|

|

|

|

|||||

|

|

|

Over the past six months, AutoNation’s stock price fell to $195.73. Shareholders have lost 13.7% of their capital, which is disappointing considering the S&P 500 has climbed by 5.1%. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in AutoNation, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons why AN doesn't excite us and a stock we'd rather own.

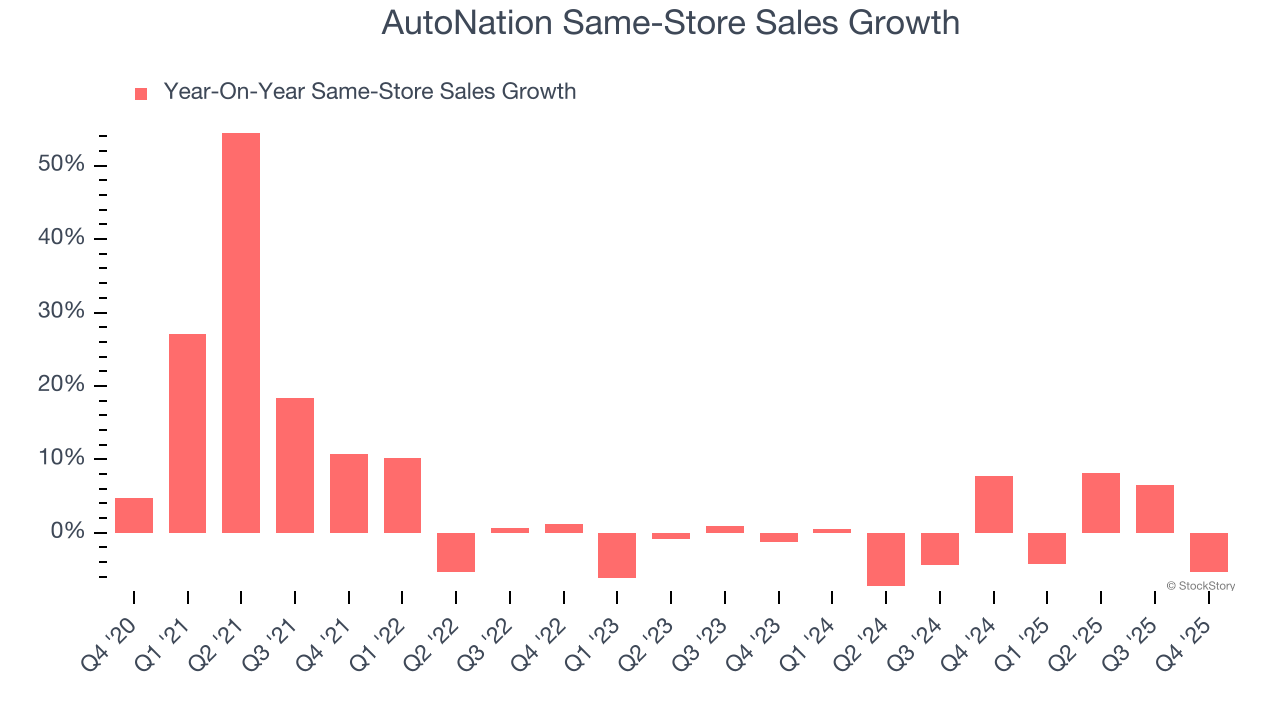

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

AutoNation’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat.

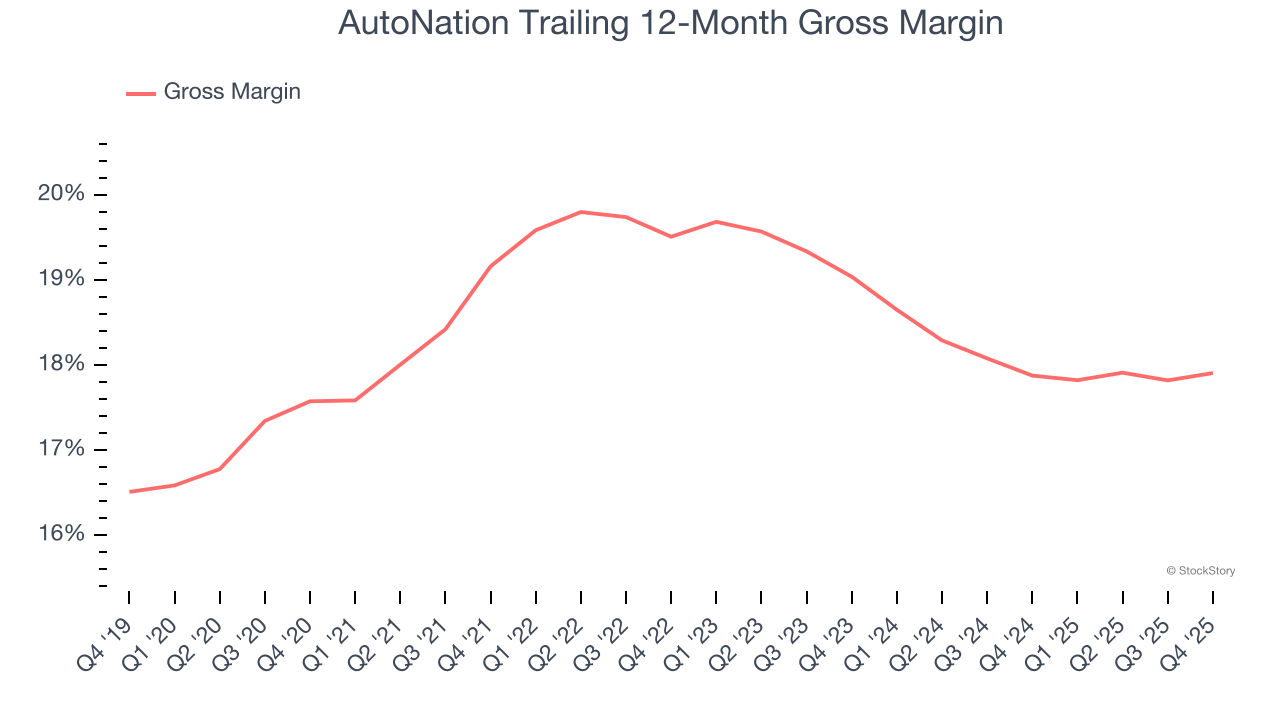

Gross profit margins are an important measure of a retailer’s pricing power, product differentiation, and negotiating leverage.

AutoNation has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 17.9% gross margin over the last two years. That means AutoNation paid its suppliers a lot of money ($82.11 for every $100 in revenue) to run its business.

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

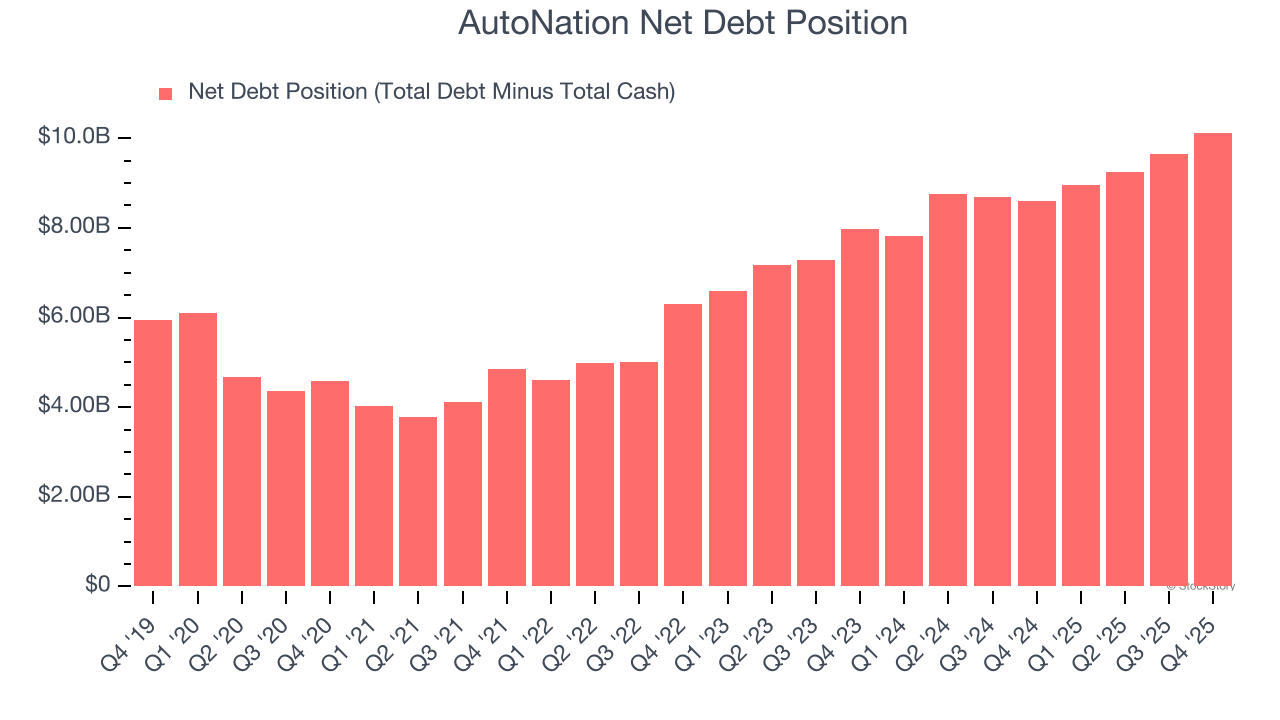

AutoNation burned through $197.5 million of cash over the last year, and its $10.18 billion of debt exceeds the $58.6 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the AutoNation’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of AutoNation until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

We see the value of companies helping consumers, but in the case of AutoNation, we’re out. Following the recent decline, the stock trades at 9.1× forward P/E (or $195.73 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. We’d suggest looking at one of our all-time favorite software stocks.

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-14 | |

| Jul-10 | |

| Jun-23 | |

| Jun-18 | |

| Jun-17 | |

| Jun-09 | |

| May-27 | |

| May-02 | |

| May-01 | |

| May-01 | |

| May-01 | |

| Apr-10 | |

| Apr-09 | |

| Mar-05 | |

| Mar-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite