|

|

|

|

|||||

|

|

|

Freeport-McMoRan Inc. FCX saw a sharp increase in its average unit net cash cost per pound of copper in the fourth quarter of 2025 to $2.22 from $1.40 in the prior quarter, marking a roughly 59% spike. It also climbed 34% year over year. The increase was fueled by a decline in copper sales volumes.

Freeport’s copper sales volumes tumbled approximately 29% year over year in the fourth quarter to 709 million pounds, and fell from 977 million pounds in the prior quarter. The downside primarily resulted from the temporary suspension of operations since the mud rush incident at the Grasberg Block Cave mine in Indonesia in September 2025.

Freeport's outlook for the first quarter of 2026 suggests higher costs on a sequential basis. It expects unit net cash costs to rise to $2.60 per pound, while projecting a full-year average of roughly $1.75. Lower expected sales volumes are likely to adversely impact costs in the quarter. Higher costs are expected to weigh on the company's margins.

Among FCX’s peers, Southern Copper Corporation SCCO reported lower unit costs in the fourth quarter. Southern Copper’s operating cash cost per pound of copper, net of by-product revenue credits, was 52 cents, marking a roughly 46% decline from 96 cents per pound reported in the prior-year quarter. SCCO’s operating cash cost per pound of copper also declined roughly 34% year over year in 2025.

BHP Group Limited BHP saw lower unit costs across its Escondida and Copper South Australia operations in the first half of fiscal 2026 (ended Dec. 31, 2025), partly offset by an increase at Spence. BHP expects the unit cost for Escondida to be in the band of $1.20-$1.50 per pound for fiscal 2026. BHP also projects Copper South Australia’s unit cost to be between $1 and $1.50 per pound. Unit costs at Spence are expected to be between $2.10 and $2.40 per pound for fiscal 2026.

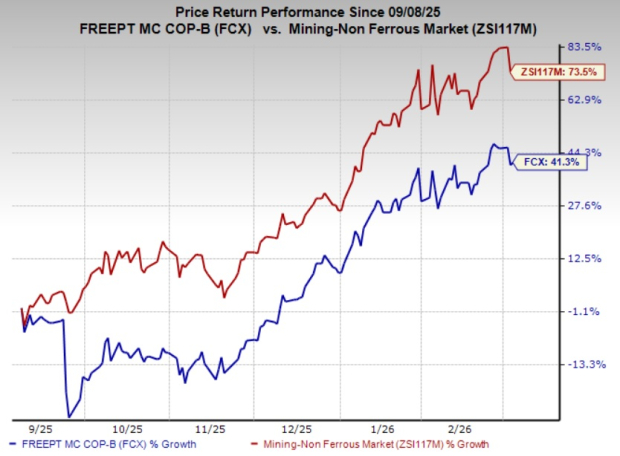

Shares of Freeport are up 41.3% in the past six months against the Zacks Mining - Non Ferrous industry’s rise of 73.5%.

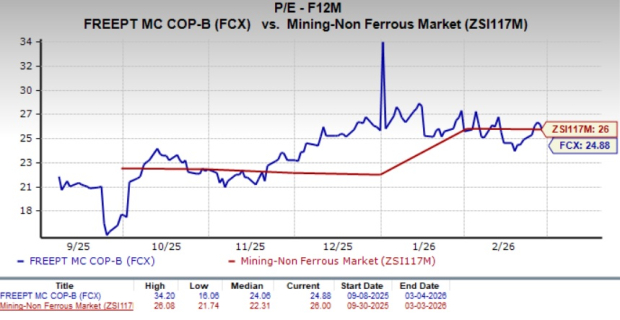

From a valuation standpoint, FCX is currently trading at a forward 12-month earnings multiple of 24.88, a 4.3% discount to the industry average of 26X. It carries a Value Score of B.

The Zacks Consensus Estimate for FCX’s 2026 and 2027 earnings implies a year-over-year rise of 44.1% and 22.3%, respectively. The EPS estimates for 2026 and 2027 have been trending higher over the past 30 days.

FCX stock currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite