|

|

|

|

|||||

|

|

|

Inspire Medical Systems INSP is well-positioned for solid growth over the next few quarters as it navigates a significant product transition.

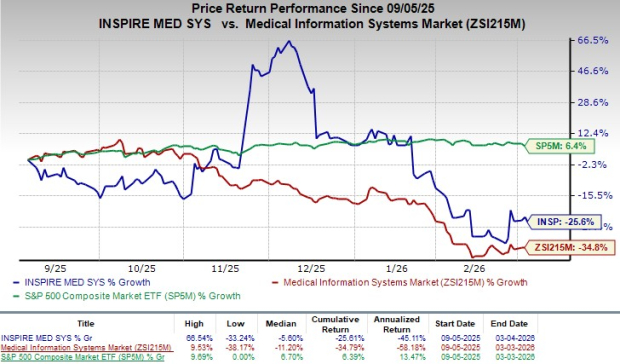

Shares of this Zacks Rank #3 (Hold) company have lost 25.6% over the past six months compared with the industry’s 34.8% decline. The S&P 500 Index has increased 6.4% in the same time frame.

Inspire Medical, a medical technology company focused on the development and commercialization of innovative, minimally invasive solutions for patients with obstructive sleep apnea, has a market capitalization of $1.88 billion.

The company’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 185.1%.

Focus on R&D: Inspire Medical continues to invest in R&D to improve patient selection, expand indications and simplify therapy management. In early 2024, the company completed enrollment of 600 patients in its PREDICTOR study. The study evaluates whether factors like BMI and neck circumference can help predict the absence of complete concentric collapse at the soft palate. Early findings suggest some patients may not need drug-induced sleep endoscopy screening, which could streamline the treatment pathway and improve procedural efficiency.

The company is also strengthening its intellectual property portfolio. As of Dec. 31, 2025, Inspire Medical held rights to 119 issued U.S. patents, along with numerous pending U.S. and foreign patent applications and trademark filings. R&D spending remains a key focus. Expenses accounted for 9.3% of revenues in the fourth quarter of 2025 and 11.3% for full-year 2024, supporting next-generation Inspire neurostimulators, the SleepSync programmer and platform, along with regulatory and clinical study activities.

Regulatory Expansion and Clinical Scale: Inspire Medical has treated more than 125,000 patients worldwide across the United States, Europe and Asia. This growing installed base reinforces its first-mover advantage and embeds the therapy within ENT and sleep center workflows. It also supports a large and expanding body of clinical evidence, including more than 385 peer-reviewed publications. This strengthens physician confidence and improves engagement with payors.

Regulatory progress is also expanding the addressable market. In 2023, the FDA raised the upper apnea-hypopnea index limit to 100 from 65 and increased the BMI warning to 40 from 32, widening eligibility among moderate-to-severe OSA patients. The same year, the therapy was approved for certain pediatric patients with Down syndrome. In 2024, the FDA cleared the next-generation Inspire V neurostimulator, launched in the United States in 2025, which integrates the respiratory sensor within the device and simplifies the implant procedure.

Solid Q4 Results: Inspire Medical exited the fourth quarter of 2025 with better-than-expected results. The solid improvement of the top line and improved margins were impressive. The company’s launch progress with the latest Inspire V models in the United States looks promising as management stated that more than 90% of its centers have implanted the device.

Inspire Medical exited fourth-quarter 2025 with cash and cash equivalents and short-term investments of $308 million compared with $323 million at the end of the third quarter. The company does not have any debt on its balance sheet. Therefore, there appears to be no near-term threat to its solvency.

Overdependence on Inspire System: Sales of the Inspire system generate nearly all of Inspire Medical’s revenue and are expected to remain the company’s primary revenue driver for the foreseeable future. Although the company reported net income in 2024 and 2025, it historically incurred operating losses and may face challenges sustaining profitability. Future performance depends heavily on continued adoption of Inspire therapy among moderate to severe OSA patients who cannot tolerate or benefit from PAP therapies like CPAP.

As a single-product company, Inspire Medical faces significant risk if the therapy fails to maintain strong physician or patient acceptance. Adoption could also be limited by anatomical constraints, reluctance to undergo an implant procedure, potential side effects such as infection or tongue discomfort and reimbursement or insurance coverage challenges.

Inspire Medical is witnessing a positive estimate revision trend for 2026. In the past 30 days, the Zacks Consensus Estimate for earnings has moved north 21 cents to $1.93 per share.

The Zacks Consensus Estimate for first-quarter 2026 revenues and loss per share is pegged at $206.1 million and 33 cents, respectively.

Some better-ranked stocks from the broader medical space are Intuitive Surgical ISRG, Phibro Animal Health PAHC and GE HealthCare Technologies GEHC.

Intuitive Surgical, sporting a Zacks Rank #1 (Strong Buy) at present, reported fourth-quarter 2025 adjusted earnings per share (EPS) of $2.53, beating the Zacks Consensus Estimate by 12.4%. Revenues of $2.87 billion surpassed the Zacks Consensus Estimate by 4.7%. You can see the complete list of today’s Zacks #1 Rank stocks here.

ISRG’s earnings per share estimate for 2026 has moved up 46 cents to $10.07 in the past 60 days. The company beat earnings estimates in the trailing four quarters, the average surprise being 13.2%.

Phibro Animal Health, currently flaunting a Zacks Rank #1, reported second-quarter 2025 adjusted EPS of 87 cents, which surpassed the Zacks Consensus Estimate by 26.1%. Revenues of $373.9 million beat the Zacks Consensus Estimate by 4.7%.

PAHC’s earnings per share estimate for 2026 has moved up 26 cents to $3.02 in the past 60 days. The company’s earnings beat estimates in the trailing four quarters, the average surprise being 20.1%.

GE HealthCare Technologies, currently carrying a Zacks Rank #2 (Buy), reported fourth-quarter 2025 adjusted EPS of $1.44, which surpassed the Zacks Consensus Estimate by 0.7%. Revenues of $5.7 billion beat the Zacks Consensus Estimate by 1.9%.

GEHC’s earnings per share estimate for 2026 has moved up 6 cents to $4.99 in the past 60 days. The company beat earnings estimates in the trailing four quarters, the average surprise being 7.5%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-18 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite