|

|

|

|

|||||

|

|

|

Chewy’s stock price has taken a beating over the past six months, shedding 33.2% of its value and falling to $27.03 per share. This might have investors contemplating their next move.

Is now the time to buy Chewy, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Even with the cheaper entry price, we're swiping left on Chewy for now. Here are three reasons we avoid CHWY and a stock we'd rather own.

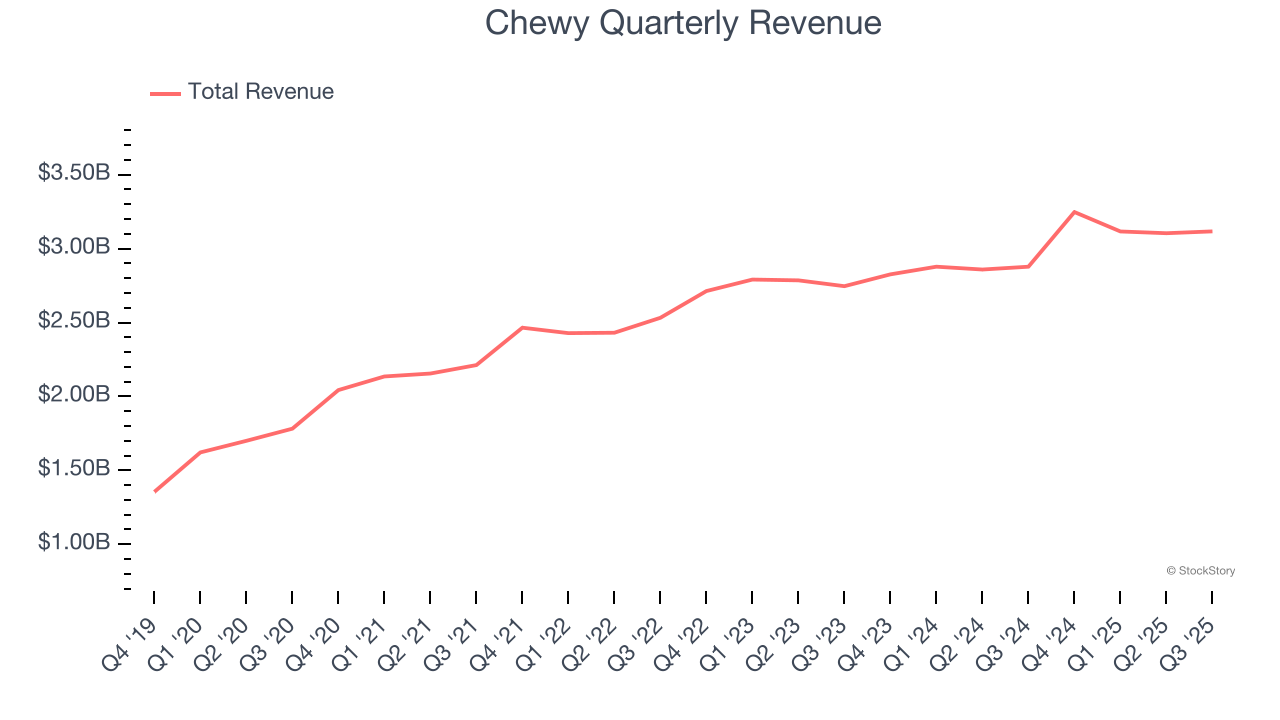

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Chewy’s 8.5% annualized revenue growth over the last three years was mediocre. This was below our standard for the consumer internet sector.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Chewy’s revenue to rise by 6.1%, a slight deceleration. This projection doesn't excite us and implies its products and services will see some demand headwinds.

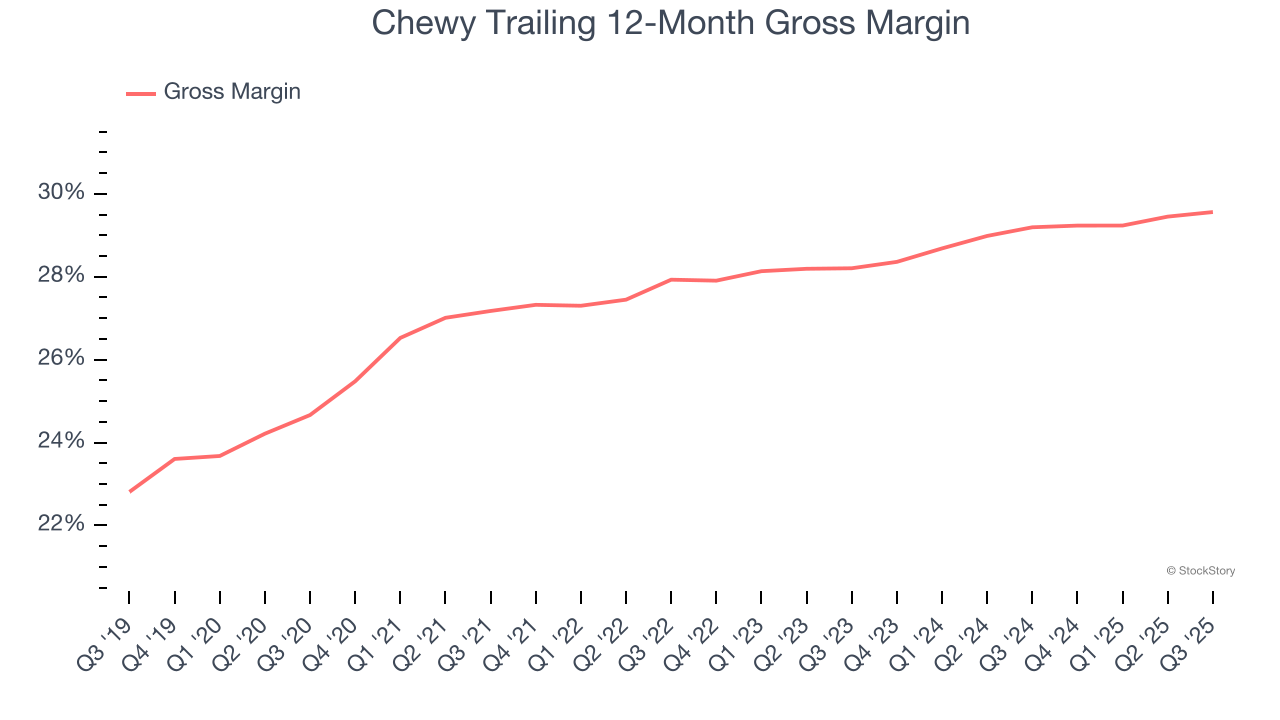

For online retail (separate from online marketplaces) businesses like Chewy, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include the cost of acquiring the products sold, shipping and fulfillment, customer service, and digital infrastructure.

Chewy’s unit economics are far below other consumer internet companies because it must carry inventories as an online retailer. This means it has relatively higher capital intensity than a pure software business like Meta or Airbnb and signals it operates in a competitive market. As you can see below, it averaged a 29.4% gross margin over the last two years. Said differently, Chewy had to pay a chunky $70.61 to its service providers for every $100 in revenue.

Chewy’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 13.2× forward EV/EBITDA (or $27.03 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at an all-weather company that owns household favorite Taco Bell.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-22 | |

| Jun-14 | |

| Jun-12 | |

| Jun-12 | |

| Jun-11 | |

| Jun-11 | |

| Jun-11 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 | |

| Jun-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite