|

|

|

|

|||||

|

|

|

Shares of Palantir Technologies PLTR have been volatile lately, falling 16% over the past three months but rebounding with a 12% gain in the past month. This recent uptick suggests the stock may be regaining momentum after a period of weakness over the last six months.

To better understand whether the investment thesis remains intact, it is worth taking a closer look at Palantir’s technology capabilities, its financial execution and the trajectory of its long-term growth.

At the heart of Palantir’s strategy is its Artificial Intelligence Platform, which allows organizations to structure, integrate, and govern complex datasets so AI systems can operate effectively. Enterprises typically struggle with fragmented data across finance, operations, supply chains and human resources. PLTR solves this problem using an ontology-based architecture that creates a digital twin of an organization’s operations.

This design enables AI to interact directly with business workflows rather than producing disconnected insights. As a result, Palantir is positioned on the demand side of the AI economy, where monetization depends on execution and outcomes rather than raw computing power. This distinction is increasingly important as enterprises shift from AI experimentation to production-scale deployments.

Foundry has become Palantir’s primary growth engine in the commercial market. The platform integrates data from ERP systems, IoT sensors, and enterprise databases using more than 200 prebuilt connectors. Automated, low-code pipelines allow companies to unify structured and unstructured data quickly, while embedded analytics and machine learning tools support use cases such as supply chain optimization, fraud detection and predictive maintenance.

The commercial momentum behind Foundry is accelerating rapidly. In the most recent quarter, Palantir’s U.S. commercial revenues surged 137% year over year, highlighting growing enterprise demand for operational AI solutions. Overall, U.S. revenues rose 93% year over year, significantly outpacing international growth and reinforcing the strength of the domestic market.

Customer expansion is also deepening. Palantir closed 61 deals exceeding $10 million in value during the quarter.

While Foundry fuels commercial expansion, Gotham remains a cornerstone of Palantir’s business. Gotham is designed for mission-critical intelligence applications, integrating massive datasets in real time and applying AI-driven analytics to identify threats, detect anomalies and enhance situational awareness.

Gotham’s continued adoption by government and defense agencies provides Palantir with long-term revenue stability and exceptionally high switching costs. These relationships also enhance Palantir’s credibility with commercial customers, particularly in regulated industries such as healthcare, finance, and energy. A few companies can successfully serve both public-sector intelligence agencies and large enterprises, giving Palantir a unique competitive advantage.

Together, Foundry and Gotham form a dual-platform strategy that balances high-growth commercial opportunities with durable public-sector contracts.

Palantir’s recent financial performance underscores the scalability of its software model. In the fourth quarter of 2025, total revenues increased 70% year over year, driven primarily by U.S. commercial demand. The company achieved an adjusted operating margin of 57%, its highest level to date, reflecting strong operating leverage and disciplined cost management.

Profitability is also improving on a GAAP basis. Operating income reached $575.4 million, while net income rose to $608.7 million. Earnings per share increased more than 100% year over year, demonstrating that Palantir’s growth is translating into bottom-line results rather than being consumed by rising expenses.

The balance sheet further strengthens the investment case. Palantir ended the quarter with approximately $7.2 billion in cash and equivalents and no debt, providing substantial flexibility to invest in innovation, pursue strategic initiatives and withstand macroeconomic uncertainty.

Palantir currently generates a return on equity of roughly 30%, slightly below the industry average of 32% but still indicative of strong capital efficiency. Importantly, this metric reflects management’s deliberate decision to prioritize platform expansion and long-term scale over short-term optimization.

As investments in product development and customer deployment mature, operating leverage is expected to increase further, providing a pathway for return on equity expansion. For long-term investors, today’s ROE represents a foundation rather than a ceiling.

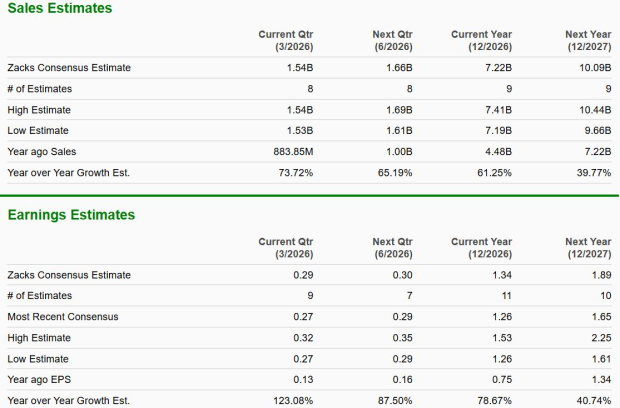

Earnings expectations for Palantir remain highly favorable. The consensus estimate indicates strong year-over-year earnings growth for both the current quarter and the next two fiscal years, supported by accelerating commercial adoption and expanding margins.

The Zacks Consensus Estimate for Palantir’s first-quarter 2026 earnings stands at 29 cents per share, suggesting 123% year-over-year growth. For 2026 and 2027, earnings are projected to increase 79% and 41%, respectively, year over year. Sales are also expected to see robust growth, increasing 74% in the first quarter of 2026, with full-year sales projected to rise 61% in 2026 and 40% in 2027.

Snowflake SNOW operates a cloud-native data platform that enables organizations to store, process, and analyze large datasets across multiple environments. Snowflake emphasizes scalability and cross-cloud compatibility, positioning itself as a neutral data layer. Unlike Palantir’s application-heavy approach, Snowflake focuses more on infrastructure and analytics flexibility, making it a foundational data partner for enterprises pursuing AI initiatives.

C3.ai AI develops enterprise AI applications tailored to sectors such as energy, manufacturing and defense. C3.ai's strategy is centered on pre-built AI models designed to accelerate deployment timelines. While smaller in scale, C3.ai competes in overlapping verticals where applied AI and predictive analytics are core priorities.

Palantir stands out as a rare combination of rapid growth, improving profitability, and strategic relevance in the enterprise AI landscape. With Foundry driving explosive commercial expansion, Gotham anchoring long-term stability, and a debt-free balance sheet supporting continued investment, the company is well positioned for sustained value creation. While near-term volatility is possible following a strong rally, Palantir’s fundamentals continue to strengthen. For investors seeking exposure to scalable, mission-critical AI infrastructure, Palantir remains a buy with a compelling long-term outlook.

PLTR stock currently has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 (Strong Buy) Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 7 hours |

Palantir Aims For 12th Straight Revenue Acceleration, But U.S. Growth Is Key

PLTR

Investor's Business Daily

|

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite