|

|

|

|

|||||

|

|

|

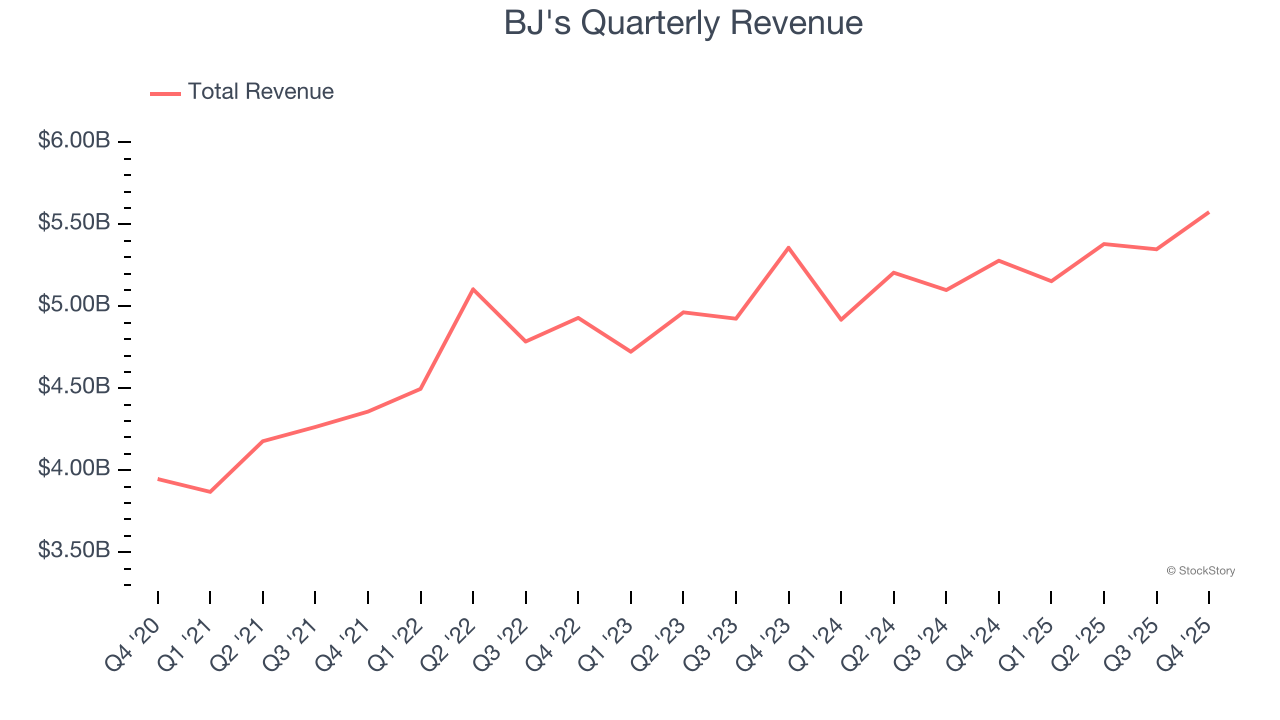

Membership-only discount retailer BJ’s Wholesale Club (NYSE:BJ) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 5.6% year on year to $5.58 billion. Its non-GAAP profit of $0.96 per share was 3.3% above analysts’ consensus estimates.

Is now the time to buy BJ's? Find out by accessing our full research report, it’s free.

Appealing to the budget-conscious individual shopping for a household, BJ’s Wholesale Club (NYSE:BJ) is a membership-only retail chain that sells groceries, appliances, electronics, and household items, often in bulk quantities.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $21.46 billion in revenue over the past 12 months, BJ's is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. For BJ's to boost its sales, it likely needs to adjust its prices or lean into foreign markets.

As you can see below, BJ's grew its sales at a sluggish 3.6% compounded annual growth rate over the last three years as it barely increased sales at existing, established locations.

This quarter, BJ's grew its revenue by 5.6% year on year, and its $5.58 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.1% over the next 12 months, an acceleration versus the last three years. This projection is particularly healthy for a company of its scale and indicates its newer products will fuel better top-line performance.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

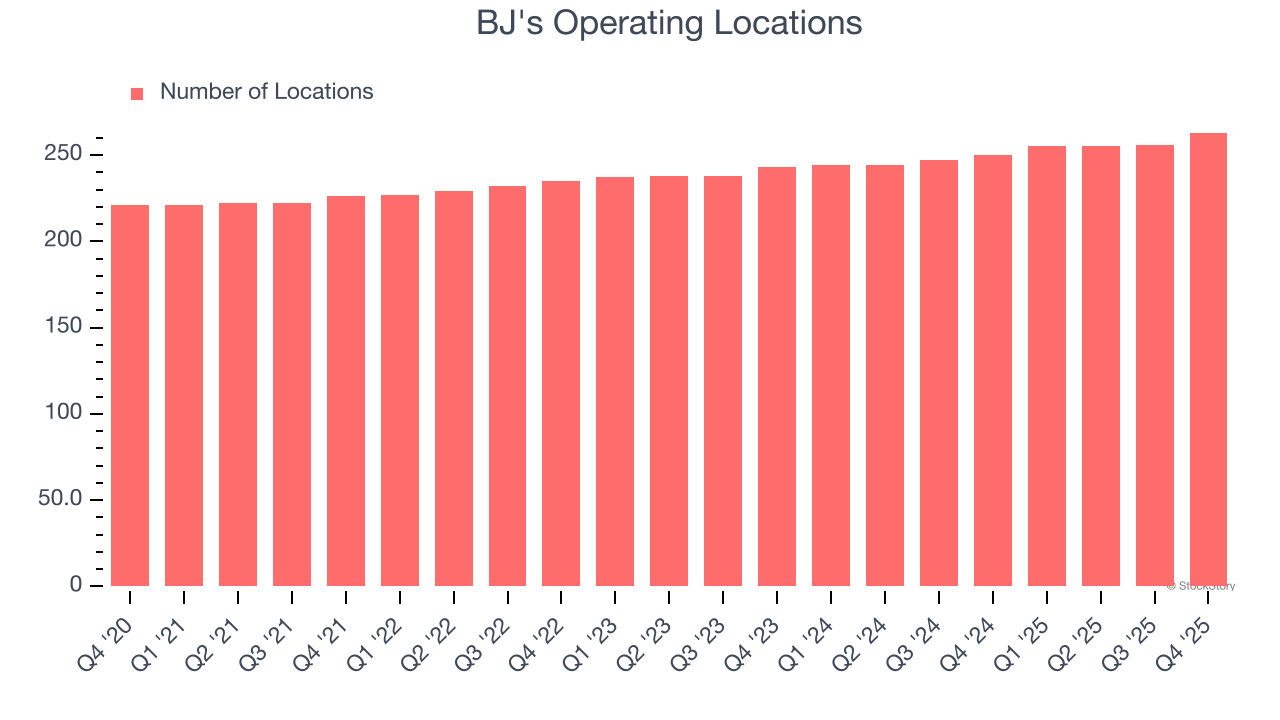

BJ's operated 263 locations in the latest quarter. It has opened new stores quickly over the last two years, averaging 3.7% annual growth, faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

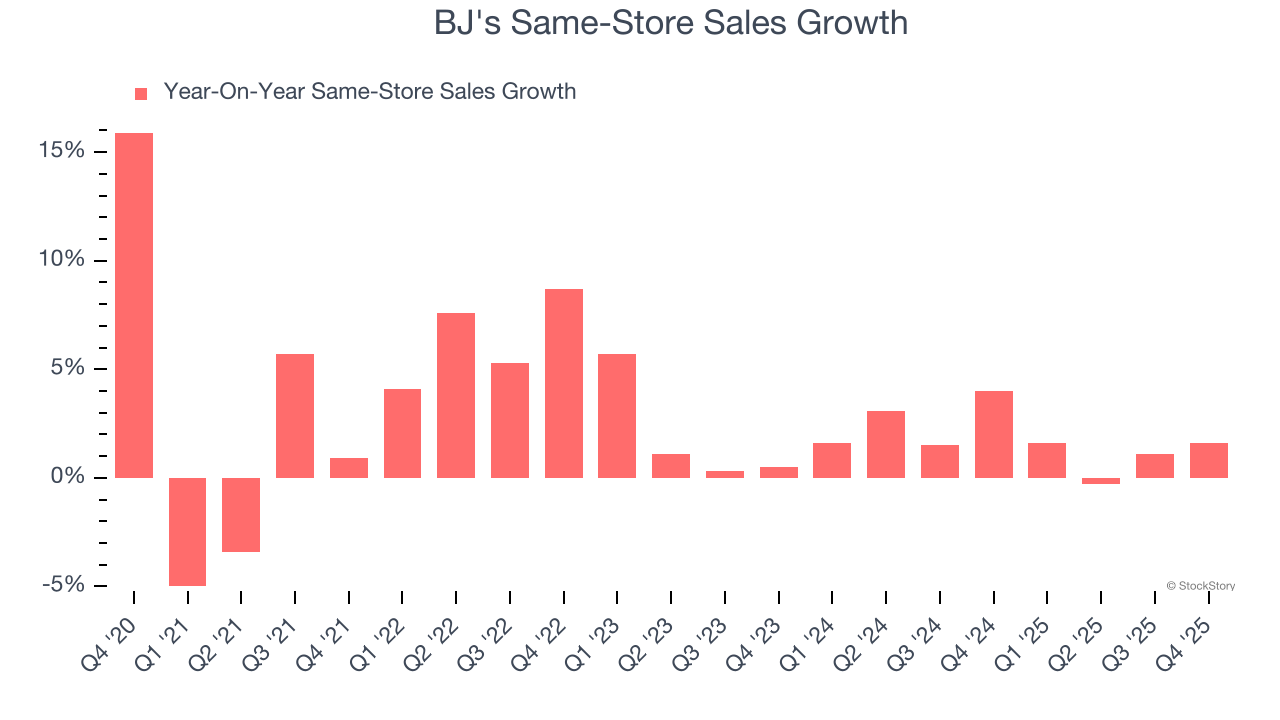

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

BJ’s demand within its existing locations has been relatively stable over the last two years but was below most retailers. On average, the company’s same-store sales have grown by 1.8% per year. This performance suggests it should consider improving its foot traffic and efficiency before expanding its store base.

In the latest quarter, BJ’s same-store sales rose 1.6% year on year. This performance was more or less in line with its historical levels.

It was good to see BJ's narrowly top analysts’ gross margin expectations this quarter. We were also happy its revenue was in line with Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its EBITDA fell slightly short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 3.1% to $96.90 immediately after reporting.

BJ's underperformed this quarter, but does that create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-23 | |

| Jul-10 | |

| May-29 | |

| May-28 | |

| May-27 | |

| May-26 | |

| May-26 | |

| May-25 | |

| May-25 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite