|

|

|

|

|||||

|

|

|

MasTec, Inc. MTZ reported fourth-quarter 2025 results on Feb. 26, with both earnings and revenues exceeding the Zacks Consensus Estimate by 6.7% and 6.1%, respectively. The company also delivered strong year-over-year growth across key metrics.

This Florida-based infrastructure construction company delivered a strong operational performance in the fourth quarter. Adjusted earnings per share (EPS) came in at $2.07, increasing 44% year over year. Revenues totaled $3.94 billion, rising nearly 16% from the prior-year quarter. Growth was driven by strong activity across communications, clean energy and pipeline infrastructure markets. Higher wireless and fiber deployments, continued renewable project momentum and improving pipeline volumes supported the top line.

Strong execution across projects also aided profitability. Adjusted EBITDA margin increased 60 bps to 8.6% from the year-ago quarter. In addition, the backlog expanded significantly, reflecting sustained demand tied to energy transition and infrastructure investment. (read more: MasTec Beats Q4 Earnings & Revenue Estimates, Books Solid Backlog)

However, the company continued to face certain near-term challenges. Project delays, start-up costs tied to new programs and ongoing investments to support growth created some pressure on margins during the quarter.

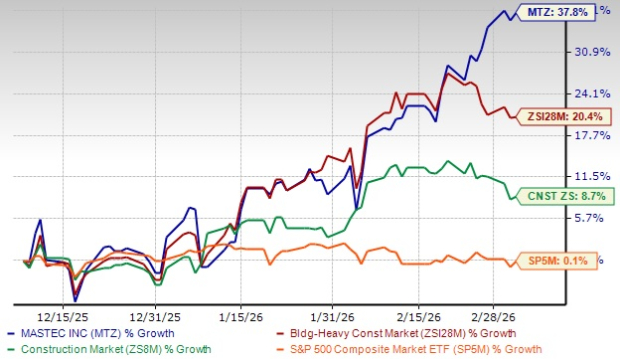

Shares of MasTec have gained 37.8% in the past three months, significantly outperforming the Zacks Building Products - Heavy Construction industry’s 20.4% growth. The stock has further outperformed the broader Construction sector and the S&P 500, which have advanced 8.7% and 0.1%, respectively, in the same period. Let us take a closer look at the factors shaping MasTec stock’s prospects.

MasTec entered 2026 with a significantly stronger backlog, providing solid visibility into future revenues. As of Dec. 31, 2025, the company reported an 18-month backlog of about $18.96 billion, up 33% year over year and 13% sequentially. The increase was broad-based across all four operating segments, with the largest gains coming from the Pipeline Infrastructure and Clean Energy and Infrastructure businesses. Pipeline backlog expanded as energy infrastructure projects continued to move forward, while the clean energy unit benefited from higher renewable and infrastructure contract awards.

Beyond the headline numbers, management highlighted strong project visibility and a growing pipeline of opportunities tied to grid upgrades, renewable installations and digital infrastructure. With demand strengthening across several end markets, MasTec’s expanding backlog provides a strong foundation for revenue growth in the coming quarters.

MasTec continues to benefit from strong spending on telecommunications infrastructure. In the fourth quarter, revenues from the Communications segment increased 23% year over year. The growth was driven by strong wireless and wireline construction activity as telecom providers accelerated broadband deployment.

Investments in fiber networks and mobility infrastructure are expanding nationwide to support rising data usage and artificial intelligence-driven connectivity needs. With telecommunications providers continuing to expand network capacity and broadband access, the communications business remains a key growth engine for MTZ going forward.

MasTec’s Clean Energy and Infrastructure segment remains a major beneficiary of the global shift toward renewable energy. The segment delivered solid growth during 2025, supported by rising activity in solar, wind and infrastructure construction projects. New contract wins during the quarter drove a meaningful increase in backlog, reflecting strong customer demand for renewable power installations.

Industry tailwinds such as electrification, grid modernization and energy transition investments continue to support the segment’s outlook. With utilities and developers increasing spending on renewable infrastructure, MasTec remains well-positioned to capture additional opportunities in this market over the coming years.

MasTec is also gaining momentum from the rising demand for digital infrastructure. During the fourth quarter, the company secured nearly $1 billion of data-center-related work as part of its growing backlog. These projects involve a mix of construction management, civil work, power delivery and telecom infrastructure services, allowing the company to leverage multiple capabilities within a single project.

The expansion of artificial intelligence, cloud computing and data processing is driving large investments in data center infrastructure across the United States. As hyperscale operators and technology companies continue to build new facilities, MasTec is seeing increasing opportunities to participate in these projects. Over time, the company expects data center development to become a meaningful contributor to growth.

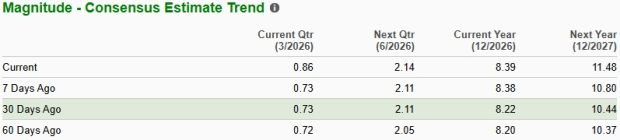

MasTec’s 2026 earnings estimate has increased to $8.39 per share from $8.22 over the past 30 days. The estimated figure for 2026 implies growth of 28.1% year over year on projected revenue growth of 19%.

Despite favorable demand trends across infrastructure and energy markets, certain operational pressures continue to weigh on MasTec’s near-term outlook. Rapid business expansion and the ramp-up of new programs are creating start-up costs and operational inefficiencies in some segments. These investments are aimed at supporting long-term growth but can limit margin expansion as projects scale and operations mature. In addition, project timing can vary due to permitting requirements and customer scheduling, which may affect revenue recognition in certain periods.

The fourth quarter also reflected some of these challenges. Margin performance in the Power Delivery segment came under pressure due to project mix headwinds and delays related to permitting issues on portions of the Greenlink transmission project. At the same time, ongoing investments to support strong organic growth and new program launches increased operating costs. If project delays persist or cost pressures remain elevated, these factors could weigh on MasTec’s near-term profitability and earnings visibility.

MTZ stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 34.77, as shown in the chart below.

MasTec operates in highly competitive energy, power and infrastructure markets, where it competes with established industry players such as EMCOR Group, Inc. EME, Quanta Services, Inc. PWR and Primoris Services Corporation PRIM. Each of these companies holds strong capabilities in different areas of infrastructure construction and engineering services.

EMCOR leverages a broad mechanical and electrical services network, allowing it to maintain strong regional coverage across industrial, commercial and utility markets. This footprint helps generate steady work from maintenance contracts, facility upgrades and distributed energy projects. Quanta Services remains a leading player in the electric power space, supported by deep expertise in transmission and distribution infrastructure and long-standing relationships with utility customers, positioning it to secure major grid modernization and high-voltage transmission projects. Primoris Services continues to expand its presence across solar, gas infrastructure and civil construction, supported by flexible project execution and long-term master service agreements.

At the same time, industry demand continues to expand as renewable energy deployment accelerates and utilities increase investments in grid modernization and electrification. Within this environment, MasTec benefits from its ability to deliver multi-scope infrastructure services across power, energy and communications networks. This integrated capability allows the company to participate in complex infrastructure projects that require multiple service offerings, providing a competitive edge alongside larger peers.

MasTec continues to benefit from strong demand across communications, clean energy and digital infrastructure markets. A growing backlog, rising telecom investments and expanding data center opportunities provide visibility into future revenues. The company is also seeing favorable estimate revisions for 2026, indicating improving earnings prospects as infrastructure spending remains strong.

That said, certain challenges remain. Start-up costs tied to new programs, project timing variability and margin pressure in some segments could create near-term volatility. In addition, MTZ is currently trading at a premium valuation compared with peers, which may limit immediate upside.

Given this backdrop, this Zacks Rank #3 (Hold) stock appears positioned for steady performance in the near term. Existing investors may consider holding the stock, while new investors might wait for a more attractive entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-22 | |

| Jul-21 | |

| Jul-20 | |

| Jul-16 | |

| Jul-16 | |

| Jul-10 | |

| Jul-10 |

AI Data-Center Boom Has 'Longer Legs Than People Think': Infrastructure Veteran

MTZ

Investor's Business Daily

|

| Jul-09 | |

| Jul-07 | |

| Jul-01 | |

| Jul-01 | |

| Jun-25 | |

| Jun-25 | |

| Jun-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite