|

|

|

|

|||||

|

|

|

Bio-Techne trades at $56.99 and has moved in lockstep with the market. Its shares have returned 7.7% over the last six months while the S&P 500 has gained 5.7%.

Is there a buying opportunity in Bio-Techne, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We're sitting this one out for now. Here are three reasons there are better opportunities than TECH and a stock we'd rather own.

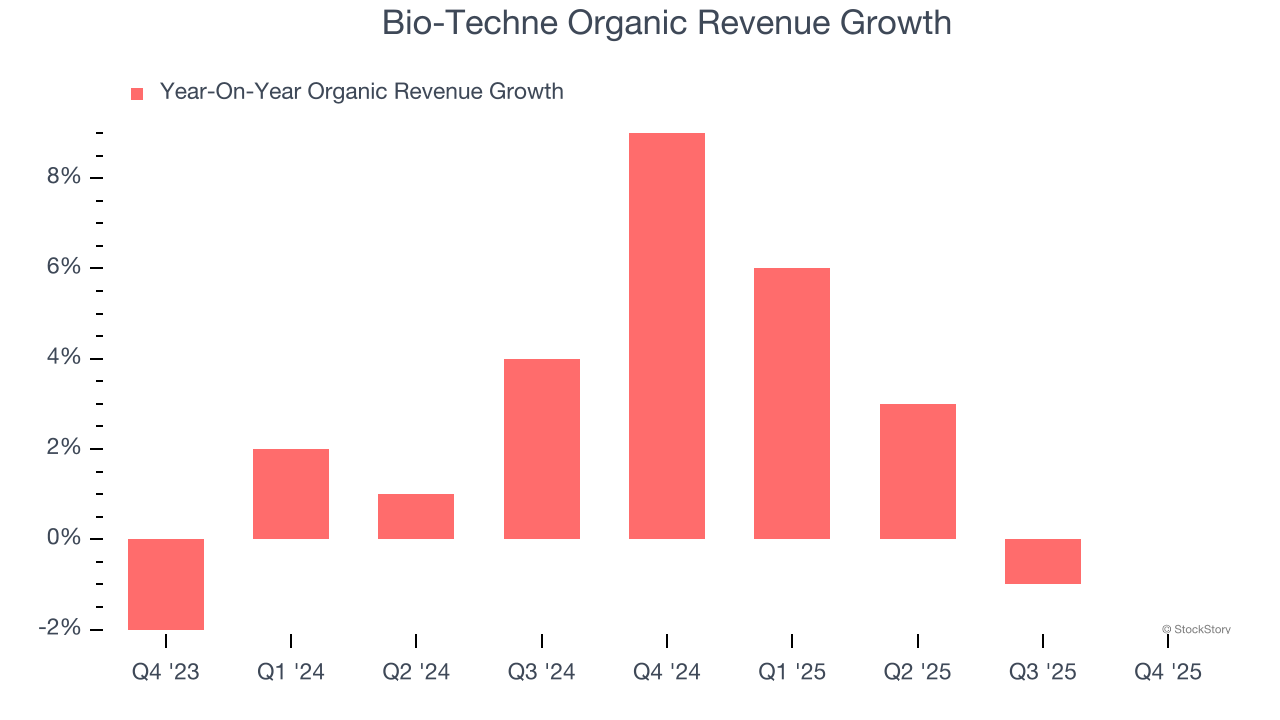

We can better understand Research Tools & Consumables companies by analyzing their organic revenue. This metric gives visibility into Bio-Techne’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Bio-Techne’s organic revenue averaged 3% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.22 billion in revenue over the past 12 months, Bio-Techne is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

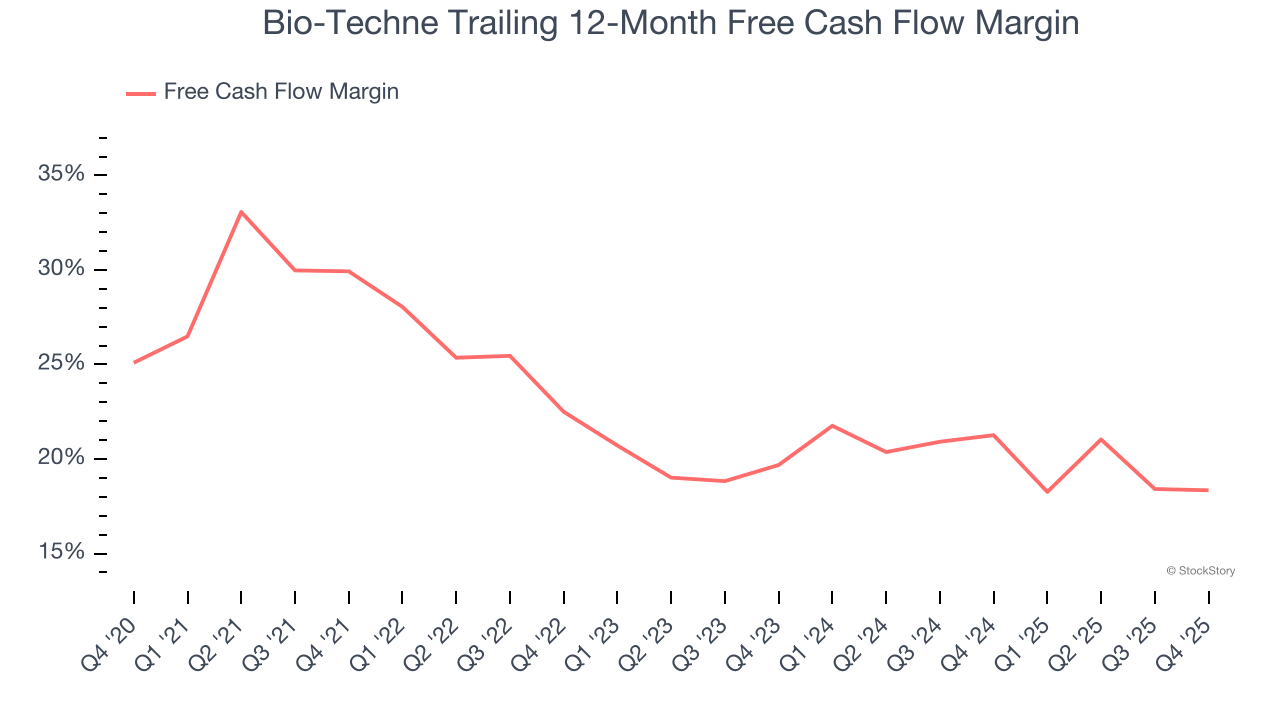

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Bio-Techne’s margin dropped by 11.6 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Bio-Techne’s free cash flow margin for the trailing 12 months was 18.3%.

We cheer for all companies helping people live better, but in the case of Bio-Techne, we’ll be cheering from the sidelines. That said, the stock currently trades at 28.1× forward P/E (or $56.99 per share). At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere. Let us point you toward the most dominant software business in the world.

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-08 | |

| Jul-02 | |

| Jul-01 | |

| Jun-29 | |

| Jun-26 | |

| Jun-26 | |

| Jun-26 | |

| Jun-25 | |

| Jun-25 | |

| Jun-25 |

Germany's Merck to Boost Lab-Tools Business With $11 Billion Bio-Techne Deal

TECH +20.08%

The Wall Street Journal

|

| Jun-25 |

Merck KGaA to buy Bio-Techne for $11.3bn in life science footprint expansion

TECH +20.08%

Medical Device Network

|

| Jun-25 | |

| Jun-25 | |

| Jun-25 | |

| Jun-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite