|

|

|

|

|||||

|

|

|

Since February 2021, the S&P 500 has delivered a total return of 77.9%. But one standout stock has nearly doubled the market - over the past five years, Rush Enterprises has surged 149% to $71.67 per share. Its momentum hasn’t stopped as it’s also gained 22.2% in the last six months thanks to its solid quarterly results, beating the S&P by 15%.

Is now the time to buy Rush Enterprises, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

We’re glad investors have benefited from the price increase, but we don't have much confidence in Rush Enterprises. Here are three reasons we avoid RUSHA and a stock we'd rather own.

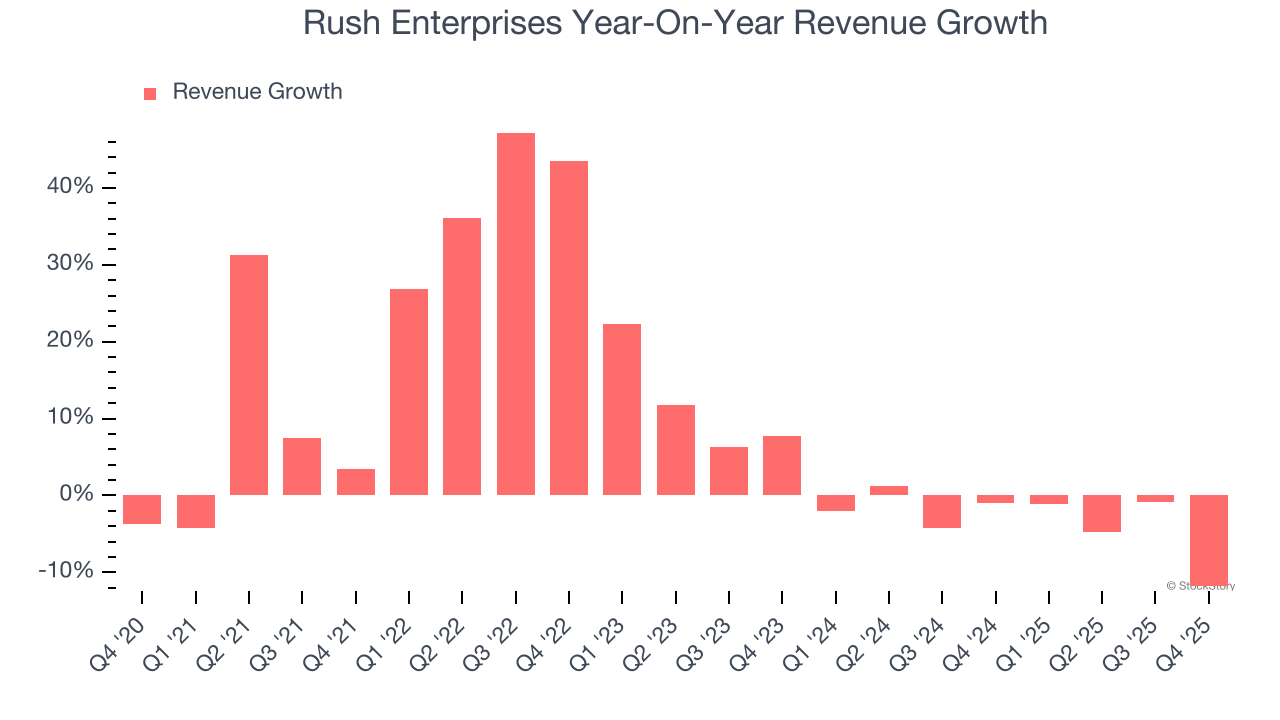

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Rush Enterprises’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 3.1% over the last two years.

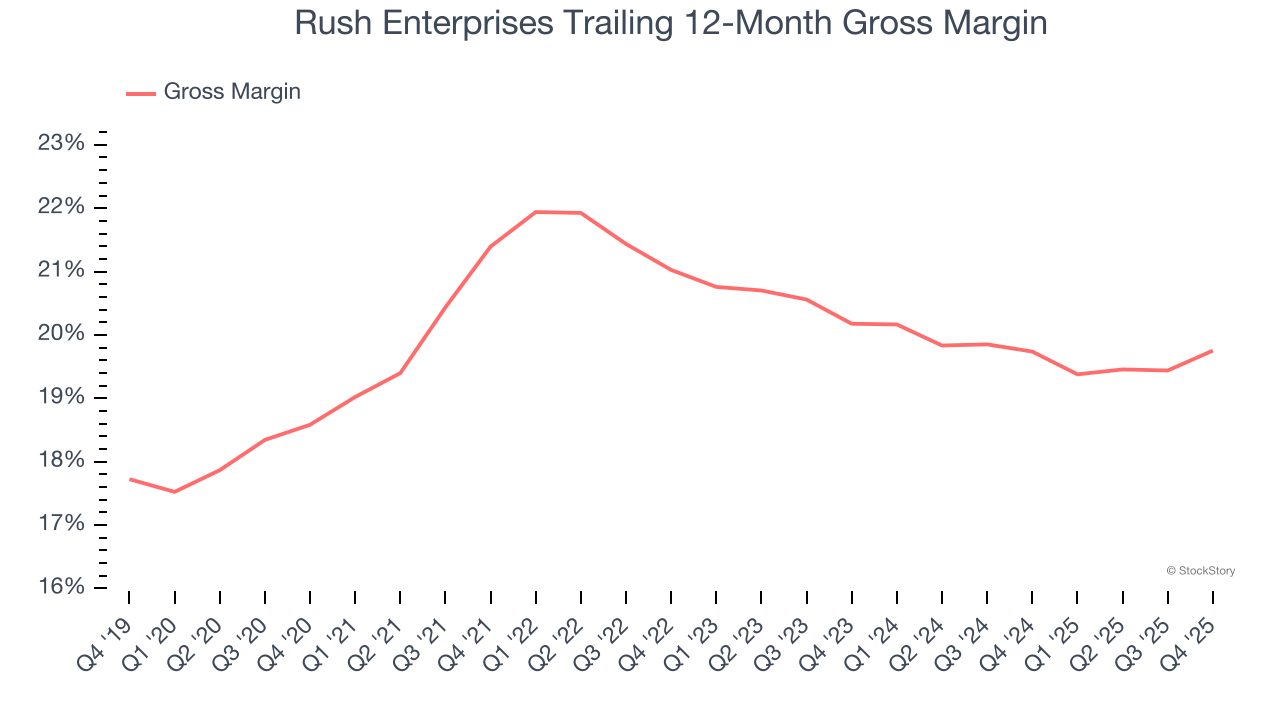

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

Rush Enterprises has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 20.3% gross margin over the last five years. Said differently, Rush Enterprises had to pay a chunky $79.66 to its suppliers for every $100 in revenue.

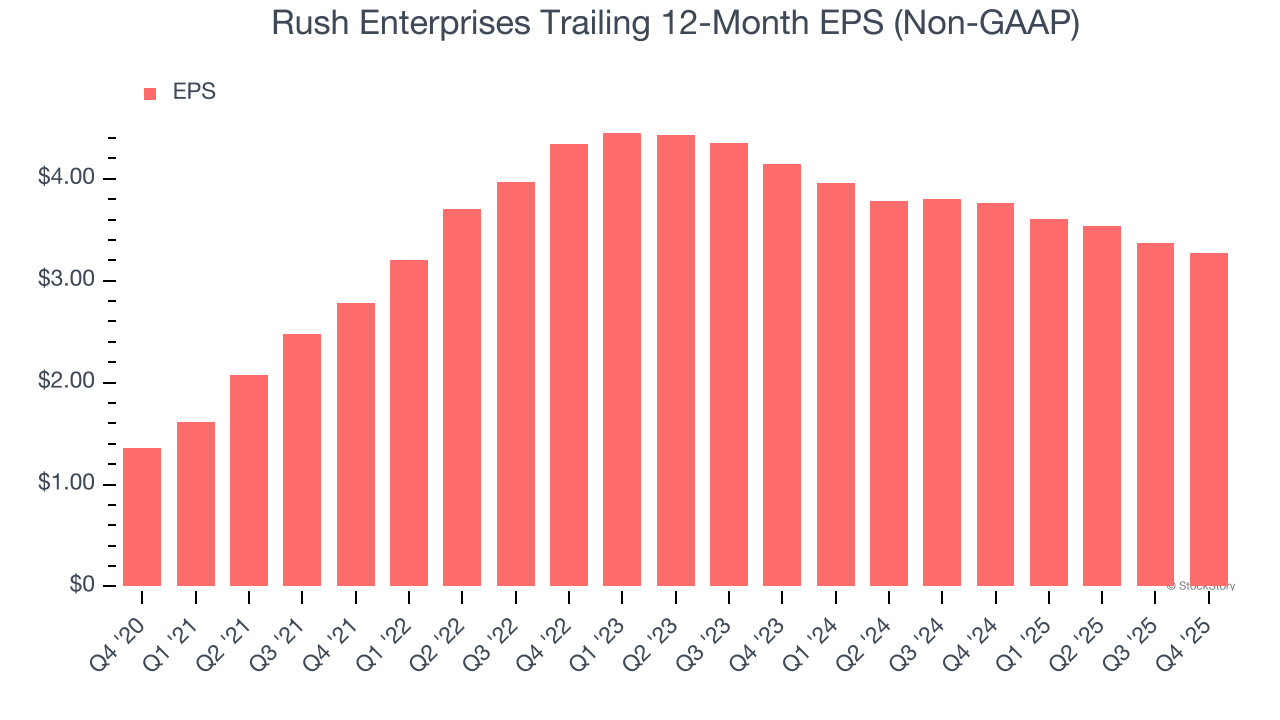

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Rush Enterprises, its EPS declined by more than its revenue over the last two years, dropping 11.1%. This tells us the company struggled to adjust to shrinking demand.

We cheer for all companies making their customers lives easier, but in the case of Rush Enterprises, we’ll be cheering from the sidelines. With its shares beating the market recently, the stock trades at 19.5× forward P/E (or $71.67 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better stocks to buy right now. Let us point you toward one of our top software and edge computing picks.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-02 | |

| Jun-30 | |

| Apr-30 | |

| Apr-28 | |

| Apr-28 | |

| Apr-02 | |

| Mar-23 | |

| Feb-26 | |

| Feb-24 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite