|

|

|

|

|||||

|

|

|

Clover Health Investments CLOV is well poised for growth in the coming quarters, courtesy of its broad product spectrum. This optimism is primarily driven by its technology-first care model, as evident from solid membership growth, rising revenues and sustained adjusted EBITDA profitability. However, elevated medical costs, margin pressure and execution risks in scaling Clover Assistant present near-term challenges.

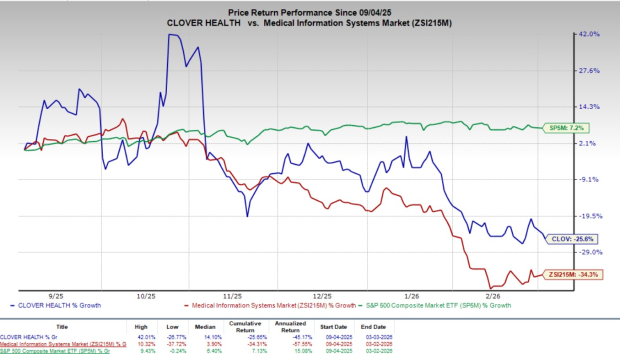

Shares of this Zacks Rank #3 (Hold) company have lost 25.6% over the past six months compared with the industry’s 34.3% decline. However, the S&P 500 Index has risen 7.2% in the same time frame.

Clover, a tech-enabled Medicare Advantage insurer leveraging its proprietary AI-powered platform, has a market capitalization of $1.05 billion. The company projects 39.8% earnings growth for the first quarter of 2026.

Its earnings surpassed estimates in one of the trailing four quarters, missed one and met the other two, delivering an average surprise of 17.86%.

Strong Membership Growth and Star Ratings Momentum: Clover delivered robust membership momentum in fourth-quarter 2025, with Medicare Advantage enrollment rising 38% year over year. The company closed the quarter with over 113,803 insurance members, reflecting a 4.4% sequential increase. After earning a 4-Star rating from CMS for its flagship PPO plan covering more than 95% of its members, Clover now qualifies for higher quality bonus payments and stronger plan-level economics. The improved rating should further support membership growth. Alongside its attractive benefits and affordable out-of-pocket structure in underserved regions, this blend of steady organic enrollment gains, stronger member retention and incremental bonus revenues builds a strong growth cycle, supporting durable revenue expansion and improving operating efficiency over time.

Adjusted EBITDA Profitability Momentum: Clover has demonstrated solid financial progress, delivering $22 million in adjusted EBITDA in 2025. This improvement reflects tight cost discipline, better control of medical cost ratios and efficiencies gained through its workforce optimization and a redesigned operating infrastructure.

Clover expects 2026 to be its first full year of GAAP net income profitability, guiding to net income between breakeven and $20 million and adjusted EBITDA of $50-$70 million. A key tailwind is 2026 being a 4-star payment year, benefiting 97% of members in Clover’s PPO plan. Additional support comes from a favorable Part C rate notice, deeper Clover Assistant engagement, expanded PCP adoption and growth concentrated in core markets where integration is strongest.

Management also highlighted better new member unit economics through more cost-efficient acquisition channels, Part D optimization initiatives and corrective actions taken to address elevated dental and DME utilization seen in 2025. At the same time, continued SG&A leverage and scale efficiencies are expected to further expand margins.

Strategic Positioning and Long-Term Durability: Clover believes its model is structurally aligned with the evolving Medicare Advantage policy environment. Since its model is built on claims-linked documentation and real-time physician workflows powered by Clover Assistant, management sees this direction as reinforcing its long-term approach. Instead of depending on annual rate increases or favorable star ratings to sustain profitability, CLOV focuses on disciplined cost management and clinical integration drive performance, making it less sensitive to policy cycles.

2027 priorities include maintaining leadership in New Jersey, where Clover is the largest individual non-SNP PPO plan and scaling its technology platform. The company aims to expand Counterpart Health, targeting parity between Counterpart Assistant and Clover Assistant lives managed, positioning technology as a parallel long-term growth engine.

Elevated Insurance Benefit Expense Ratio: Clover reported an Insurance Benefit Expense Ratio (BER) of 90.9% in 2025, a 970 basis-point increase year over year. While this reflects strong member utilization, indicating active engagement with healthcare services, it also underscores continued pressure on insurance margins.

One major driver was the rollout of a new Clover Assistant-enabled affiliated entity designed to strengthen care coordination. Although strategically important for long-term clinical and economic outcomes, the initiative created additional short-term cost pressure. Expense levels were also impacted by normal seasonality and higher-than-expected inpatient utilization earlier in the quarter.

As the company continues to grow, improving BER will depend on capturing efficiencies from its technology-enabled care model and maintaining tighter control over medical costs. This is significantly important amid ongoing risk adjustment changes and competitive dynamics within Medicare Advantage.

Regulatory and Policy Dependence: Clover operates in a highly regulated Medicare Advantage environment, where changes in risk adjustment, rate notices and policy guidance can affect financial outcomes. Although the company has successfully navigated transitions like HCC v28 and recent rate notices, the broader Medicare Advantage environment remains politically sensitive and subject to regulatory shifts. Policy misalignment, delays in data sharing or unfavorable regulatory changes could create headwinds.

The U.S. government’s recent “Big Beautiful Bill” introduces automatic Medicare spending reductions of 4%, totaling an estimated $500 billion over eight years beginning in 2026. These cuts could affect overall Medicare funding levels and reimbursement dynamics. The legislation also includes substantial Medicaid reductions, which may indirectly impact low-income Medicare beneficiaries who rely on Medicaid for supplemental coverage. Around 1.3 million beneficiaries could lose Medicaid support, affecting plan enrollment mix and future revenue visibility for Clover.

Scaling Technology-Driven Care Platforms:Clover’s differentiation relies heavily on Clover Assistant and its expansion into Counterpart Health. The ability to grow these platforms, deepen physician adoption and translate clinical engagement into economic upside is essential to sustaining long-term earnings growth. If adoption slows or operational challenges arise in new markets like Georgia, the anticipated benefits of AI-enabled care management could lag, limiting both cost-control advantages and profitability. Monetizing Counterpart Health remains a work in progress and failure to scale efficiently could constrain CLOV’s growth trajectory.

Clover Health Investments, Corp. price | Clover Health Investments, Corp. Quote

Clover Health is witnessing a stable estimate revision trend for 2026. For the past 30 days, the Zacks Consensus Estimate for full-year 2026 earnings has remained unchanged at 6 cents per share.

Some better-ranked stocks from the broader medical space are Intuitive Surgical ISRG, Phibro Animal Health PAHC and GE HealthCare Technologies GEHC.

Intuitive Surgical, sporting a Zacks Rank #1 (Strong Buy) at present, reported fourth-quarter 2025 adjusted earnings per share (EPS) of $2.53, beating the Zacks Consensus Estimate by 12.4%. Revenues of $2.87 billion surpassed the Zacks Consensus Estimate by 4.7%. You can see the complete list of today’s Zacks #1 Rank stocks here.

ISRG’s earnings per share estimate for 2026 has moved up 46 cents to $10.07 in the past 60 days. The company beat earnings estimates in the trailing four quarters, the average surprise being 13.2%.

Phibro Animal Health, currently flaunting a Zacks Rank #1, reported second-quarter 2025 adjusted EPS of 87 cents, which surpassed the Zacks Consensus Estimate by 26.1%. Revenues of $373.9 million beat the Zacks Consensus Estimate by 4.7%.

PAHC’s earnings per share estimate for 2026 has moved up 26 cents to $3.02 in the past 60 days. The company’s earnings beat estimates in the trailing four quarters, the average surprise being 20.1%.

GE HealthCare Technologies, currently carrying a Zacks Rank #2 (Buy), reported fourth-quarter 2025 adjusted EPS of $1.44, which surpassed the Zacks Consensus Estimate by 0.7%. Revenues of $5.7 billion beat the Zacks Consensus Estimate by 1.9%.

GEHC’s earnings per share estimate for 2026 has moved up 6 cents to $4.99 in the past 60 days. The company beat earnings estimates in the trailing four quarters, the average surprise being 7.5%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite