|

|

|

|

|||||

|

|

|

Shareholders of Gibraltar would probably like to forget the past six months even happened. The stock dropped 32% and now trades at $41.26. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Gibraltar, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons you should be careful with ROCK and a stock we'd rather own.

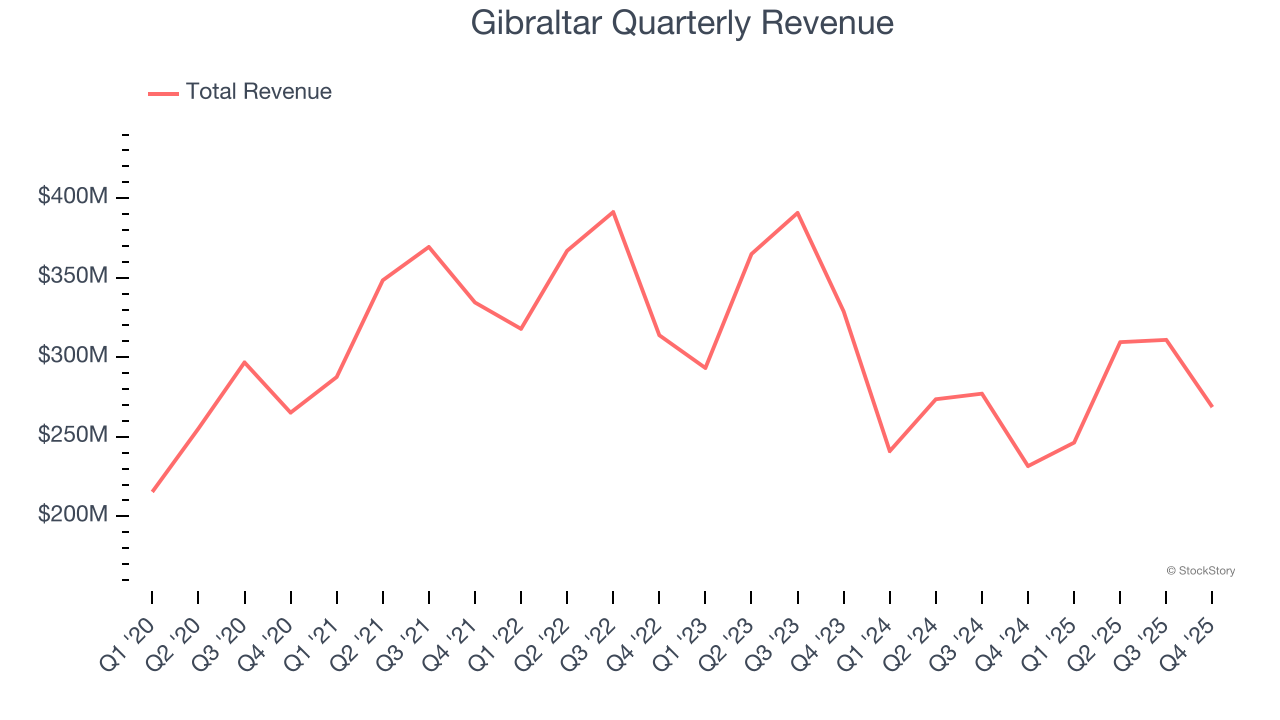

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Gibraltar’s sales grew at a sluggish 1.9% compounded annual growth rate over the last five years. This fell short of our benchmarks.

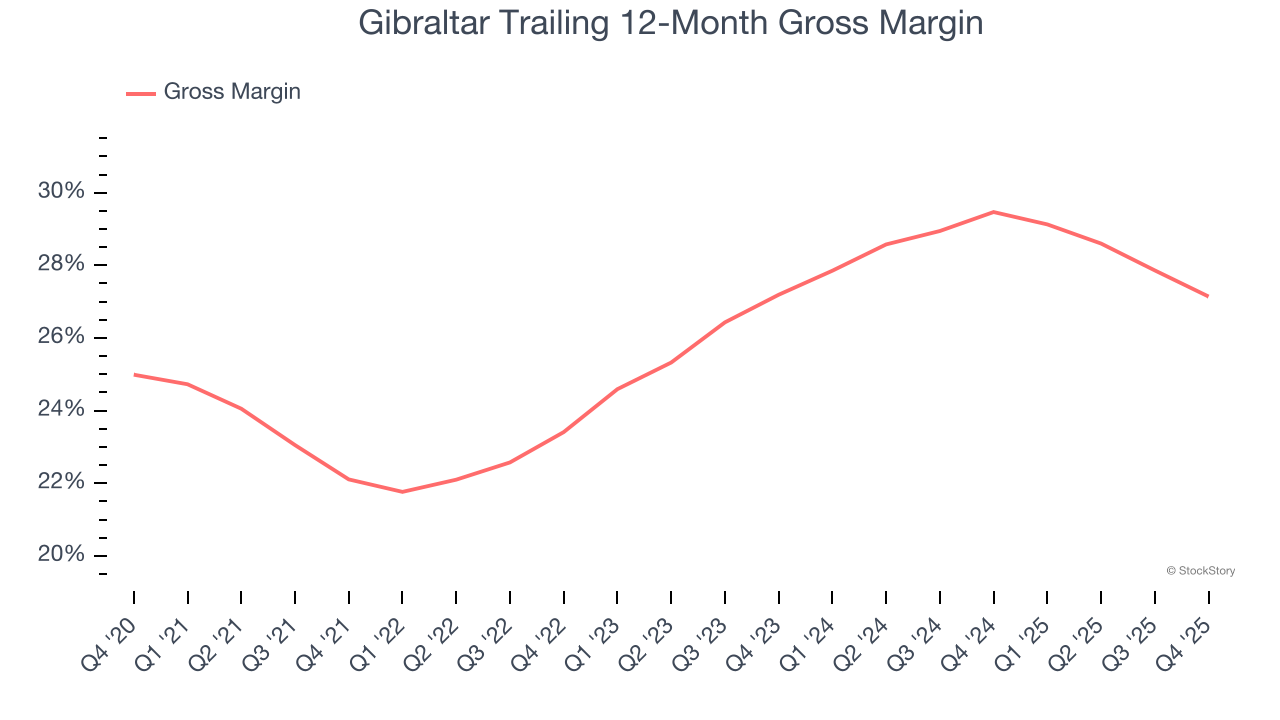

Cost of sales for an industrials business is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics.

Gibraltar has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 25.6% gross margin over the last five years. That means Gibraltar paid its suppliers a lot of money ($74.37 for every $100 in revenue) to run its business.

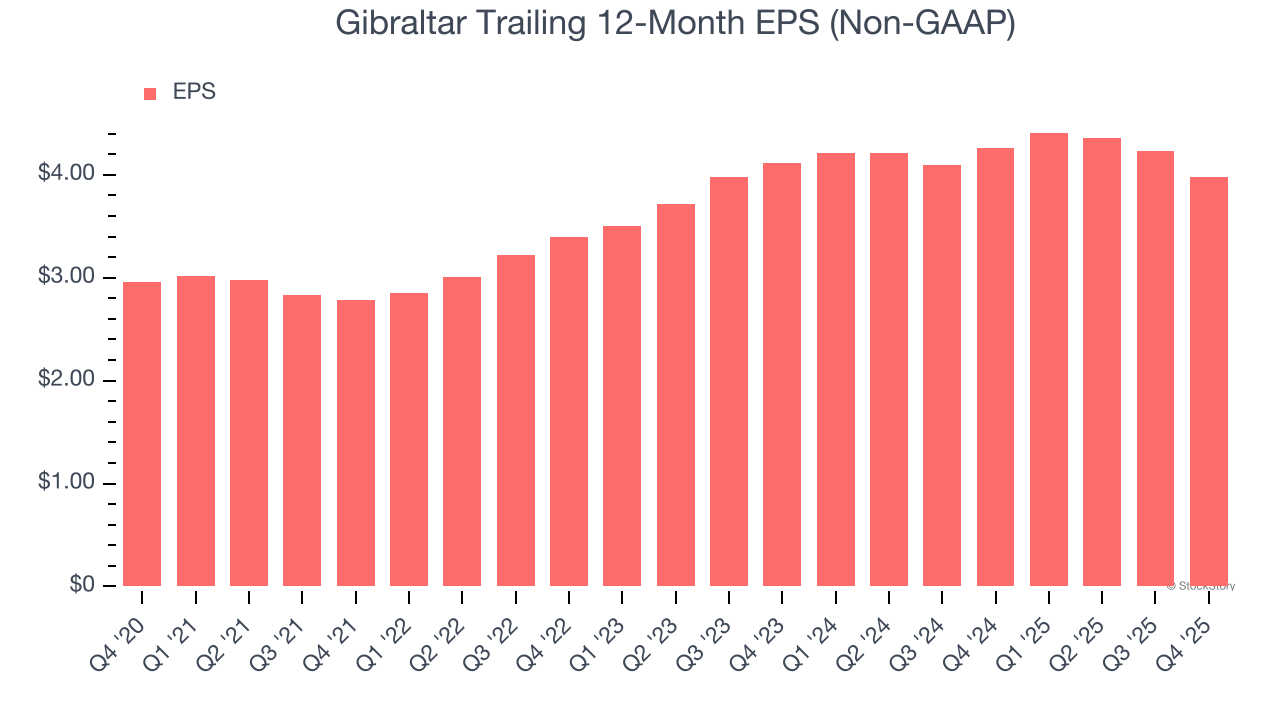

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Gibraltar’s EPS grew at 6.1% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 1.9% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

We see the value of companies helping their customers, but in the case of Gibraltar, we’re out. After the recent drawdown, the stock trades at 11.4× forward P/E (or $41.26 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are better stocks to buy right now. We’d suggest looking at one of our all-time favorite software stocks.

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-22 | |

| Jul-16 | |

| Jul-01 | |

| Jun-03 | |

| May-08 | |

| May-08 | |

| May-07 | |

| May-07 | |

| Apr-23 | |

| Mar-11 | |

| Mar-09 | |

| Mar-09 | |

| Mar-05 | |

| Feb-27 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite