|

|

|

|

|||||

|

|

|

As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the water infrastructure industry, including Watts Water Technologies (NYSE:WTS) and its peers.

Trends towards conservation and reducing groundwater depletion are putting water infrastructure and treatment products front and center. Companies that can innovate and create solutions–especially automated or connected solutions–to address these thematic trends will create incremental demand and speed up replacement cycles. On the other hand, water infrastructure and treatment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 5 water infrastructure stocks we track reported a slower Q4. As a group, revenues missed analysts’ consensus estimates by 4.5%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 12.6% since the latest earnings results.

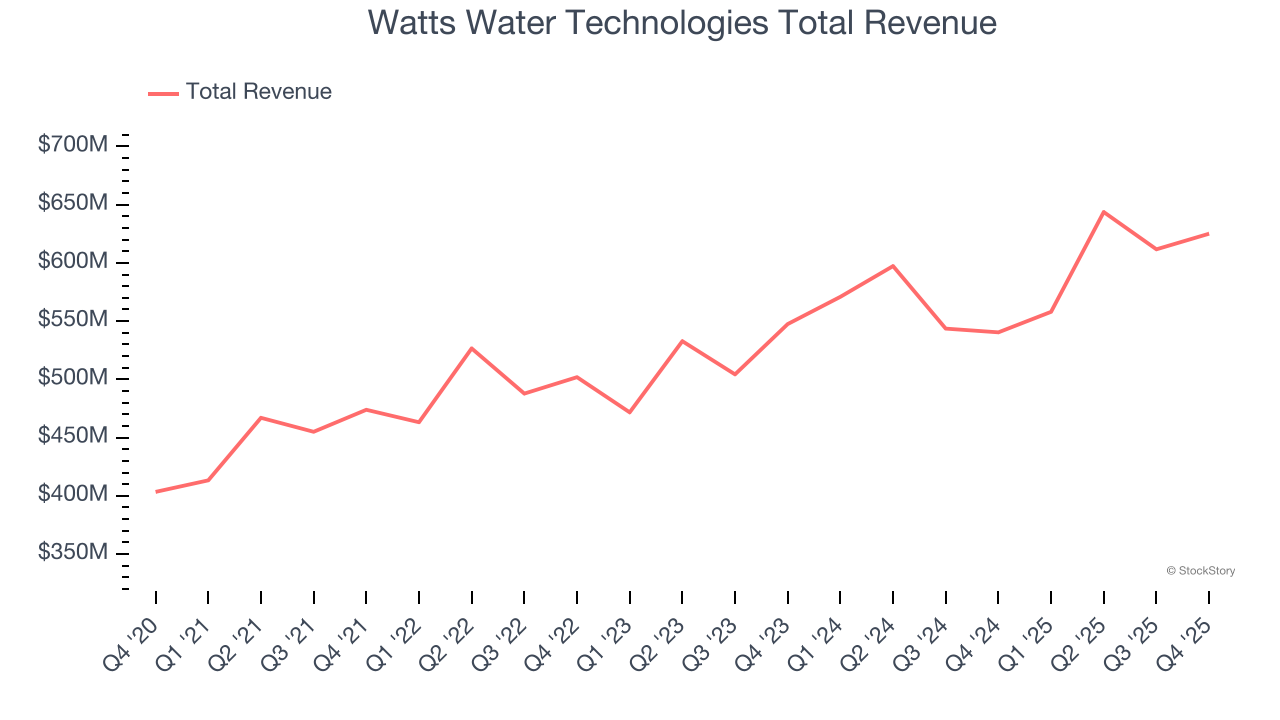

Founded in 1874, Watts Water (NYSE:WTS) specializes in manufacturing water products and systems for residential, commercial, and industrial applications globally.

Watts Water Technologies reported revenues of $625.1 million, up 15.7% year on year. This print exceeded analysts’ expectations by 2.3%. Overall, it was an exceptional quarter for the company with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ adjusted operating income estimates.

Chief Executive Officer Robert J. Pagano Jr. said, “I would like to recognize the Watts team for their hard work and dedication, which resulted in record fourth quarter and full year 2025 performance, including record sales, operating income and earnings per share. In addition, we continued to meet our customers’ needs for innovative solutions that address their greatest water safety, water conservation and energy efficiency challenges. We also successfully executed on our goals to develop differentiated products and further enhance productivity through the One Watts Performance System.”

Watts Water Technologies scored the biggest analyst estimates beat and fastest revenue growth of the whole group. The results were likely priced in, however, and the stock is flat since reporting. It currently trades at $313.19.

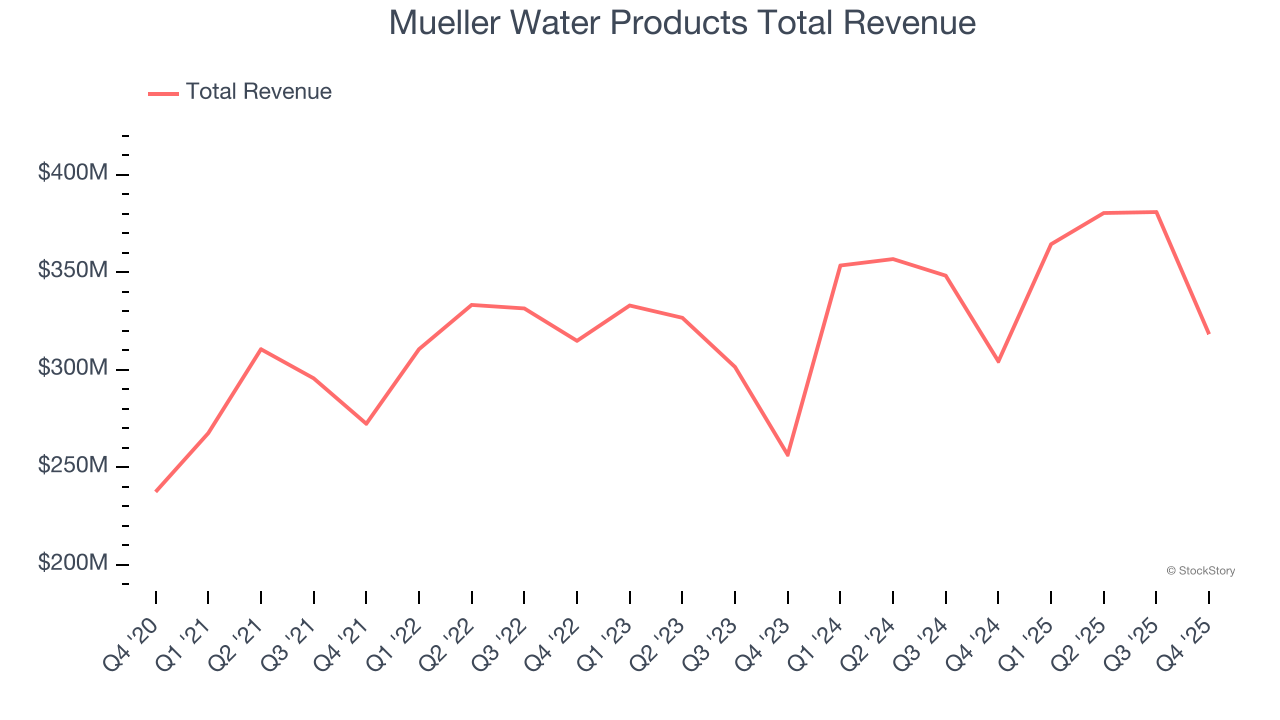

As one of the oldest companies in the water infrastructure industry, Mueller (NYSE:MWA) is a provider of water infrastructure products and flow control systems for various sectors.

Mueller Water Products reported revenues of $318.2 million, up 4.6% year on year, outperforming analysts’ expectations by 2%. The business had a very strong quarter with a solid beat of analysts’ adjusted operating income estimates and full-year EBITDA guidance beating analysts’ expectations.

The market seems content with the results as the stock is up 4.9% since reporting. It currently trades at $28.88.

Is now the time to buy Mueller Water Products? Access our full analysis of the earnings results here, it’s free.

Having saved far more than a trillion gallons of water, Energy Recovery (NASDAQ:ERII) provides energy recovery devices to the water treatment, oil and gas, and chemical processing sectors.

Energy Recovery reported revenues of $66.87 million, flat year on year, falling short of analysts’ expectations by 19%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ EBITDA estimates.

Energy Recovery delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 33.3% since the results and currently trades at $10.75.

Read our full analysis of Energy Recovery’s results here.

Formed through a spinoff, Xylem (NYSE:XYL) manufactures and services engineered products across a wide variety of applications primarily in the water sector.

Xylem reported revenues of $2.40 billion, up 6.3% year on year. This result topped analysts’ expectations by 1.1%. Overall, it was a strong quarter as it also recorded an impressive beat of analysts’ organic revenue estimates and a solid beat of analysts’ EBITDA estimates.

Xylem had the weakest full-year guidance update among its peers. The stock is down 9.6% since reporting and currently trades at $126.70.

Read our full, actionable report on Xylem here, it’s free.

As the world’s largest manufacturer of autonomous mobile robots, Tennant (NYSE:TNC) designs, manufactures, and sells cleaning products to various sectors.

Tennant reported revenues of $291.6 million, down 11.3% year on year. This number missed analysts’ expectations by 9%. Overall, it was a disappointing quarter as it also produced full-year EBITDA guidance missing analysts’ expectations significantly and a significant miss of analysts’ revenue estimates.

Tennant scored the highest full-year guidance raise but had the slowest revenue growth among its peers. The stock is down 24.6% since reporting and currently trades at $62.05.

Read our full, actionable report on Tennant here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

| Jul-09 | |

| Jul-08 | |

| Jun-16 | |

| Jun-15 | |

| Jun-04 | |

| May-12 | |

| May-06 | |

| May-06 | |

| May-04 | |

| Apr-28 | |

| Apr-27 | |

| Apr-22 | |

| Apr-08 | |

| Apr-04 | |

| Mar-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite