|

|

|

|

|||||

|

|

|

Over the last six months, Franklin BSP Realty Trust’s shares have sunk to $9.40, producing a disappointing 19.1% loss - a stark contrast to the S&P 500’s 4.8% gain. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy Franklin BSP Realty Trust, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Even though the stock has become cheaper, we're swiping left on Franklin BSP Realty Trust for now. Here are three reasons we avoid FBRT and a stock we'd rather own.

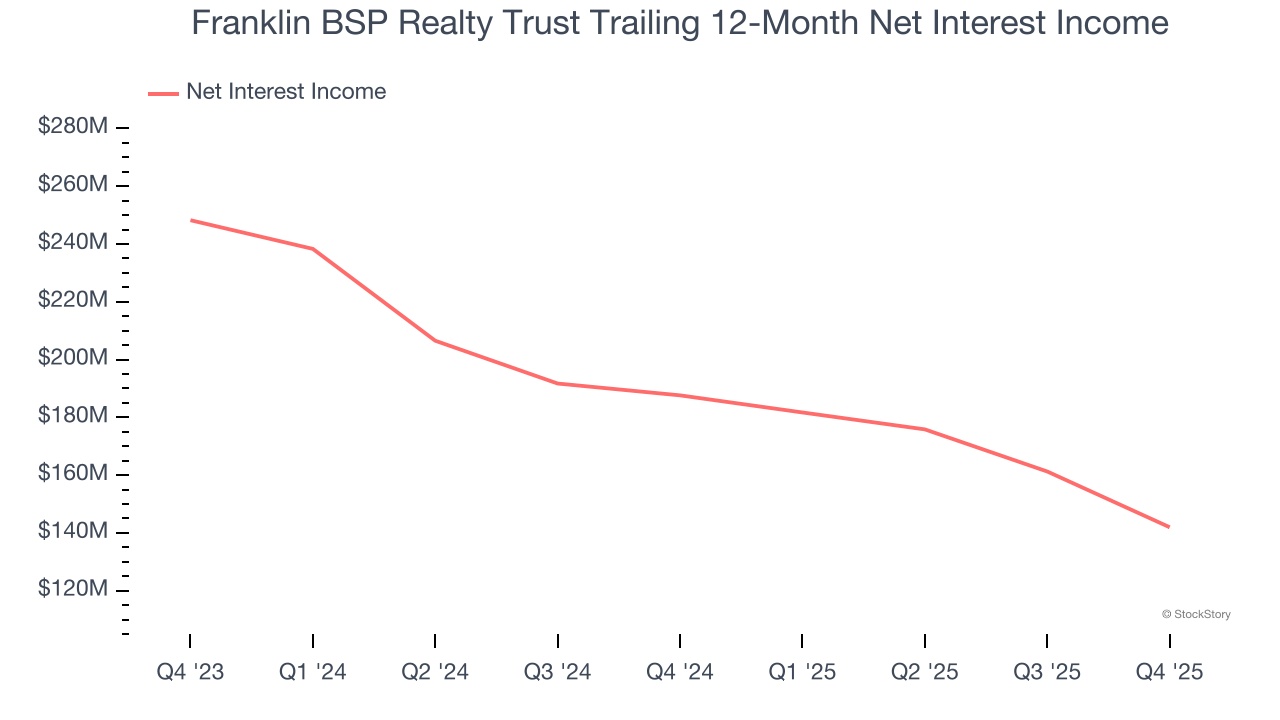

While bank generate revenue from multiple sources, investors view net interest income as a cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of one-time fees.

Franklin BSP Realty Trust’s net interest income has grown at a 6.1% annualized rate over the last five years, worse than the broader banking industry and slower than its total revenue.

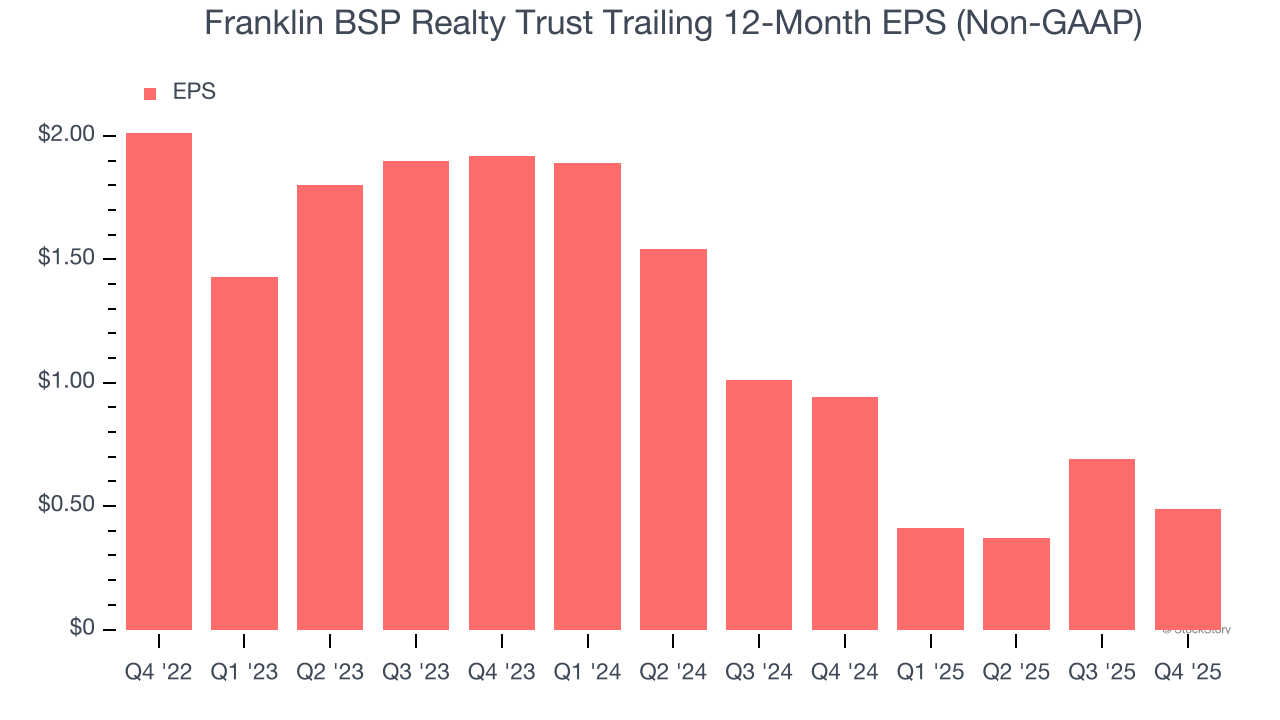

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Franklin BSP Realty Trust’s full-year EPS dropped significantly over the last three years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Franklin BSP Realty Trust’s low margin of safety could leave its stock price susceptible to large downswings.

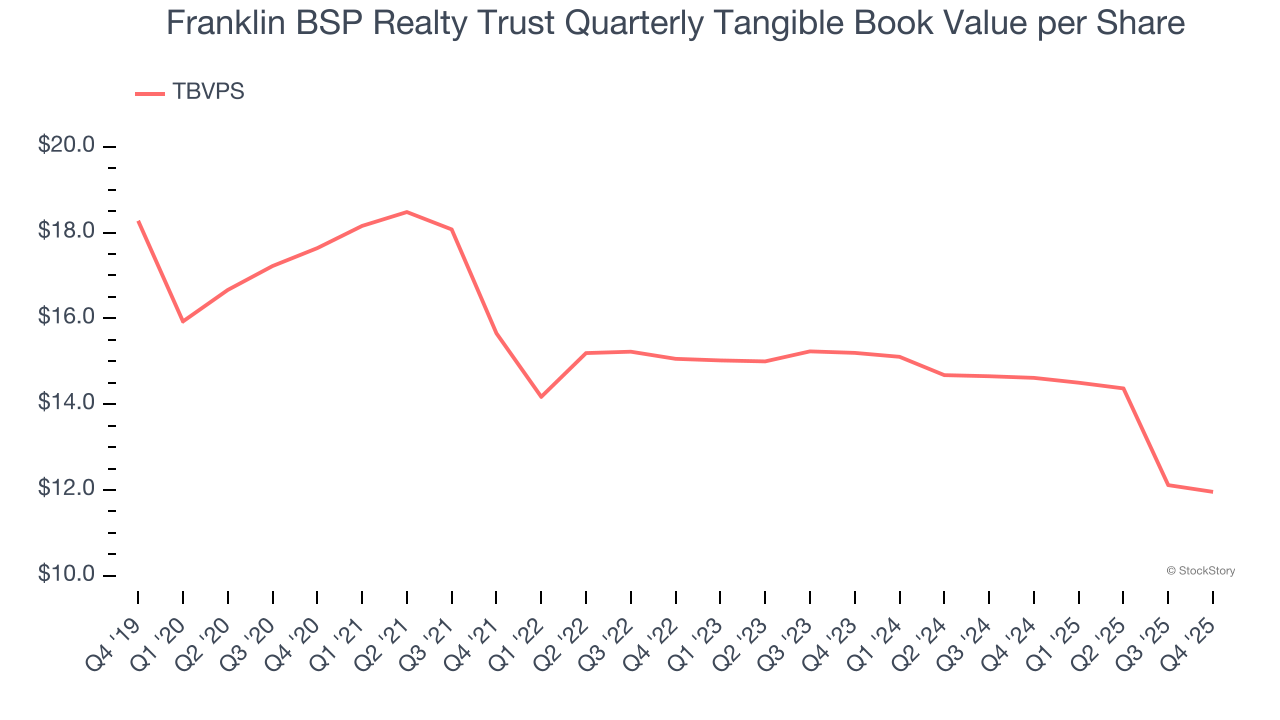

Tangible book value per share (TBVPS) serves as a key indicator of a bank’s financial strength, representing the hard assets available to shareholders after removing intangible assets that could evaporate during financial distress.

To the detriment of investors, Franklin BSP Realty Trust’s TBVPS continued freefalling over the past two years as TBVPS declined at a -11.3% annual clip (from $15.20 to $11.96 per share).

We see the value of companies driving economic growth, but in the case of Franklin BSP Realty Trust, we’re out. Following the recent decline, the stock trades at 0.7× forward P/B (or $9.40 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now. Let us point you toward one of our all-time favorite software stocks.

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jun-17 | |

| Apr-30 | |

| Apr-29 | |

| Apr-29 | |

| Apr-15 | |

| Apr-02 | |

| Apr-02 | |

| Mar-30 | |

| Mar-30 | |

| Mar-12 | |

| Mar-09 | |

| Mar-09 | |

| Mar-03 | |

| Feb-18 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite