|

|

|

|

|||||

|

|

|

Since March 2021, the S&P 500 has delivered a total return of 76%. But one standout stock has more than doubled the market - over the past five years, W.W. Grainger has surged 186% to $1,112 per share. Its momentum hasn’t stopped as it’s also gained 11.8% in the last six months, beating the S&P by 7%.

Is now the time to buy W.W. Grainger, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

We’re happy investors have made money, but we're sitting this one out for now. Here are three reasons we avoid GWW and a stock we'd rather own.

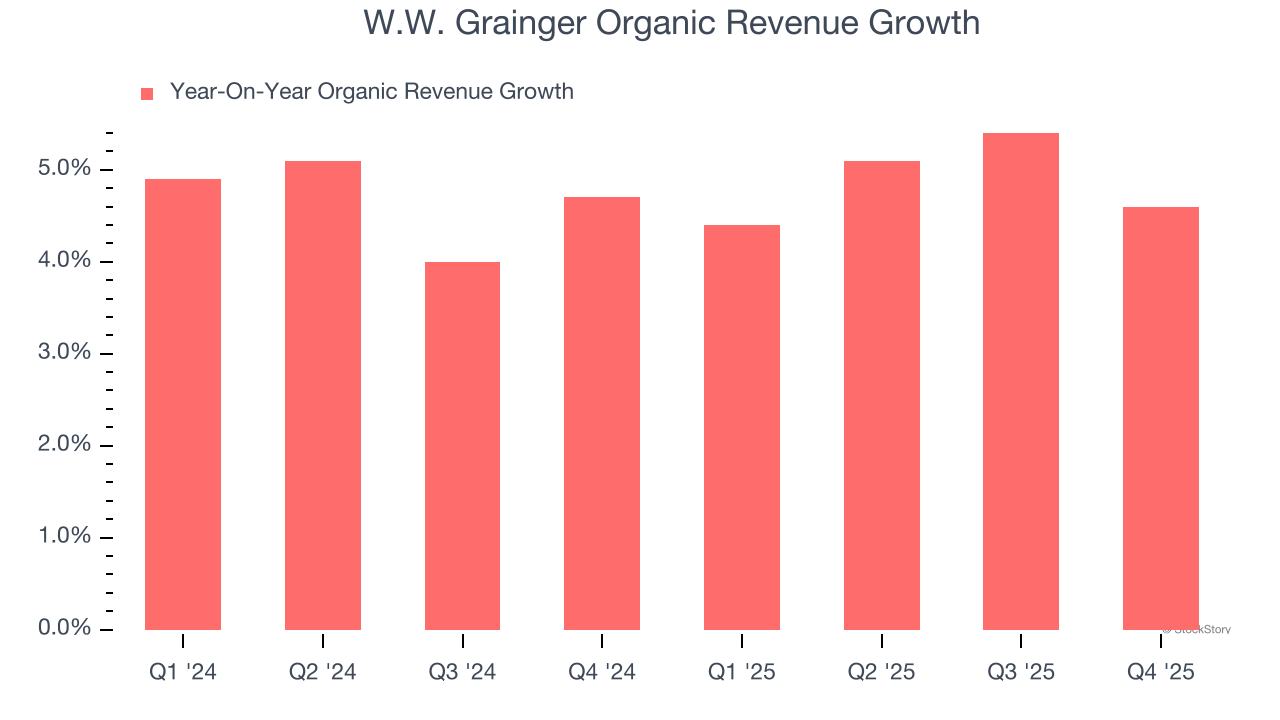

In addition to reported revenue, organic revenue is a useful data point for analyzing Maintenance and Repair Distributors companies. This metric gives visibility into W.W. Grainger’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, W.W. Grainger’s organic revenue averaged 4.8% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect W.W. Grainger’s revenue to rise by 5.6%, close to its 8.7% annualized growth for the past five years. This projection doesn't excite us and suggests its newer products and services will not catalyze better top-line performance yet.

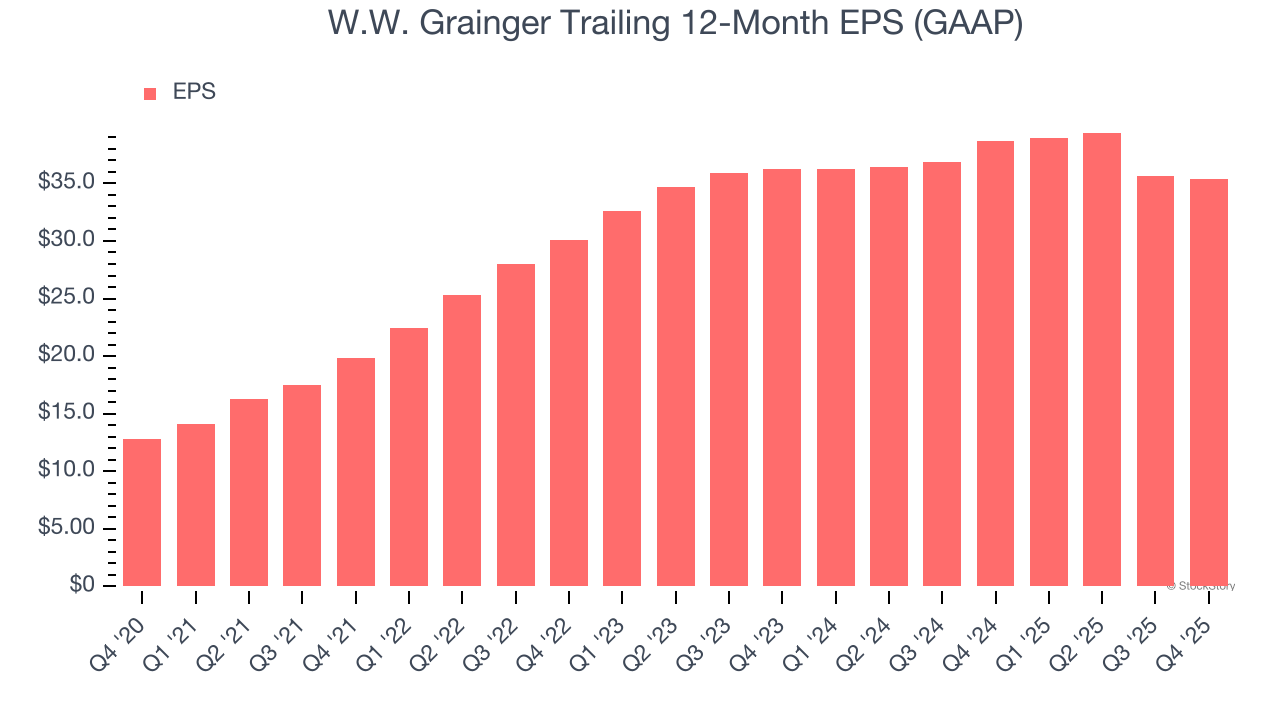

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for W.W. Grainger, its EPS declined by 1.1% annually over the last two years while its revenue grew by 4.3%. This tells us the company became less profitable on a per-share basis as it expanded.

W.W. Grainger isn’t a terrible business, but it isn’t one of our picks. With its shares beating the market recently, the stock trades at 26.3× forward P/E (or $1,112 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at one of our all-time favorite software stocks.

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| 7 hours | |

| 7 hours | |

| Aug-03 | |

| Jul-29 | |

| Jul-21 | |

| Jul-17 | |

| Jul-15 | |

| Jul-10 | |

| Jun-24 | |

| May-11 | |

| May-07 | |

| May-07 | |

| May-07 | |

| Apr-29 | |

| Apr-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite