|

|

|

|

|||||

|

|

|

Broadcom AVGO shares appreciated 4.8% post the first-quarter fiscal 2026 results reported on Wednesday. The company registered non-GAAP earnings of $2.05 per share, beating the Zacks Consensus Estimate by 0.99% and jumping 28.1% year over year.

Revenues rallied 29.5% year over year to $19.31 billion and beat the Zacks Consensus Estimate by 0.13%. The strong results were driven by strong Semiconductor solutions revenues, which soared 52% year over year, driven by a 106% surge in AI revenues. AI networking revenues grew 60% year over year and represented one-third of AI revenues.

Broadcom expects a positive second-quarter fiscal 2026 performance, with AI revenues of $10.7 billion, suggesting a 140% year-over-year upsurge. AI networking is expected to accelerate in the second quarter of fiscal 2026 and grow to 40% of the total AI revenues. Semiconductor revenues are expected to be $14.8 billion, indicating 76% year-over-year growth. Broadcom expects revenues of $22 billion, indicating 47% year-over-year growth for the second quarter of fiscal 2026. However, the gross margin is expected to be flat sequentially at 77%.

So, what should investors do with the AVGO stock right now? Let us dig deeper to find out.

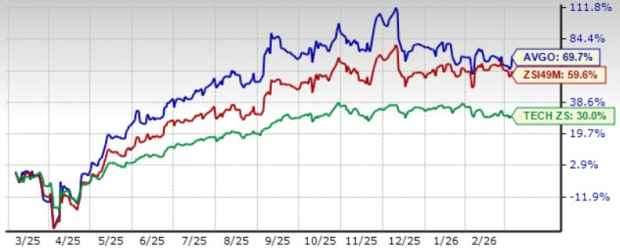

AVGO shares have jumped 69.7% in the trailing 12 months, outperforming the broader Zacks Computer and Technology sector’s and the Zacks Electronics – Semiconductors industry’s returns of 25.2% and 53.2%, respectively. The outperformance can be attributed to an innovative product portfolio, growing clientele and an expanding partner base. AVGO’s prospect benefits from rising AI revenues despite growing concerns over overspending on AI-related infrastructure and services by hyperscalers.

In the first quarter of fiscal 2026, Broadcom’s revenues from custom accelerators jumped 140% year over year. The momentum is expected to continue in the current quarter, thanks to a clientele that includes Google, Meta Platforms and Anthropic. The company continues to gain market share in AI networking, driven by the first-to-market Tomahawk 6 switch at 100 terabit per second, as well as Broadcom’s 200G SerDes, which are capturing demand from hyperscalers.

For 2027, Broadcom expects AI revenues from chips to surpass $100 billion.

However, the sluggish non-AI revenue view for the second quarter of fiscal 2026 is creating a headwind for investors. AVGO’s soft gross margin guidance for the fiscal second quarter indicates a higher AI mix in revenues.

The company continues to face stiff competition from NVIDIA NVDA, Advanced Micro Devices AMD and Skyworks SWKS in the AI domain. NVIDIA is benefiting from strong demand for Hopper and Blackwell architectures, while AMD’s prospects are benefiting from strong demand for EPYC and Instinct processors. Skyworks is benefiting from growing demand for its solutions across edge IoT, automotive and infrastructure end markets, as well as the pending acquisition of Qorvo.

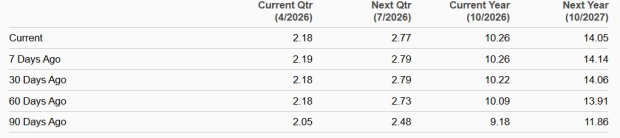

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $10.25 per share, up three cents over the past 30 days, indicating 50.3% growth from the fiscal 2025 reported figure. The consensus mark for fiscal 2026 revenues is pegged at $95.48 billion, suggesting 49.5% growth from the fiscal 2025 reported number.

The Zacks Consensus Estimate for the second-quarter fiscal 2026 earnings is pegged at $2.18 per share, unchanged over the past 30 days, indicating 38% growth from the figure reported in the year-ago quarter. The consensus mark for the second quarter of fiscal 2026 revenues is pegged at $20.44 billion, suggesting 36.2% growth from the figure reported in the year-ago quarter.

Broadcom shares are trading at a premium, as suggested by the Value Score of D. In terms of the forward 12-month price/sales (P/S), AVGO is trading at 14.58X, higher than the broader sector’s 6.2X and industry’s 7.85X. Broadcom is also trading at a premium against peers, NVIDIA, AMD and Skyworks, shares of which are currently trading at 12.87X, 6.77X and 2.23X, respectively.

Although Broadcom’s expanding AI portfolio, along with a rich partner base, reflects solid top-line growth potential, a stretched valuation makes the stock risky for investors.

Broadcom currently carries a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable point to start accumulating the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 30 min | |

| 51 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite