|

|

|

|

|||||

|

|

|

Vertiv has been on fire lately. In the past six months alone, the company’s stock price has rocketed 102%, reaching $254.23 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is it too late to buy VRT? Find out in our full research report, it’s free.

Formerly part of Emerson Electric, Vertiv (NYSE:VRT) manufactures and services infrastructure technology products for data centers and communication networks.

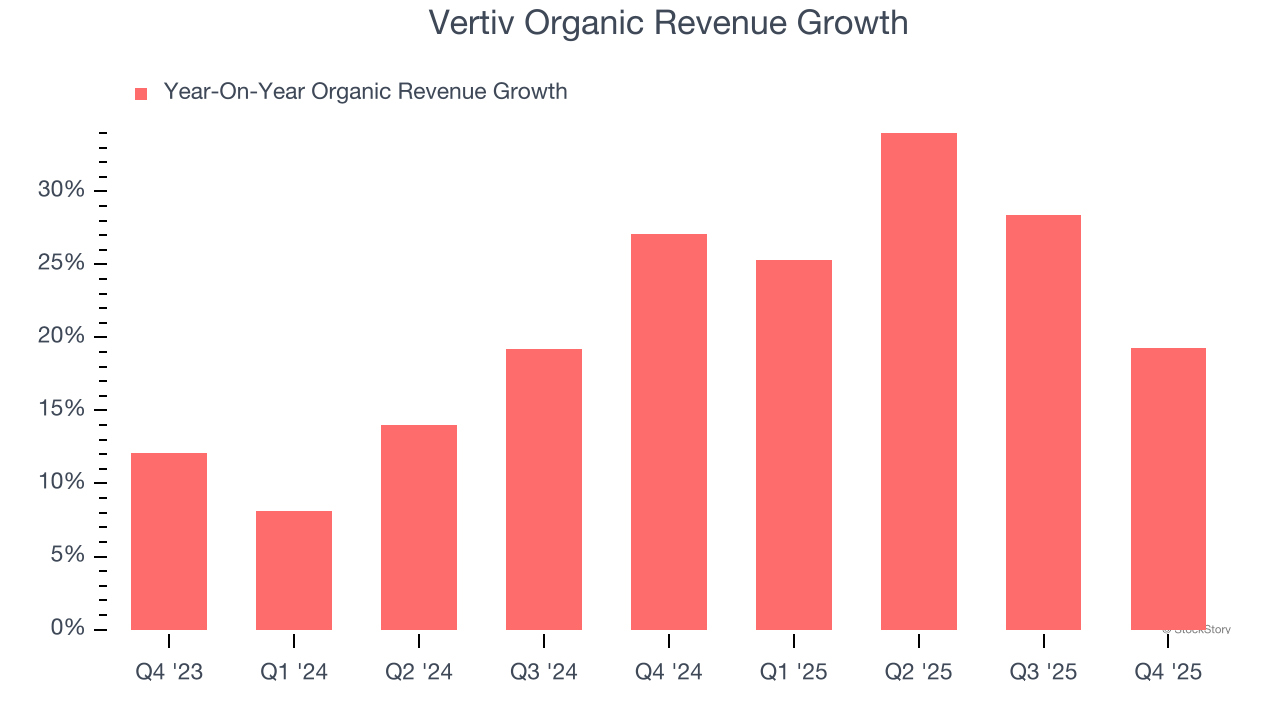

Investors interested in Electrical Systems companies should track organic revenue in addition to reported revenue. This metric gives visibility into Vertiv’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Vertiv’s organic revenue averaged 21.9% year-on-year growth. This performance was fantastic and shows it can expand quickly without relying on expensive (and risky) acquisitions.

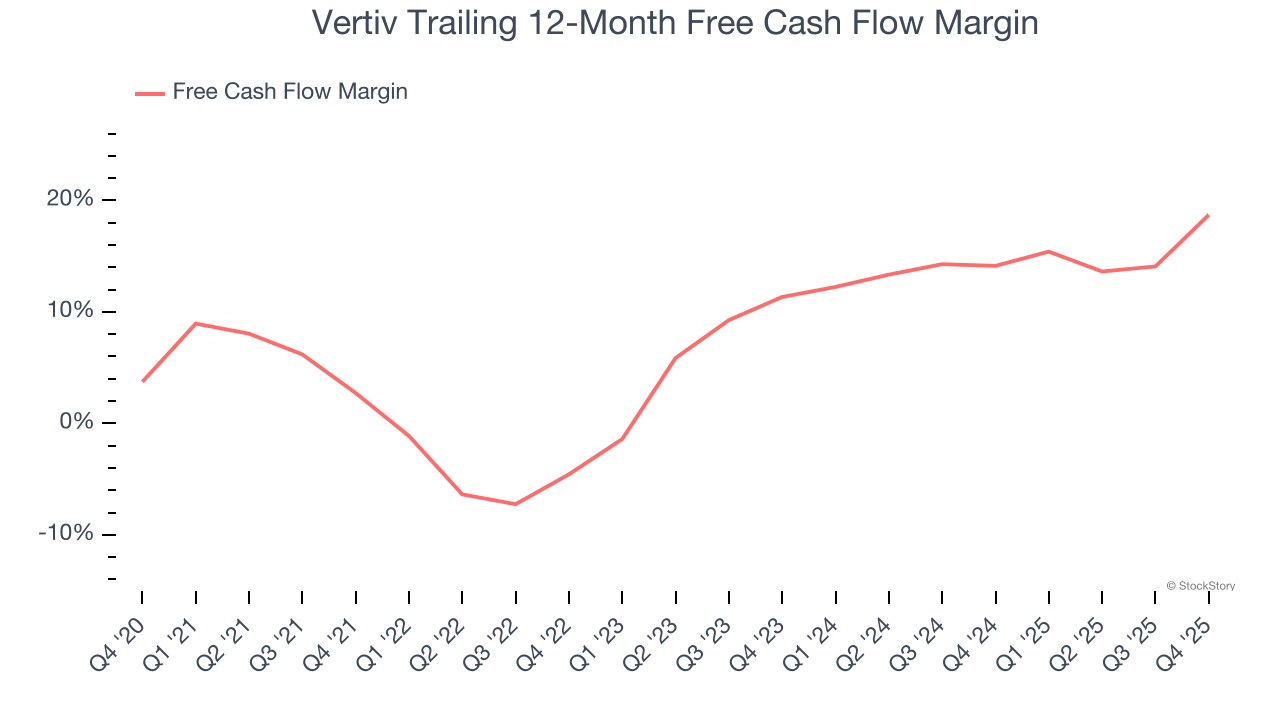

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Vertiv’s margin expanded by 16 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Vertiv’s free cash flow margin for the trailing 12 months was 18.7%.

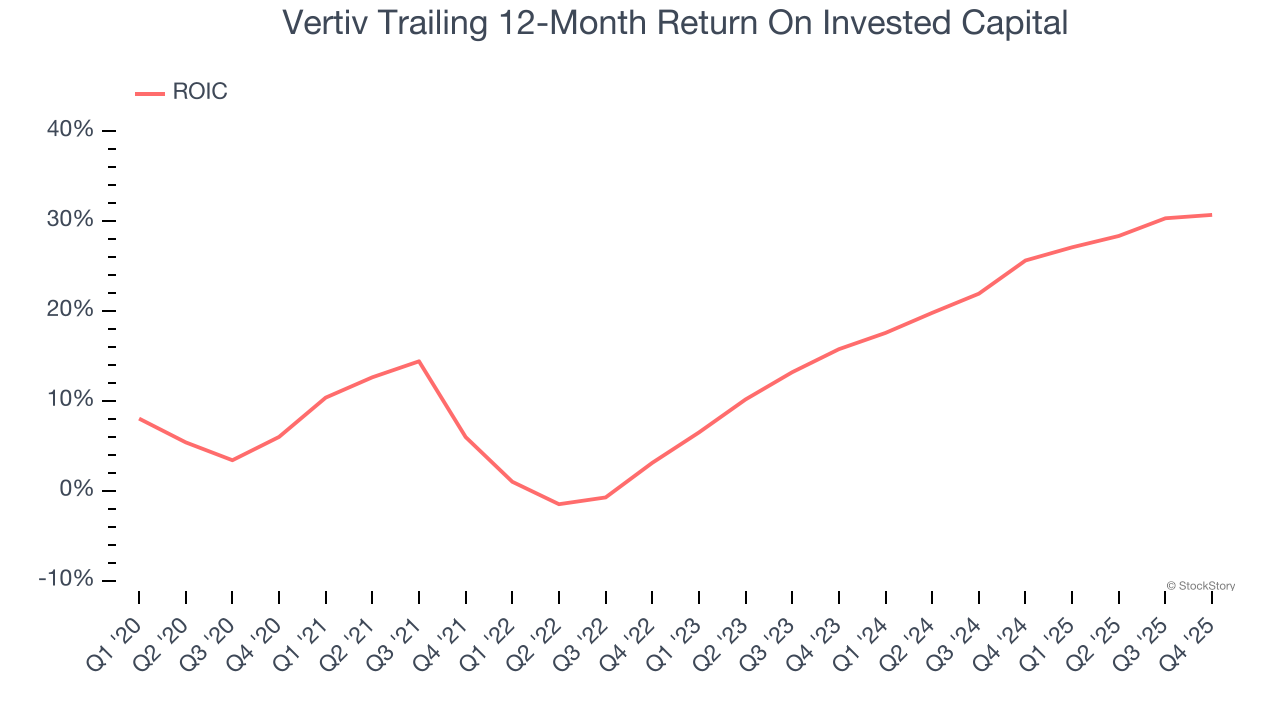

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Vertiv’s ROIC has increased significantly over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

These are just a few reasons why we're bullish on Vertiv, and after the recent surge, the stock trades at 40.7× forward P/E (or $254.23 per share). Is now a good time to buy despite the apparent froth? See for yourself in our in-depth research report, it’s free.

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| 13 hours | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-15 | |

| Jul-15 | |

| Jul-13 | |

| Jul-10 | |

| Jul-09 | |

| Jul-09 | |

| Jul-06 | |

| Jul-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite