|

|

|

|

|||||

|

|

|

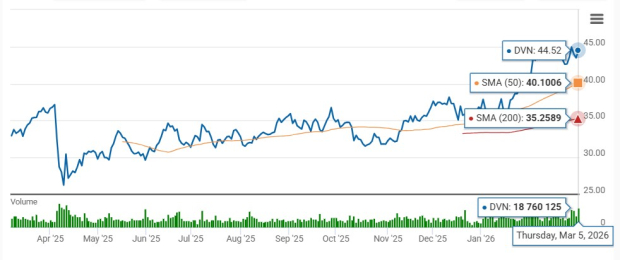

Devon Energy Corporation’s DVN shares have gained 29% in the past six months, outperforming the Zacks Oil & Gas- Exploration and Production- United States industry’s return of 14% and the broader Zacks Oil and Energy sector’s 26.7%. The company has also outperformed the S&P 500’s 6.9% return in the same time period.

Devon Energy benefits from its high-quality multi-basin assets, cost-management initiatives, debt management and strategic investments to upgrade and expand its existing assets. Yet, the competitive oil and gas industry and fluctuating oil and gas prices are posing challenges to the company.

Another stock from the same industry, Diamondback Energy FANG, is having focus of the Permian Basin. This exploration and production company registered a 30.4% gain in the past six months.

The 50 and 200-day SMAs are key indicators for traders and analysts to identify support and resistance levels. It is considered particularly important as this is the first marker of an uptrend or downtrend of the stocks.

Should you consider adding DVN to your portfolio only based on positive price movements? Let’s delve deeper and find out the factors that can help investors decide whether it is a good entry point to add DVN stock to their portfolio.

Devon Energy has a strong U.S. operational presence across key oil regions, including the Delaware Basin, Eagle Ford, Anadarko Basin, Rockies and Powder River Basin. Production rates from newly drilled wells have continued to improve across these five U.S. oil plays. Moreover, faster cycle times, production optimization efforts and ongoing cost-reduction initiatives are helping the company reduce breakeven costs across its asset portfolio.

Devon Energy has pursued a disciplined acquisition strategy to expand its asset base, boost operational scale and enhance shareholder returns. DVN is expected to complete an all-stock merger with Coterra Energy in mid-2026. The combined company would produce more than 1.6 million Boe/d and hold nearly 750,000 net acres in the core of the Delaware Basin, supporting longer laterals and lower costs. The deal is projected to generate $1 billion in annual pre-tax synergies by year-end 2027 through operational optimization and the elimination of duplicate services.

Devon Energy continues to strengthen profitability through its low-cost operating strategy. By divesting higher-cost assets and focusing on more efficient, lower-cost production, the company has significantly improved its cost structure. Ongoing efforts to reduce drilling and completion expenses, along with workforce optimization aligned with strategic priorities, are further supporting Devon Energy’s strong operating margins.

Devon Energy also benefits from a balanced commodity mix, with exposure to oil, natural gas and natural gas liquids. The company continues to focus on strengthening its portfolio by adding high-quality resource assets.

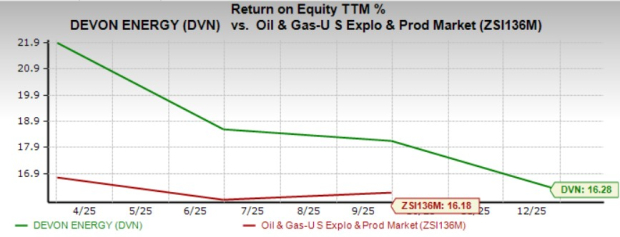

The return on equity (“ROE”) measures how well a company generates returns from the shareholders’ equity. ROE indicates how well management utilizes investors' funds to expand the business.

Devon Energy’s ROE has outperformed the industry average in the trailing 12 months. ROE of DVN was 16.28% compared with the industry average of 16.18%.

Another company, Occidental Petroleum OXY, operating in the same sector, is generating returns lower than its industry. ROE of OXY is currently pegged at 9.89% lower than the industry level.

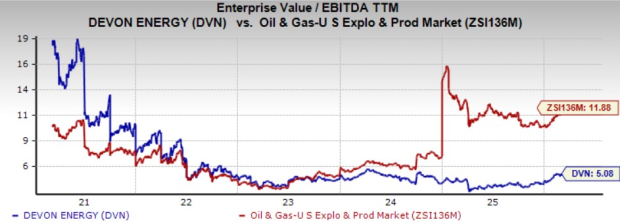

Devon Energy is currently trading at a discount relative to its industry based on the trailing 12-month Enterprise Value to EBITDA (EV/EBITDA TTM) basis. DVN’s current valuation of 5.08X is lower than the industry average of 11.88X and it is trading above the five-year median of 4.79X.

Diamondback Energy is presently trading at an EV/EBITDA TTM of 7.97X, a discount compared with the industry.

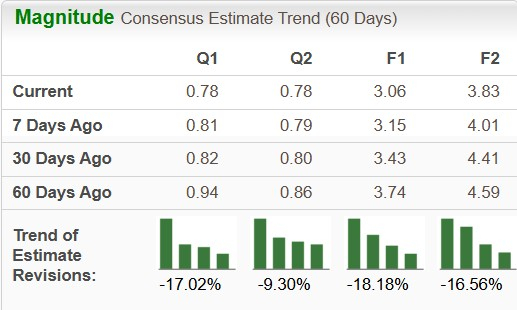

The Zacks Consensus Estimate for Devon Energy’s 2026 and 2027 earnings per share has decreased 18.18% and 16.56%, respectively, in the past 60 days.

The Zacks Consensus Estimate for Occidental Petroleum’s 2026 earnings per share has increased 5.79% and the same for 2027 EPS decreased 5.74% in the past 60 days.

Devon Energy gains significant value from its diverse multi-basin asset portfolio, which delivers strong free cash flow and supports ongoing balance sheet improvement. The company’s well-balanced production mix across oil, natural gas and NGLs further enhances operational flexibility and strengthens its competitive position.

Despite a negative revision in earnings estimates, investors can remain invested in the Zacks Rank #3 (Hold) stock as it is currently trading at a discount and has a better ROE than the industry.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 59 min | |

| 3 hours | |

| 3 hours | |

| Jul-22 | |

| Jul-20 | |

| Jul-18 | |

| Jul-14 | |

| Jul-12 | |

| Jul-09 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite