|

|

|

|

|||||

|

|

|

Security technology and services company ADT (NYSE:ADT) fell short of the market’s revenue expectations in Q4 CY2025 as sales only rose 1.3% year on year to $1.28 billion. Its non-GAAP profit of $0.23 per share was in line with analysts’ consensus estimates.

Is now the time to buy ADT? Find out by accessing our full research report, it’s free.

“ADT again delivered solid financial performance in 2025, generating robust cash flow and further strengthening our financial foundation. As we enter 2026, we are positioning ADT to lead the next era of smart home intelligence with our ADT+ platform and new ambient sensing capabilities,” said ADT Chairman, President and CEO, Jim DeVries.

Founded in 1874 and headquartered in Boca Raton, Florida, ADT (NYSE:ADT) is a provider of security, automation, and smart home solutions, offering comprehensive services for home and business protection.

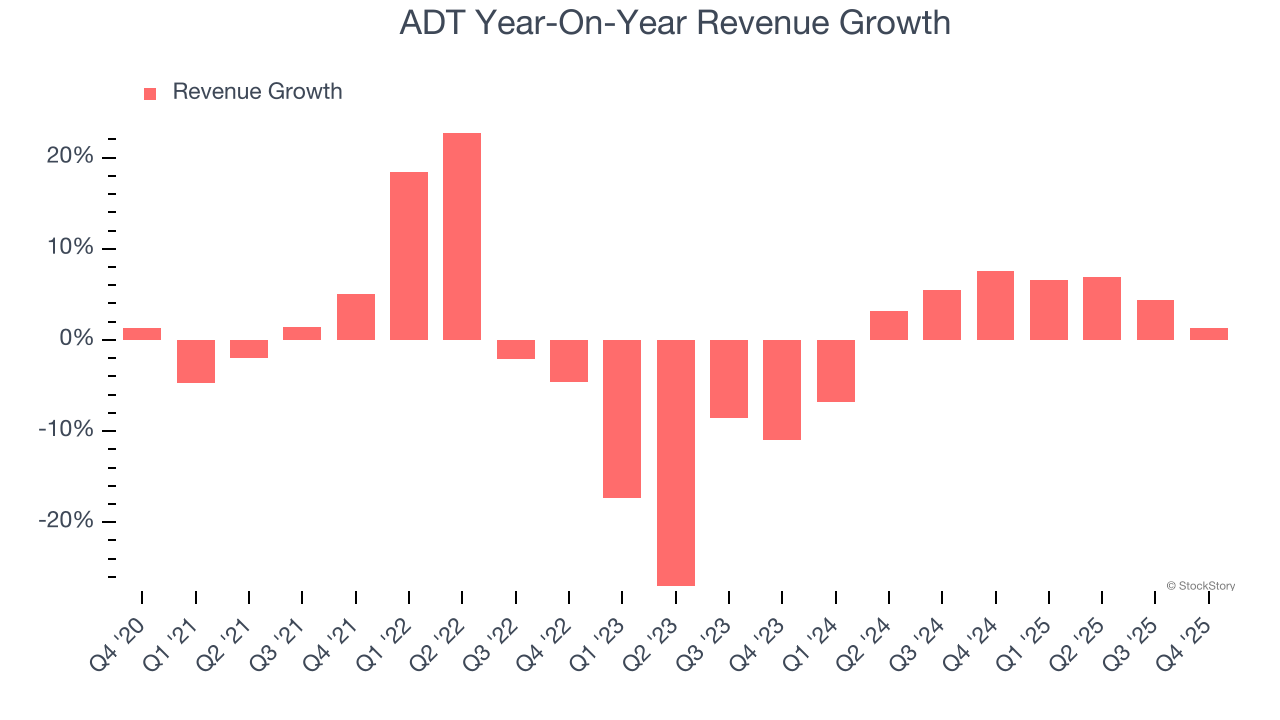

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, ADT struggled to consistently increase demand as its $5.13 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of poor business quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. ADT’s annualized revenue growth of 3.4% over the last two years is above its five-year trend, which is encouraging.

This quarter, ADT’s revenue grew by 1.3% year on year to $1.28 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.6% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not lead to better top-line performance yet.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

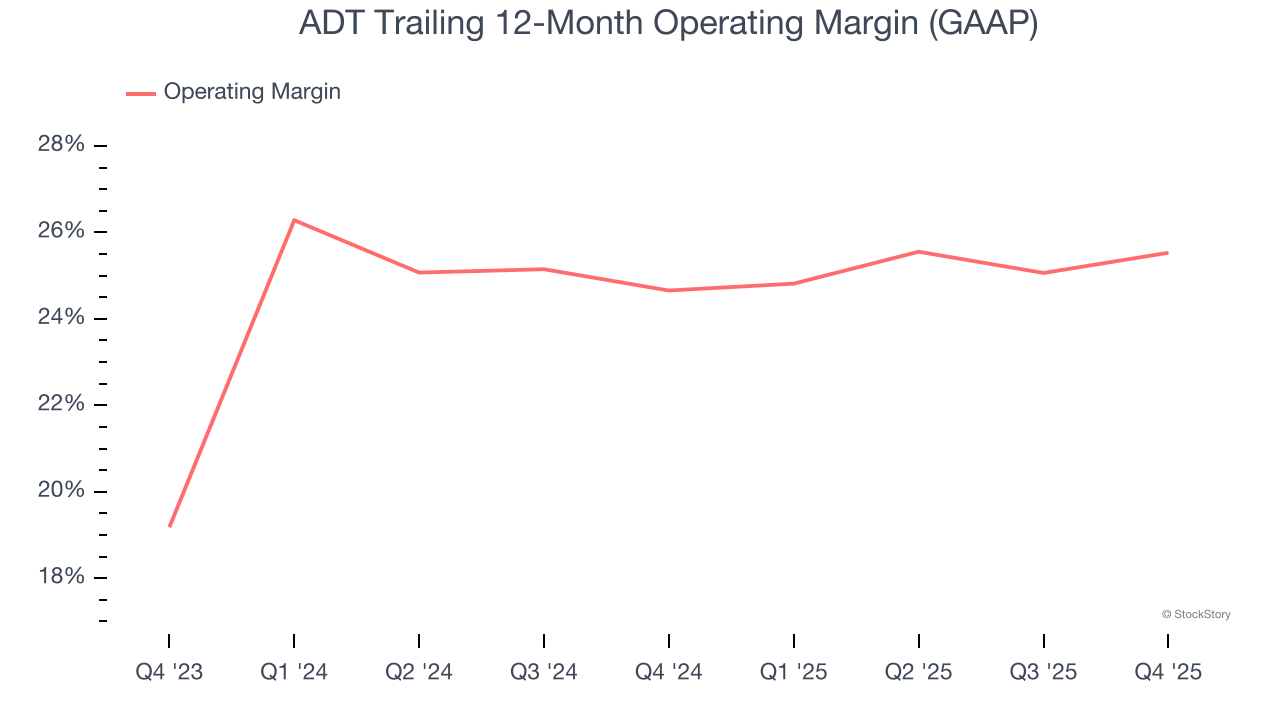

ADT’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 25.1% over the last two years. This profitability was lousy for a consumer discretionary business and caused by its suboptimal cost structure.

In Q4, ADT generated an operating margin profit margin of 26.1%, up 1.9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

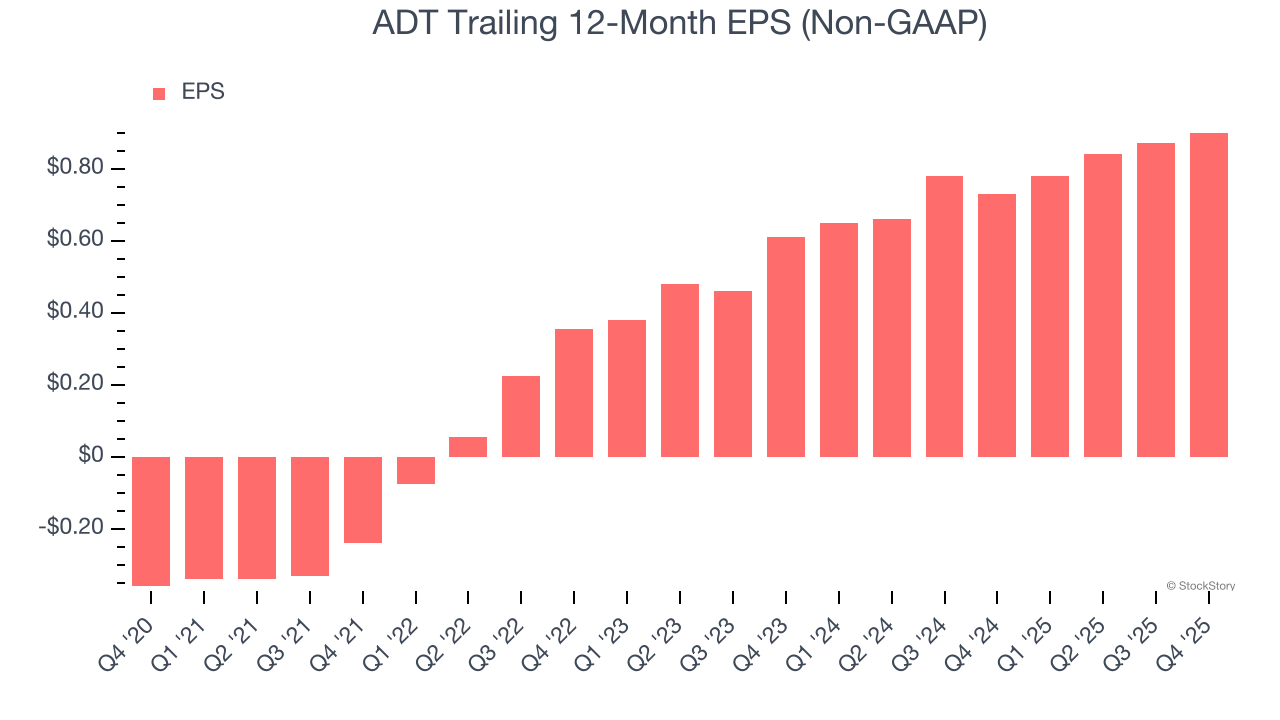

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

ADT’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, ADT reported adjusted EPS of $0.23, up from $0.20 in the same quarter last year. This print beat analysts’ estimates by 3.4%. Over the next 12 months, Wall Street expects ADT’s full-year EPS of $0.90 to grow 5.5%.

It was encouraging to see ADT meet analysts’ EPS expectations this quarter. On the other hand, its revenue slightly missed. Overall, this was a weaker quarter. The stock traded down 1.7% to $7.89 immediately after reporting.

So do we think ADT is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-16 | |

| Jun-18 | |

| Jun-17 | |

| May-20 | |

| May-12 | |

| May-04 | |

| May-04 | |

| Apr-30 | |

| Apr-30 | |

| Apr-30 | |

| Apr-16 | |

| Apr-14 | |

| Mar-31 | |

| Mar-09 | |

| Mar-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite