacks pricing power. As you can see below, it averaged a 29.2% gross margin over the last two years. Said differently, Sensata Technologies had to pay a chunky $70.76 to its suppliers for every $100 in revenue.

We cheer for all companies solving complex technology issues, but in the case of Sensata Technologies, we’ll be cheering from the sidelines. That said, the stock currently trades at 10.4× forward P/E (or $37.41 per share). This multiple tells us a lot of good news is priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at the most entrenched endpoint security platform on the market.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jun-30 | |

| Jun-25 | |

| Jun-01 | |

| May-29 | |

| May-21 | |

| May-15 | |

| May-13 | |

| Apr-29 | |

| Apr-29 | |

| Apr-28 | |

| Apr-28 | |

| Apr-14 | |

| Mar-22 | |

| Mar-08 | |

| Mar-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite