|

|

|

|

|||||

|

|

|

Shares of Barclays PLC BCS on NYSE have declined 14.1% year to date, compared with a 1.8% drop of the industry and a 1.9% fall of the S&P 500 Index. Among its peers, Deutsche Bank DB shares have declined 19%, while HSBC Holdings plc HSBC has gained 6.8% over the same time frame.

Investor apathy toward BCS shares can largely be attributed to the recent geopolitical headwinds, which have resulted in a major sell-off across the broader markets. Does this pullback present a potential buying opportunity? Let’s assess the company’s fundamentals to understand whether this is the right time to buy the stock or wait for a better entry point.

Business Streamlining and Restructuring Efforts: Barclays has been strengthening its market position through targeted acquisitions, partnerships and portfolio optimization, reflecting its focus on core businesses. In October 2025, it announced a deal to acquire the U.S.-based digital lending platform Best Egg. Also, last year, the company became the exclusive issuer of General Motors cards by acquiring a U.S. credit card portfolio with $1.6 billion of receivables and partnered with New York-based Brookfield Asset Management Ltd. to transform its payment acceptance business. In 2025, it divested its stake in Entercard Group and its Germany-based consumer finance business.

In 2024, Barclays acquired Tesco’s retail banking business and streamlined operations by divesting its Italian mortgage portfolio. Further, in 2023, it expanded its U.K. mortgage franchise through the acquisition of Kensington Mortgage. These initiatives are expected to enhance operational efficiency and support profitability over time.

Operational Efficiency Supported by Cost Initiatives: Barclays’ operating performance has begun to improve, supported by its strategic focus on core businesses and cost-efficiency initiatives. The company’s total income recorded a three-year compound annual growth rate (CAGR) of 5.3% (2022-2025).

As part of its structural cost actions to enhance operating efficiency, Barclays achieved £1.7 billion in total gross savings across 2024 and 2025 and is targeting total gross efficiency savings of £2 billion and a cost-to-income ratio in the low 50s by 2028. Despite the volatility in the capital markets business, restructuring initiatives are expected to support top-line growth going forward. The company expects total income to reflect a CAGR of more than 5% between 2025 and 2028.

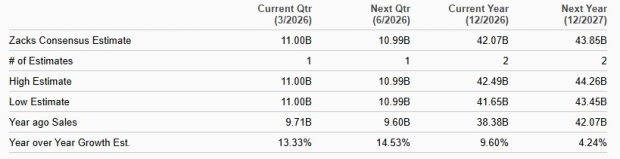

Barclays’ sales estimates for 2026 and 2027 indicate year-over-year growth of 9.6% and 4.2%, respectively.

Strong Capital Distribution and Shareholder Returns: Barclays has a solid capital distribution strategy and consistently rewards its shareholders through regular dividend payments. It intends to maintain dividend payouts at the 2025 level and aims for progressive dividend growth.

Further, Barclays plans to return more than £15 billion to shareholders between 2026 and 2028 through dividends and share buybacks. The company also intends to repurchase up to £1 billion of shares in the first quarter of 2026. Backed by a strong balance sheet, these capital distribution initiatives are expected to enhance long-term shareholder value.

Rising Expense Base: Rising operating expenses remain a concern for Barclays. Its operating costs recorded a three-year CAGR of 2% (ended 2025). Continued investments to strengthen its franchise and upgrade technology are expected to keep expenses elevated.

Weak Asset Quality: Barclays’ credit impairment charges surged to £4.8 billion in 2020, though the company reported a credit impairment release of £653 million in 2021. However, since 2022, the metric has been on the rise, recording a CAGR of 23.2% over the past five years (2020–2025). Given the challenging operating environment, credit impairment charges are expected to remain elevated in the near term.

Analysts seem optimistic regarding Barclays’ earnings growth potential. Over the past 30 days, the Zacks Consensus Estimate for the company’s 2026 and 2027 earnings has been revised higher to $2.91 and $3.39, respectively.

The projected figures imply growth of 30.5% and 16.4% for 2026 and 2027, respectively.

In terms of valuation, BCS’ price-to-earnings (P/E) forward 12 months ratio of 7.28X is lower than the industry’s 10.34X, indicating that the stock is inexpensive.

Barclays is also trading at a discount compared with HSBC and Deutsche Bank. At present, HSBC has a forward 12-month P/E ratio of 10.64X, and Deutsche Bank has a forward 12-month P/E ratio of 7.37X.

Higher operating expenses, a tough operating backdrop and lingering weak asset quality are major headwinds for Barclays. But the company’s strategic focus on core businesses, restructuring initiatives and cost-efficiency measures will likely keep driving growth. Additionally, improving operating performance, a strong balance sheet and consistent capital distribution through dividends and share buybacks are likely to enhance shareholder value.

Hence, this seems to be the right time to buy Barclays stock and hold on to it for solid long-term returns.

Currently, Barclays carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite