|

|

|

|

|||||

|

|

|

China-based EV company NIO Inc. NIO is slated to release fourth-quarter 2025 results on March 10, before the opening bell. The Zacks Consensus Estimate for the to-be-reported quarter is pegged at a loss of 5 cents a share on revenues of $4.61 billion.

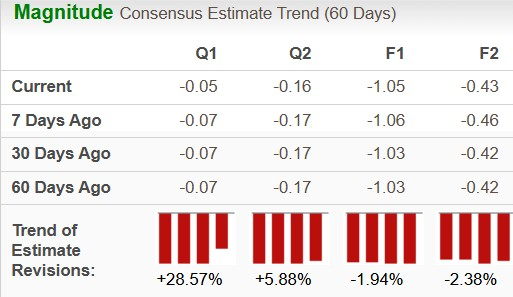

The loss estimate for the fourth quarter of 2025 has narrowed by 2 cents over the past seven days. The bottom-line projection indicates an improvement from a loss of 47 cents reported in the year-ago period. The Zacks Consensus Estimate for quarterly revenues suggests year-over-year growth of roughly 71%.

The Zacks Consensus Estimate for NIO’s 2025 revenues is pegged at $12.6 billion, implying a rise of 38% year over year. The consensus mark for the 2025 bottom line is pegged at a loss of $1.05 per share, indicating an improvement from a loss of $1.51/share incurred in 2024. For 2026, the consensus mark for NIO’s top and bottom line implies an improvement of 47% and 59%, respectively, from projected 2025 levels.

In the trailing four quarters, NIO surpassed EPS estimates once and missed thrice, with the average negative earnings surprise being 35.29%.

NIO Inc. price-eps-surprise | NIO Inc. Quote

Our proven model does not conclusively predict an earnings beat for NIO this season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

NIO has an Earnings ESP of 0.00% and a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

For the three months ended Dec 31, NIO delivered 124,807 vehicles, which marked a new quarterly high. The figure increased 72% on a year-over-year basis. In the fourth quarter, the namesake brand sold 67,433 cars. Meanwhile, ONVO and Firefly brands delivered 38,290 and 19,084 units, respectively. ONVO and Firefly brands have diversified NIO’s product portfolio, with sales gaining momentum.

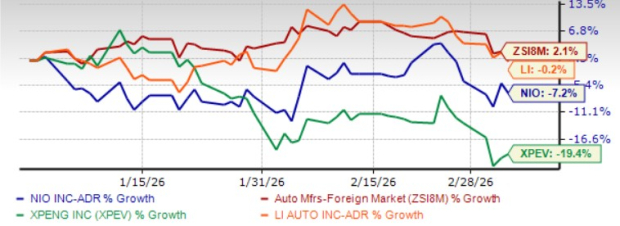

By contrast, delivery momentum at close peers was less impressive. Li Auto’s LI fourth-quarter 2025 deliveries fell to 109,194 units, down sharply from 158,696 units a year earlier. XPeng, Inc. XPEV delivered 116,249 vehicles, up 27% year over year but still below the lower end of its own guidance.

NIO’s revenues for the quarter to be reported are expected to have benefited from increased deliveries. Amid the volume ramp-up and cost optimization of components and supply chains, vehicle margins are on an upward trend. The metric grew to 14.7% in the third quarter of 2025 from 13.1% in the third quarter of 2024.

Encouragingly, NIO guided for its first-ever quarterly adjusted operating profit for the fourth quarter of 2025. NIO expects adjusted operating profit between 700 million and 1.2 billion yuan, implying a sharp reversal from the 5.54 billion yuan adjusted operating loss reported in the fourth quarter of 2024.

The improvement is being driven by a combination of strong delivery growth, a better product mix, and tighter operational discipline. NIO has been broadening its addressable market by expanding beyond its premium roots. The launch of the more affordable Onvo brand, alongside the high-end small-car brand Firefly, is helping the company attract new customers and generate incremental volume in a highly competitive EV market.

Year to date, shares of NIO have declined 7%, underperforming the industry and Li Auto, while outperforming XPeng.

From a valuation perspective, NIO currently trades at a forward price-to-sales ratio of 0.53, below the industry’s 0.62 as well as Li Auto’s 0.94 and XPeng’s 1.06.

NIO appears to be entering a stronger growth phase, supported by momentum across its products, technology and global expansion strategy. The company now offers one of the broadest EV portfolios among Chinese automakers, including models such as ES6, ES8, ET5, ET7, EC6 and EC7, along with newer vehicles under the Onvo and Firefly brands. This wide lineup allows NIO to target multiple price points and customer segments.

Deliveries reached 326,028 vehicles in 2025, up nearly 47% year over year, marking strong demand across all three brands. The momentum has carried into 2026, with deliveries in the first two months of the year rising sharply, led by the third-generation ES8. The company has also crossed the key milestone of one million cumulative deliveries.

Margins are also showing improvement as higher volumes and supply-chain efficiencies lower costs. Management is targeting vehicle margins of around 20% over time, supported by upcoming launches of three premium large SUVs that could benefit from pricing strength and platform synergies.

Another key differentiator is NIO’s battery-swap ecosystem. The company has completed more than 100 million battery swaps and operates nearly 3,800 swap stations globally, with further expansion planned. Beyond China, NIO is expanding into Central Asia, Australia, New Zealand and multiple European markets. At the same time, software upgrades like the NIO WorldModel are enhancing assisted driving and safety features, strengthening user engagement and brand loyalty.

However, risks remain due to intense competition from players like Tesla, BYD Company, Li Auto and XPeng. In addition, NIO’s relatively high leverage limits financial flexibility. Still, improving execution and clearer profitability visibility support its long-term outlook. As such, investors should hold onto NIO stock.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-29 | |

| Jul-28 | |

| Jul-27 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-16 | |

| Jul-16 |

Chinese Automaker XPeng Unveils L03 SUV in Munich, Steps Up Overseas Expansion

XPEV

The Wall Street Journal

|

| Jul-16 | |

| Jul-15 | |

| Jul-15 |

XPeng Aims to Produce Over 1,000 Robots a Month as It Plans Global Rollout

XPEV

The Wall Street Journal

|

| Jul-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite