|

|

|

|

|||||

|

|

|

Over the last six months, Disney’s shares have sunk to $105.50, producing a disappointing 10.8% loss - a stark contrast to the S&P 500’s 7.7% gain. This may have investors wondering how to approach the situation.

Is now the time to buy Disney, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Even with the cheaper entry price, we're cautious about Disney. Here are three reasons why DIS doesn't excite us and a stock we'd rather own.

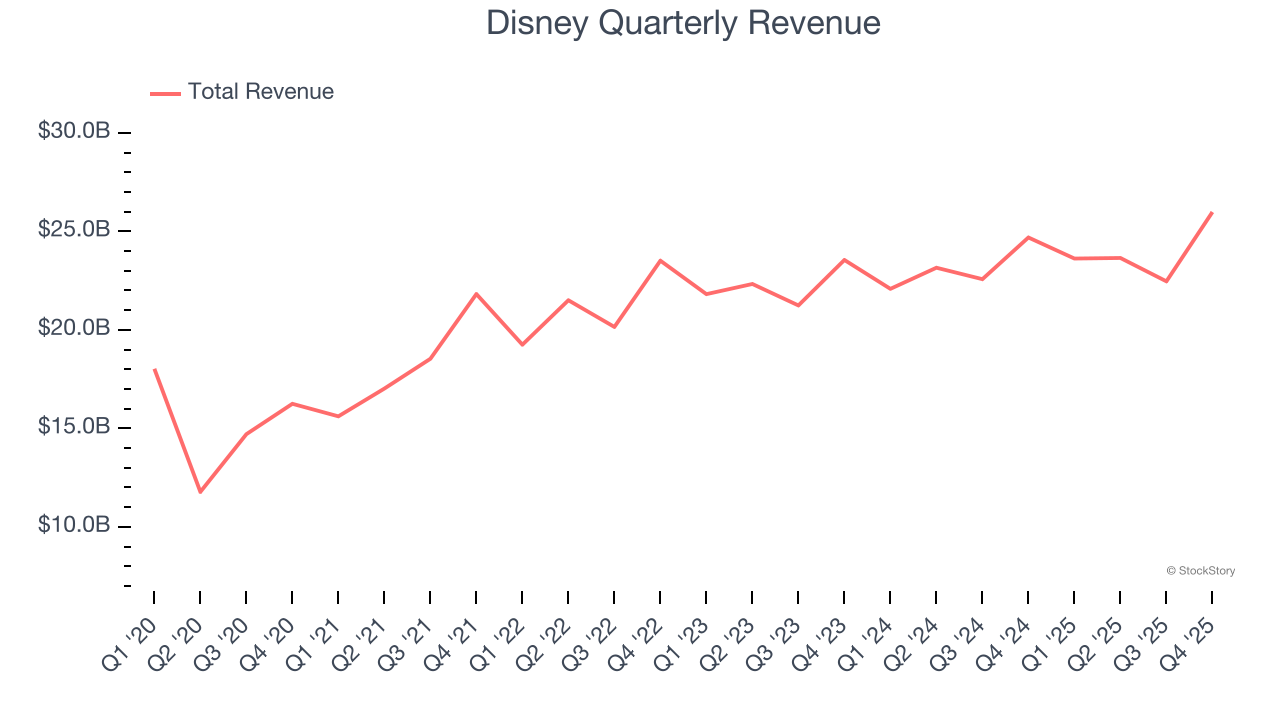

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Disney’s 9.5% annualized revenue growth over the last five years was weak. This fell short of our benchmark for the consumer discretionary sector.

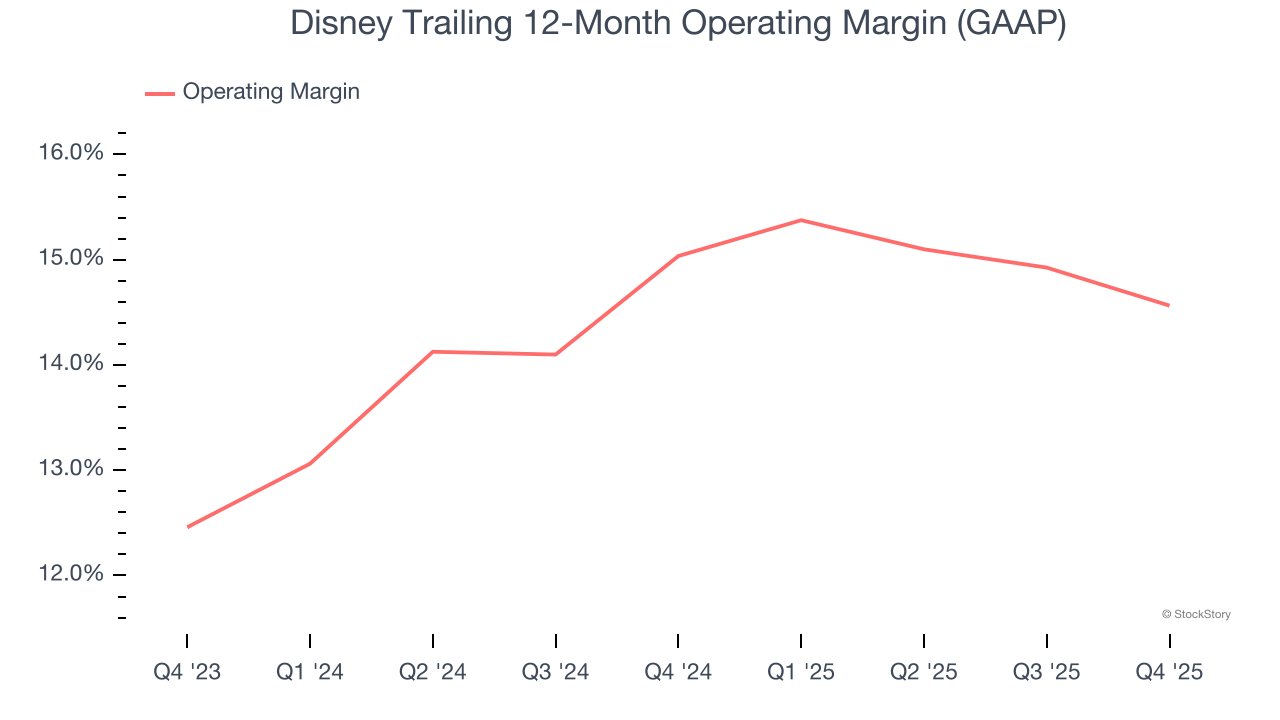

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Disney’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 14.8% over the last two years. This profitability was inadequate for a consumer discretionary business and caused by its suboptimal cost structure.

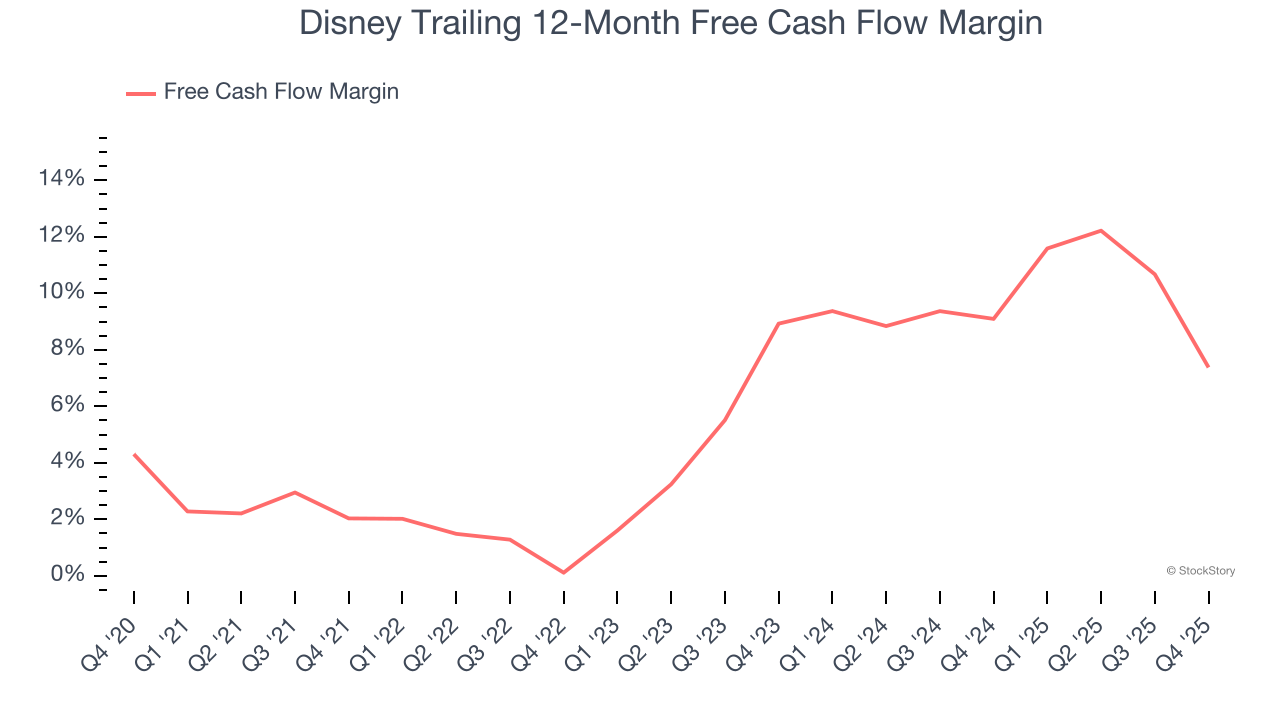

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Disney has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 8.2%, lousy for a consumer discretionary business.

We cheer for all companies serving everyday consumers, but in the case of Disney, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 15.1× forward P/E (or $105.50 per share). This valuation multiple is fair, but we don’t have much confidence in the company. There are better investments elsewhere. We’d suggest looking at a top digital advertising platform riding the creator economy.

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| 2 hours | |

| 7 hours | |

| Apr-13 | |

| Apr-12 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-08 | |

| Apr-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite