|

|

|

|

|||||

|

|

|

The Home Depot, Inc. HD expects comparable sales growth in fiscal 2026 to be stronger in the second half than in the first half. Management expects comparable sales to be flat to up 2% for the fiscal year. This guidance is largely driven by the lapping of significant headwinds that pressured performance during the latter part of fiscal 2025.

On its last earnings call, management highlighted that the expected improvement in second-half comparable sales is mainly a function of how storm activity influenced results in fiscal 2025. Storm-related demand typically creates temporary spikes in categories such as roofing, building materials and other repair-oriented products. When storms occur in a year but not the next, year-over-year comparisons can create uneven performance across quarters.

Earlier quarters in fiscal 2026 are expected to face tougher year-over-year comparisons tied to those weather-related demand patterns. As the fiscal year progresses and the company moves beyond those periods, the comparison base becomes more favorable, which is expected to support relatively stronger comparable sales performance in the back half.

Management noted that underlying demand has remained relatively stable despite ongoing pressure from housing affordability constraints and elevated mortgage rates. By the back half of fiscal 2026, the company expects its aggressive investments in Pro-specific capabilities to yield more significant results. The continued integration and organic growth of SRS and GMS are also expected to contribute to HD’s performance.

These strategic initiatives, combined with a more favorable year-over-year comparison in the back half, underpin the company’s confidence in an accelerating comparable sales trend as the fiscal year progresses.

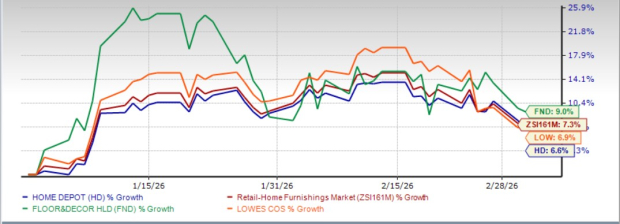

Home Depot, which competes with Floor & Decor Holdings, Inc. FND and Lowe's Companies, Inc. LOW, has seen its shares rise 6.6% year to date compared with the industry’s 7.3% growth. While shares of Floor & Decor Holdings have jumped 9%, Lowe’s has advanced 6.9% in the same period.

From a valuation standpoint, Home Depot trades at a forward price-to-earnings ratio of 24.00, higher than the industry’s 22.08. HD carries a Value Score of C. Home Depot is trading at a discount to Floor & Decor Holdings (with a forward 12-month P/E ratio of 30.75) but at a premium to Lowe’s (19.98).

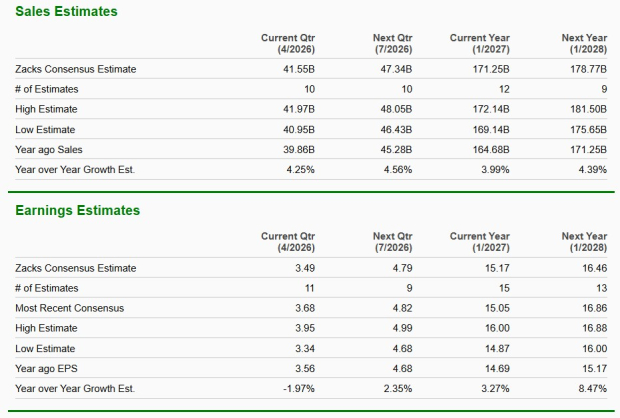

The Zacks Consensus Estimate for Home Depot’s current financial-year sales implies year-over-year growth of 4%, while the same for earnings per share suggests an increase of 3.3%. For the next fiscal year, the consensus estimate indicates a 4.4% rise in sales and 8.5% growth in earnings.

Home Depot currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 11 hours | |

| 16 hours | |

| Jul-27 | |

| Jul-23 | |

| Jul-20 | |

| Jul-17 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-13 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite