|

|

|

|

|||||

|

|

|

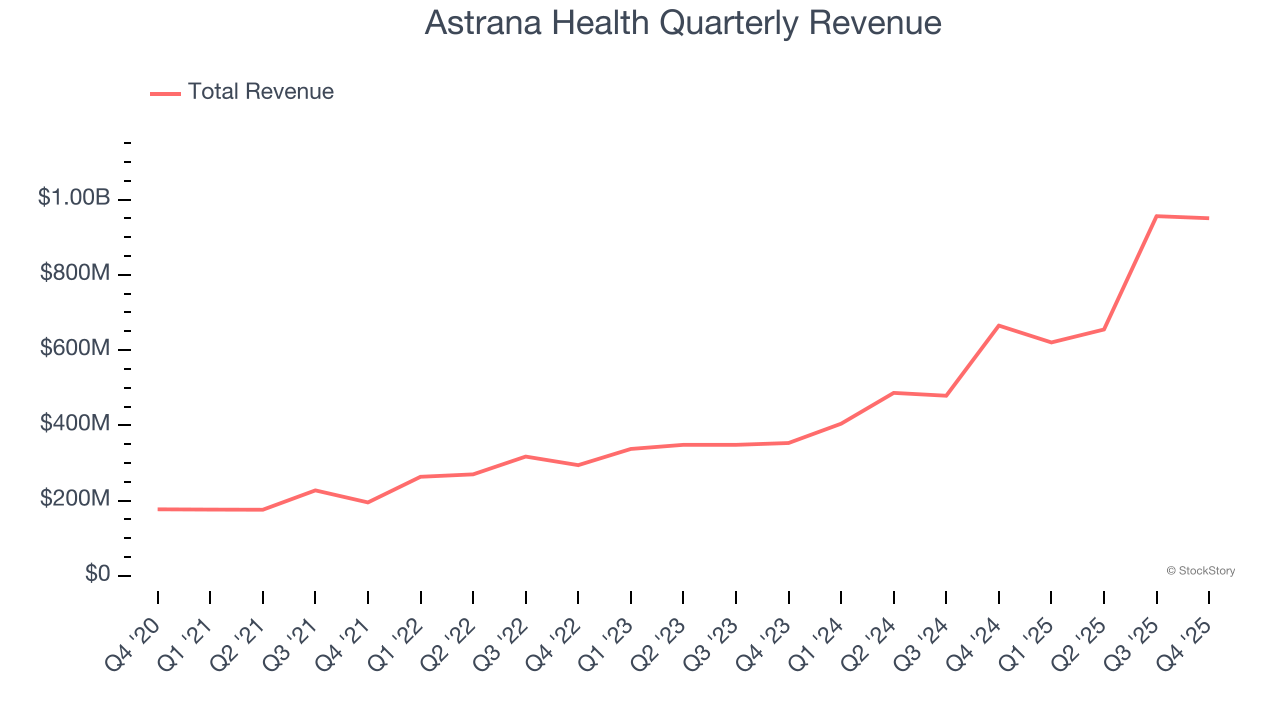

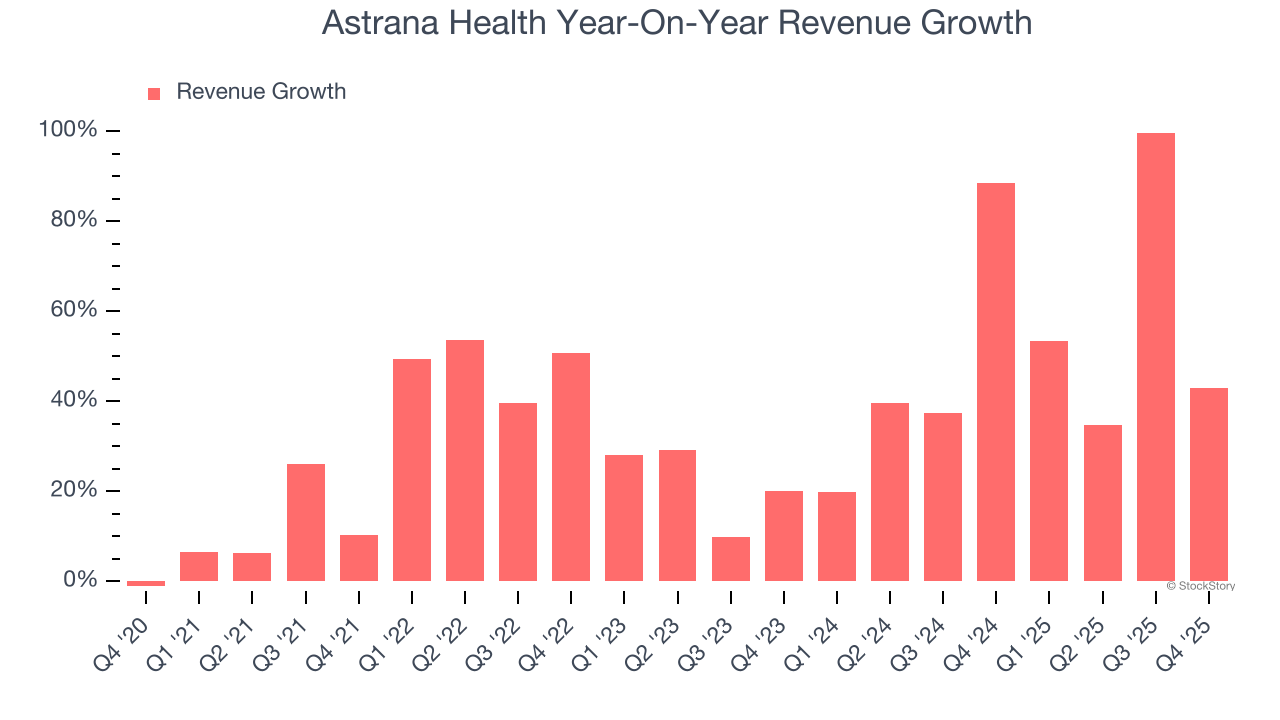

Healthcare services company Astrana Health reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 42.9% year on year to $950.5 million. The company expects next quarter’s revenue to be around $950 million, close to analysts’ estimates. Its GAAP profit of $0.12 per share was in line with analysts’ consensus estimates.

Is now the time to buy Astrana Health? Find out by accessing our full research report, it’s free.

"Astrana delivered record revenue, adjusted EBITDA, and free cash flow in 2025, demonstrating the strength and predictability of our fully delegated, payer-agnostic care model and AI-enabled technology platform in a dynamic operating environment," said Brandon Sim, President and Chief Executive Officer of Astrana Health.

Formerly known as Apollo Medical Holdings until early 2024, Astrana Health (NASDAQ:ASTH) operates a technology-powered healthcare platform that enables physicians to deliver coordinated care while successfully participating in value-based payment models.

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Astrana Health grew its sales at an incredible 35.9% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Astrana Health’s annualized revenue growth of 51.5% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Astrana Health reported magnificent year-on-year revenue growth of 42.9%, and its $950.5 million of revenue beat Wall Street’s estimates by 2.3%. Company management is currently guiding for a 53.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 24.5% over the next 12 months, a deceleration versus the last two years. Still, this projection is healthy and implies the market is forecasting success for its products and services.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

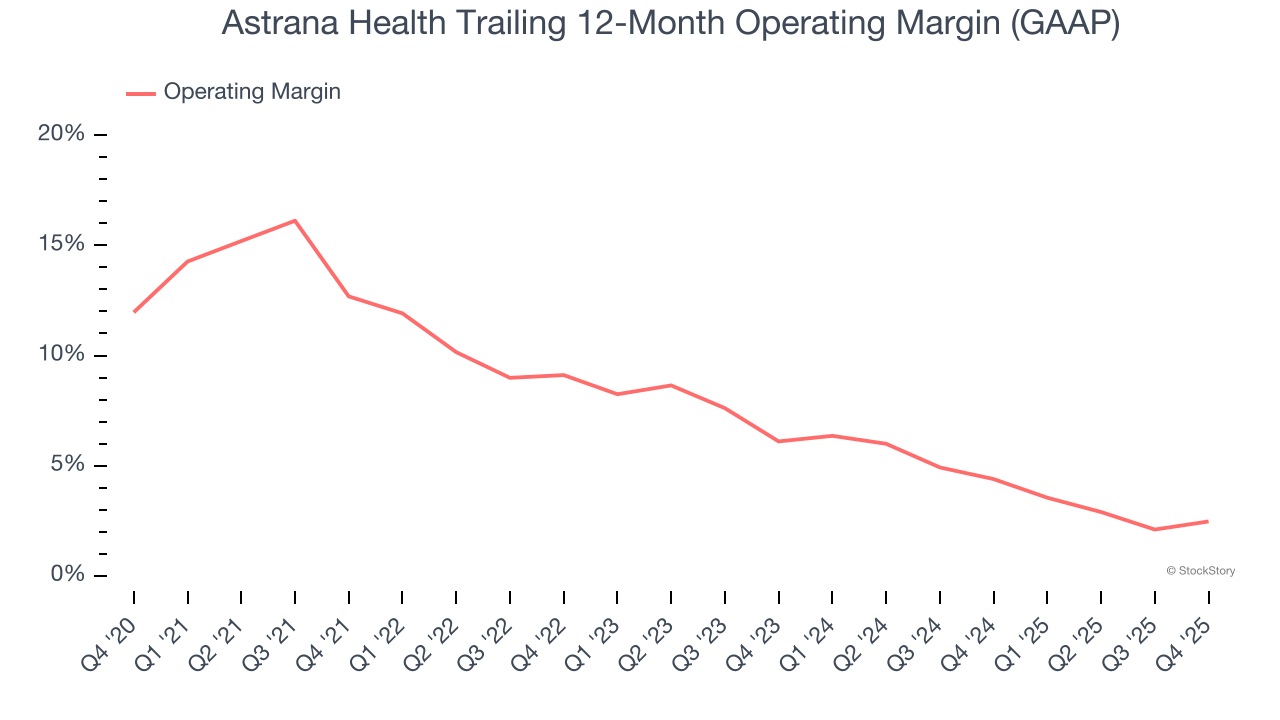

Astrana Health was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.3% was weak for a healthcare business.

Looking at the trend in its profitability, Astrana Health’s operating margin decreased by 10.2 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 3.6 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Astrana Health generated an operating margin profit margin of 1.9%, up 1.8 percentage points year on year. This increase was a welcome development and shows it was more efficient.

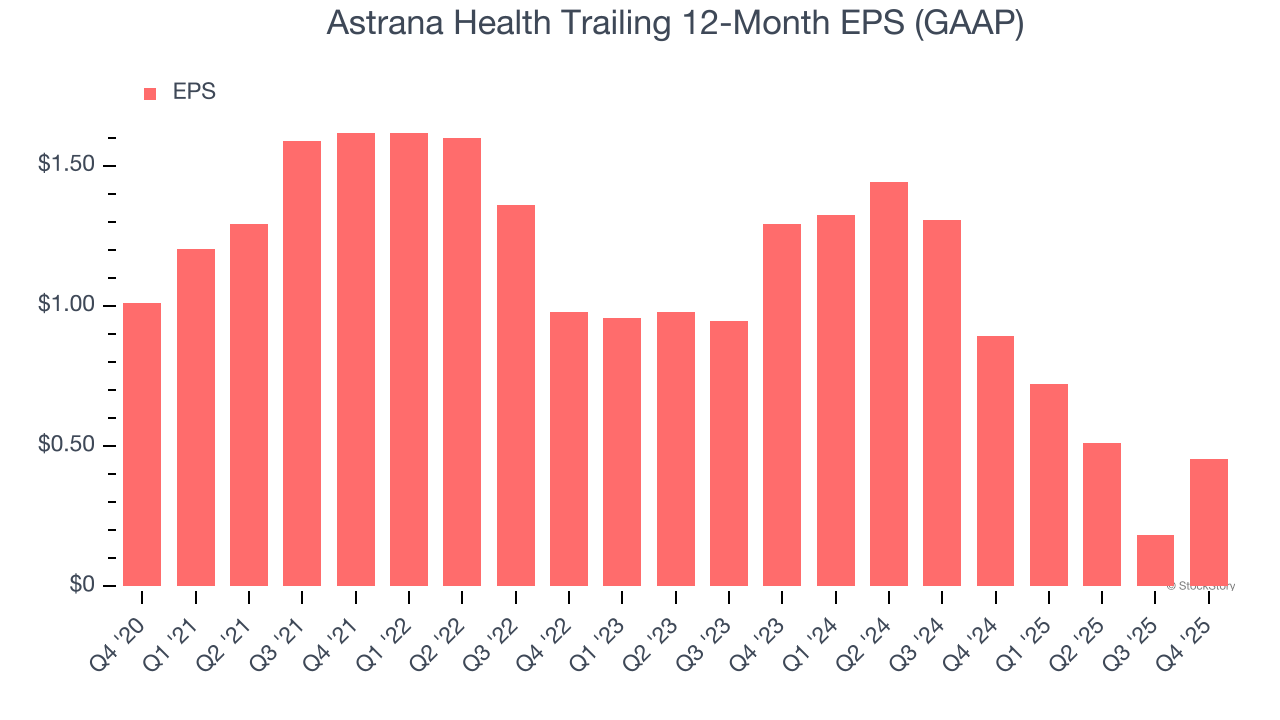

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Astrana Health, its EPS declined by 14.7% annually over the last five years while its revenue grew by 35.9%. This tells us the company became less profitable on a per-share basis as it expanded.

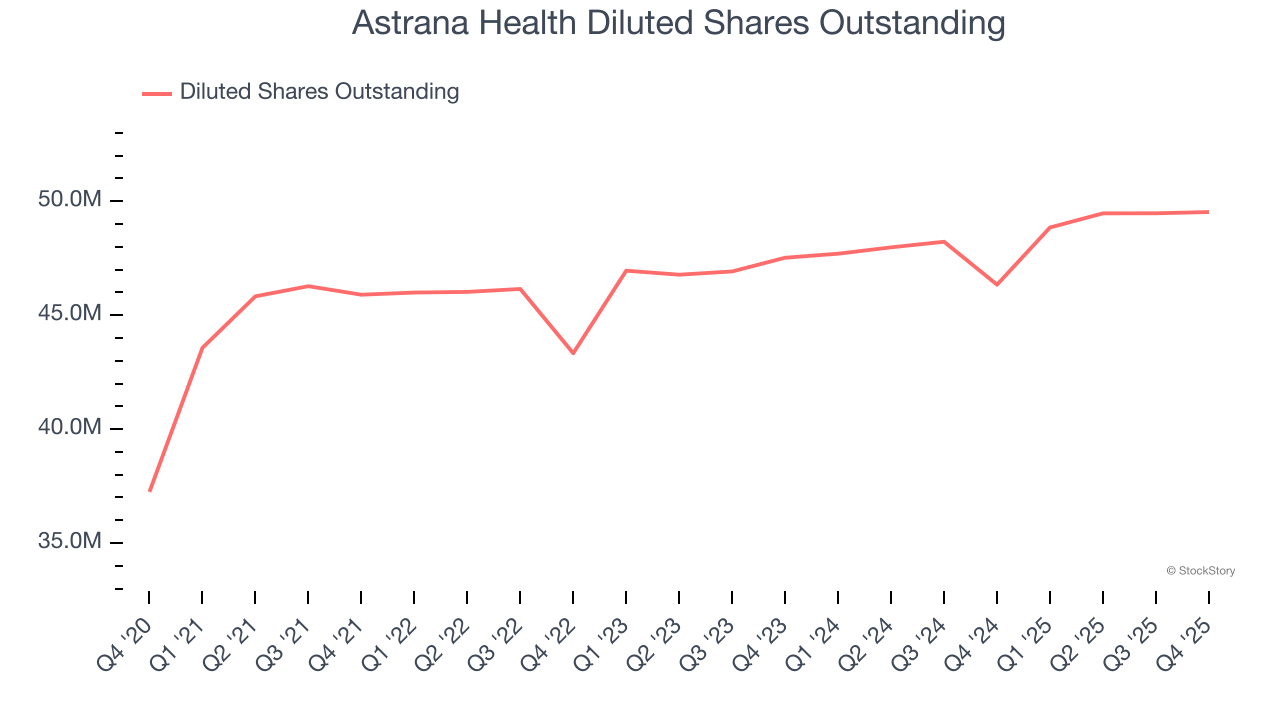

Diving into the nuances of Astrana Health’s earnings can give us a better understanding of its performance. As we mentioned earlier, Astrana Health’s operating margin expanded this quarter but declined by 10.2 percentage points over the last five years. Its share count also grew by 33%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, Astrana Health reported EPS of $0.12, up from negative $0.15 in the same quarter last year. This print beat analysts’ estimates by 3.8%. Over the next 12 months, Wall Street expects Astrana Health’s full-year EPS of $0.46 to grow 117%.

We were impressed by Astrana Health’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter was in line. Overall, this print had some key positives. The stock traded up 3.9% to $21.13 immediately following the results.

Astrana Health had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-14 | |

| Jul-13 | |

| Jul-13 | |

| Jun-04 | |

| May-12 | |

| May-11 | |

| May-08 | |

| May-07 | |

| Apr-21 | |

| Apr-10 | |

| Mar-11 | |

| Mar-03 | |

| Mar-02 | |

| Mar-02 | |

| Mar-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite