|

|

|

|

|||||

|

|

|

Over the past six months, Terex has been a great trade, beating the S&P 500 by 21.8%. Its stock price has climbed to $67.22, representing a healthy 26.9% increase. This run-up might have investors contemplating their next move.

Is now the time to buy Terex, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Despite the momentum, we don't have much confidence in Terex. Here are three reasons there are better opportunities than TEX and a stock we'd rather own.

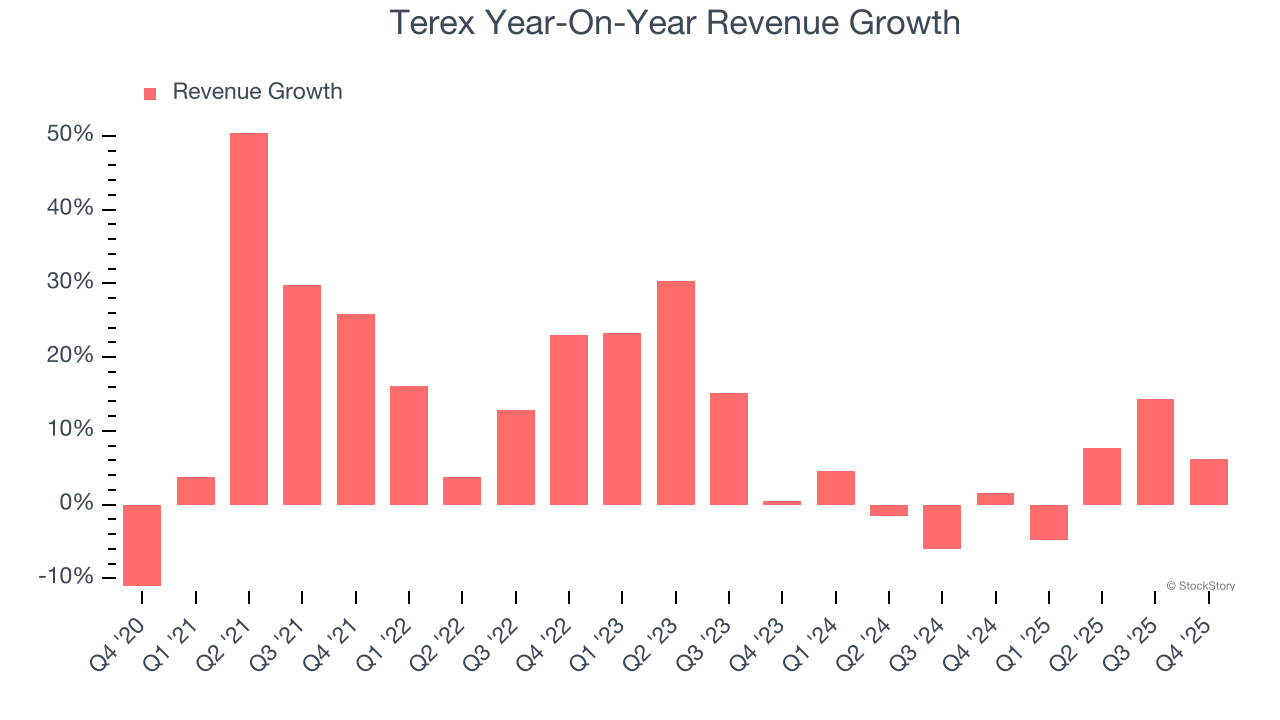

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Terex’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 2.6% over the last two years was well below its five-year trend.

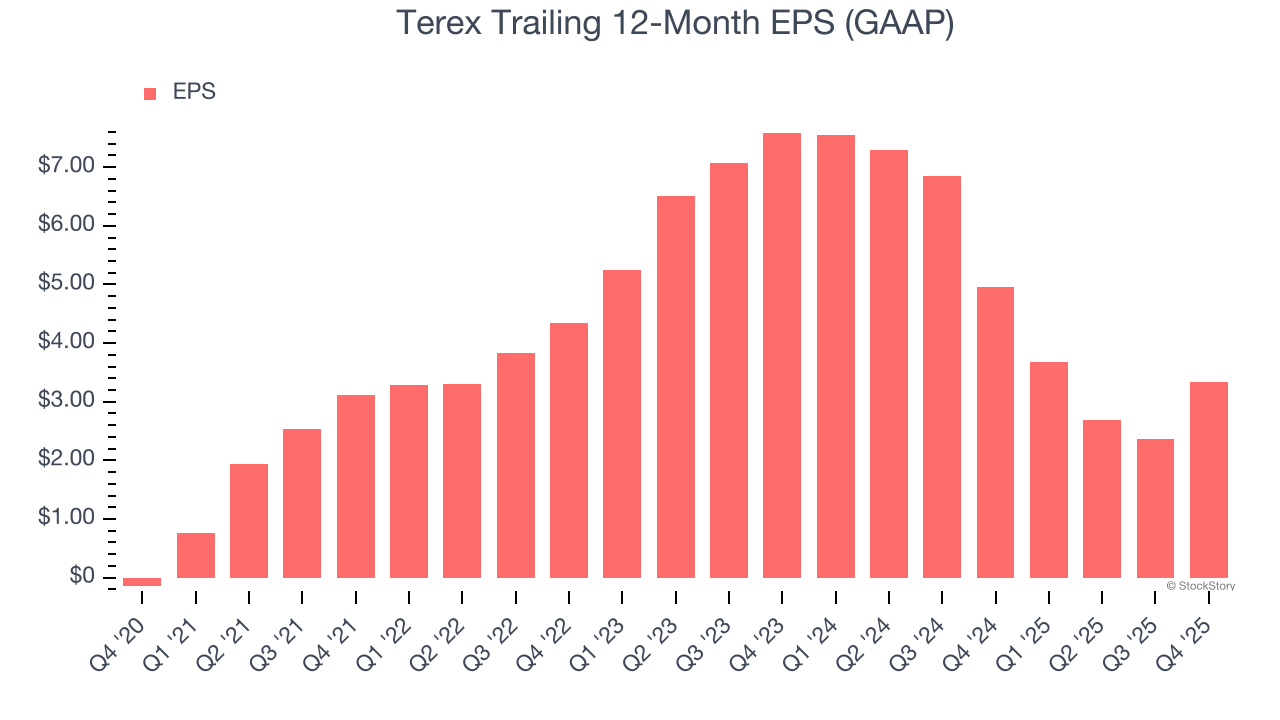

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Terex, its EPS declined by 33.7% annually over the last two years while its revenue grew by 2.6%. This tells us the company became less profitable on a per-share basis as it expanded.

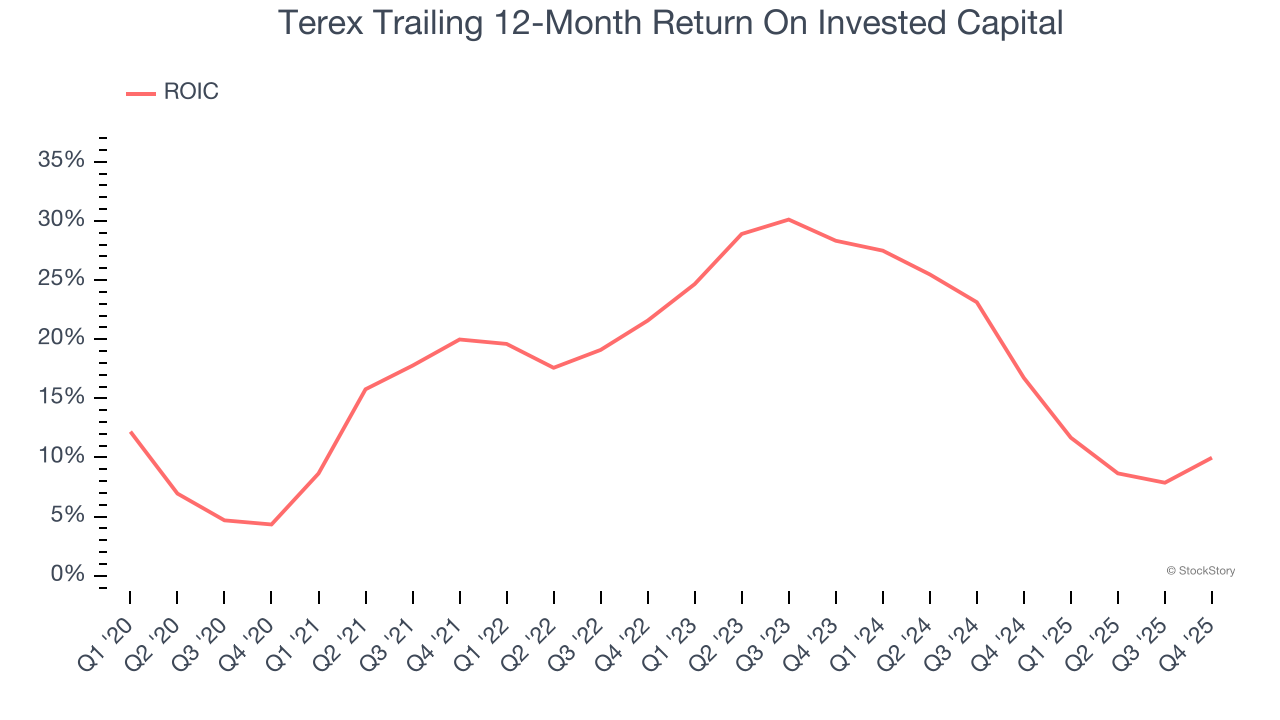

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Terex’s ROIC has unfortunately decreased. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Terex’s business quality ultimately falls short of our standards. With its shares topping the market in recent months, the stock trades at 13.8× forward P/E (or $67.22 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Jul-23 | |

| Jul-22 | |

| Jul-20 | |

| Jul-15 | |

| Jul-14 | |

| Jul-08 | |

| Jul-03 | |

| Jul-02 | |

| Jul-01 | |

| Jun-26 | |

| Jun-25 | |

| Jun-23 | |

| Jun-18 | |

| Jun-15 | |

| Jun-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite