|

|

|

|

|||||

|

|

|

Buying strong, best-in-class technology and artificial intelligence stocks into weakness is something long-term investors should consider doing to start March.

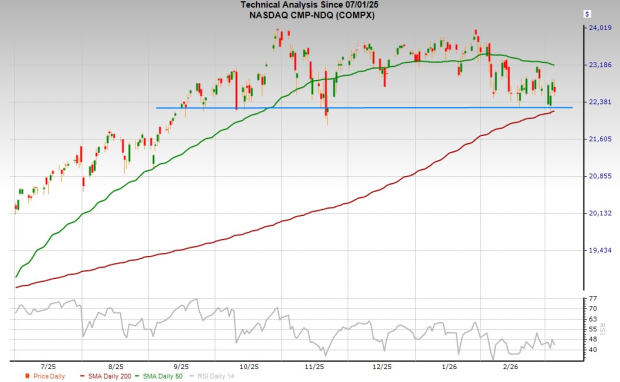

The bulls stepped up and bought stocks to defend the Nasdaq’s 200-day moving average mid-week despite escalating attacks in Iran and the surrounding region.

Of course, a lot could change over the weekend and in the coming days and weeks given the dynamic and rapidly evolving situation in the Middle East.

No matter what happens in the near-term, investors must remember that buying stocks amid downturns and chaotic times is a proven strategy over the long haul.

Wall Street has also largely shrugged off other conflicts in recent years.

It is time for investors to cut through the noise and look to the facts on the ground. The two things that move the market—earnings and interest rates—are supporting stocks.

Nvidia’s Q4 report and outlook confirmed what Wall Street already knew. Despite some AI bubble worries, the spending spree is heating up.

AI chip manufacturer Taiwan Semi was the first big tech firm to raise its 2026 capex guidance back in early January to between $52 billion and $56 billion, blowing away 2025’s $40.9 billion.

AI hyperscalers are projected to spend roughly $530 billion in capex this year, up from around $400 billion last year. This figure is likely to keep climbing after the stellar stretch of guidance from the Mag 7 and beyond.

The chart below highlights that the outlook for Q1 2026 Tech sector earnings has surged to 24% up from 18% in mid-January and 12% back in early October.

Wall Street is also excited that earnings growth is spreading across nearly every pocket of the economy, with 15 out of 16 Zacks sectors set to post YoY EPS expansion in 2026.

On the interest rate front, the big money is still betting that the Fed will cut rates again in the back half of 2026.

Now let’s dive into two AI-focused tech stocks for investors to buy on the dip in March.

We are starting with the hardest hit of the two AI stocks, ServiceNow NOW, which is down nearly 50% from its January 2025 highs. This means it offers around 100% upside if it were to return to those levels at some future date.

NOW is a perfect example of the AI-based disruption crushing software companies. But the digital workflow services and solutions firm already expanded deeply into AI over the last several years to boost ServiceNow's appeal to enterprise customers racing to innovate.

ServiceNow, which designs software for IT, customer service, HR, and other business operations, is rapidly adapting to AI. The company boasts that it’s transformed into the “AI control tower for business reinvention.”

ServiceNow is also working directly with AI leaders to incorporate their offerings directly into NOW’s portfolio. NOW announced in January that it deepened its multi-year deal with OpenAI to help it “power agentic AI experiences and accelerate enterprise AI outcomes.”

The company is also actively expanding its partnership with Anthropic to further integrate Claude models more deeply into the ServiceNow AI Platform.

Wall Street might be worried about AI eating software’s lunch. But ServiceNow is effectively integrating AI into its business, while making deals with some of the biggest AI innovators. Its 2025 growth and NOW's outlook showcase a company flexing its expansion muscles.

The software firm posted its fourth-straight year of between 21% to 24% sales growth in 2025, reaching $13.28 billion (easily doubling its 2021 total). This growth followed a period of even stronger 30% or higher expansion.

ServiceNow said it had 244 transactions over $1 million in net new annual contract value in Q4 2025, up 40% YoY. It ended 2025 with over 600 customers with more than $5 million in ACV, up 20% vs. 2024.

NOW grew its GAAP earnings by 22% to $1.67 a share, up from just $0.23 in 2021, with its adjusted EPS 27% higher. The chart below highlights NOW's impressive long-term earnings growth outlook.

Image Source: Zacks Investment Research

ServiceNow is projected to grow its revenue by 20% in 2026 and 18% in 2027 to help boost its adjusted earnings by 18% and 20%, respectively. Plus, its earnings estimates have improved since its Q4 release at the end of January.

ServiceNow flexed its financial firepower and sturdy balance sheet when it announced an additional $5 billion under its share repurchase program. CEO Bill McDermott also bought $3 million worth of NOW shares recently, saying there was “no better entry point.”

Image Source: Zacks Investment Research

NOW shares have more than tripled the Tech sector since it went public in 2012, soaring roughly 2,300%. This massive run includes its 50% tumble from its 2025 highs. The tech stock found some support recently at the technical range highlighted above after hitting its most oversold RSI levels in the past decade.

Thursday’s jump pushed it just below its 50-day moving average. Investors who buy NOW stock have a chance to nearly double their money if it eventually returns to its 2025 highs—(its average Zacks price target offers roughly 70% upside).

Celestica Inc. CLS is a leading technology manufacturing powerhouse that designs and builds high-tech electronic solutions for AI data center infrastructure and other advanced technologies. CLS struggled for years following its late 1990s IPO. But the AI arms race helped Celestica flip the script completely.

CLS is a behind-the-scenes tech manufacturing powerhouse that designs and builds high-tech electronics like super-fast AI servers, networking switches, and data-center hardware for giant customers, including multiple AI hyperscalers. The electronics manufacturing company also benefits from the long-term upside across aerospace and defense, telecom, healthcare tech, supply chain solutions, and beyond.

The data center infrastructure standout grew its revenue by 29% in 2025 to $12.39 billion, extending its run of huge AI-boosted expansion. In fact, CLS more than doubled its revenue between 2021 and 2025. Plus, it grew its adjusted earnings by 56% last year and its GAAP EPS by over 90%, after averaging 65% GAAP EPS growth between 2021 and 2024.

Celestica issued robust guidance for 2026 in late January as “demand for AI-related data center technologies continues to strengthen.” CLS expects its 2026 revenue growth trajectory to be “sustained into 2027.”

CEO Rob Mionis said in prepared Q4 remarks that CLS is continuing support its customers' long-term AI infrastructure investments. This backdrop is why CLS is increasing its planned capital investments to $1 billion in 2026, which it expects to fully fund organically through its operating cash flow.

The pick-and-shovels AI stock is projected to grow its revenue by 37% in 2026 and 39% in 2027 to reach $23.66 billion, nearly double 2025’s $12.39 billion.

Celestica is projected to expand its adjusted earnings by 46% and 43%, respectively. The company’s post-Q4 earnings revisions help it earn a Zacks Rank #2 (Buy). Plus, 15 of the 18 brokerage recommendations Zacks has for CLS are “Strong Buys.”

The behind-the-scenes AI stock has skyrocketed ~3,000% in the past five years, crushing the Zacks Tech sector’s 100%. This run includes a 220% climb in the past 12 months.

Investors who missed that rally have an opportunity to buy Celestica down roughly 25% from its November highs. Meanwhile, its average Zacks price target represents 34% upside from its current price.

Celestica’s recent pullback, coupled with its stellar earnings growth outlook, has Celestica trading 50% below its highs at 30.0X forward 12-month earnings. CLS found buyers at its pre-October breakout highs and its 200-day moving average earlier this week.

Now might be the time for traders and long-term investors to buy this growth-heavy AI infrastructure stock at a potentially huge discount.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 7 hours | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite