|

|

|

|

|||||

|

|

|

Restaurant operators continue to face a challenging backdrop marked by cautious consumer spending, intense competition and ongoing cost pressures. In this environment, Rave Restaurant Group, Inc. RAVE and Papa John's International, Inc. PZZA operate within the same quick-service pizza category but follow notably different business models. RAVE runs a largely franchise-driven platform centered on its Pizza Inn and Pie Five brands, with revenue generated mainly through franchise royalties, supplier incentives and related franchise fees rather than direct restaurant operations. Papa John’s, by contrast, operates a much larger global system that includes both company-owned and franchised restaurants, supported by commissary operations that produce and distribute key ingredients across its network.

With both companies participating in the competitive pizza segment but relying on different operating structures and scale, investors may want to assess how each model positions the business in the current environment. Let’s take a closer look.

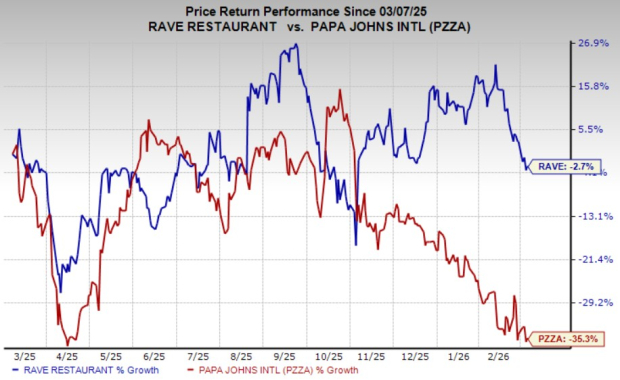

RAVE (down 5.1%) has outperformed PZZA (down 24.6%) over the past three months. In the past year, Rave Restaurant stock has lost 2.7% compared with Papa John’s loss of 35.3%.

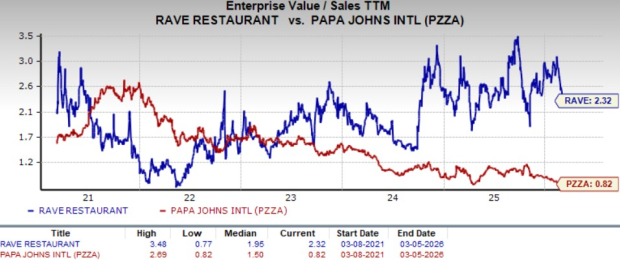

Meanwhile, RAVE is trading at a trailing 12-month enterprise value-to-sales (EV/S) ratio of 2.3X, above its median of 1.9X over the past five years. PZZA’s trailing 12-month EV/S multiple sits at 0.8X, below its last five-year median of 1.5X. While PZZA appears cheap when compared with the Zacks Retail-Wholesale sector average of 1.7X, RAVE seems to be expensive.

Rave Restaurant’s core Pizza Inn brand continues to serve as the primary engine of system performance. The brand has delivered positive comparable store sales growth and modest increases in domestic retail sales, supported by stable buffet operations and ongoing promotional initiatives aimed at driving traffic. Management has also focused on expanding the Pizza Inn buffet footprint, opening new locations and strengthening its development pipeline. These efforts, combined with the brand’s value-driven offerings and focus on family-oriented dining, have supported steady system sales and contributed to continued profitability.

RAVE operates a predominantly franchise-based model in which revenues are generated through franchise royalties, licensing fees and supplier incentives tied to franchisee sales. Because franchisees purchase food and supplies through authorized distributors, the company benefits from supplier and distributor incentive revenues linked to overall system retail sales. This structure allows Rave Restaurant to leverage systemwide sales growth without bearing the full operating costs of restaurant ownership, helping maintain stable revenue streams and operating efficiency.

Another factor supporting investor confidence is the company’s strong financial position. Rave Restaurant has maintained consistent profitability and generates cash from operating activities while keeping a conservative balance sheet. The company reported continued profitability in recent quarters, supported by improved sales at Pizza Inn and disciplined expense management. With no debt and meaningful liquidity, RAVE remains well positioned to support franchise development initiatives and sustain operations in a competitive restaurant environment.

Papa John’s operates a large global restaurant system that combines company-owned locations with a significantly larger base of franchised restaurants across North America and international markets. This structure allows the company to expand its footprint while generating royalty revenues and franchise-related income from systemwide sales. The brand continues to pursue restaurant development through franchise partnerships and market expansion, which supports long-term growth and increases overall brand presence in key markets.

Another key driver of Papa John’s business is its vertically integrated supply chain. The company operates regional production and distribution centers that supply dough, sauces and other key ingredients to restaurants across its network. This system helps maintain consistent product quality while supporting operational efficiency and cost management throughout the restaurant system. By controlling key elements of ingredient production and distribution, PZZA strengthens brand consistency and enhances support for both company-owned and franchised locations.

Papa John’s strategy emphasizes strengthening its brand proposition while expanding product innovation and customer engagement. The company continues to invest in marketing initiatives, digital ordering capabilities and technology platforms designed to enhance the customer experience and improve operational efficiency. With a significant portion of sales occurring through digital channels, these investments support customer acquisition, loyalty and long-term system growth.

While both Rave Restaurant and Papa John’s operate in the same pizza category, their recent market performance and valuations highlight differing investor perceptions. RAVE has held up better in the market over both recent months and the past year, suggesting that investors are showing increasing confidence in its franchise-heavy, asset-light structure and its ability to generate stable cash flows with limited direct operating exposure. That stronger relative performance has also pushed the stock to trade at a richer valuation compared with its historical levels, indicating that the market is already pricing in some of its operational stability and steady execution.

Papa John’s, on the other hand, has seen significantly weaker stock performance over the same period. Shares currently trade at a noticeably discounted valuation relative to both their historical range and broader industry benchmarks. While such a discount could signal potential upside if operational momentum improves, it also reflects investor caution around the company’s execution challenges, competitive pressures and ongoing investments aimed at repositioning the business.

For investors, the contrast essentially comes down to stability versus turnaround potential. RAVE offers a more predictable model supported by franchising and disciplined operations, while PZZA may require clearer evidence of sustained improvement before sentiment shifts meaningfully.

Given its stronger relative momentum and more stable operating structure, RAVE currently appears to be the better buy among the two pizza restaurant stocks.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-21 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-02 | |

| Jul-02 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-25 | |

| Jun-17 | |

| Jun-17 | |

| Jun-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite