|

|

|

|

|||||

|

|

|

Atmus Filtration Technologies has had an impressive run over the past six months as its shares have beaten the S&P 500 by 24.3%. The stock now trades at $58.66, marking a 29.1% gain. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Atmus Filtration Technologies, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons we avoid ATMU and a stock we'd rather own.

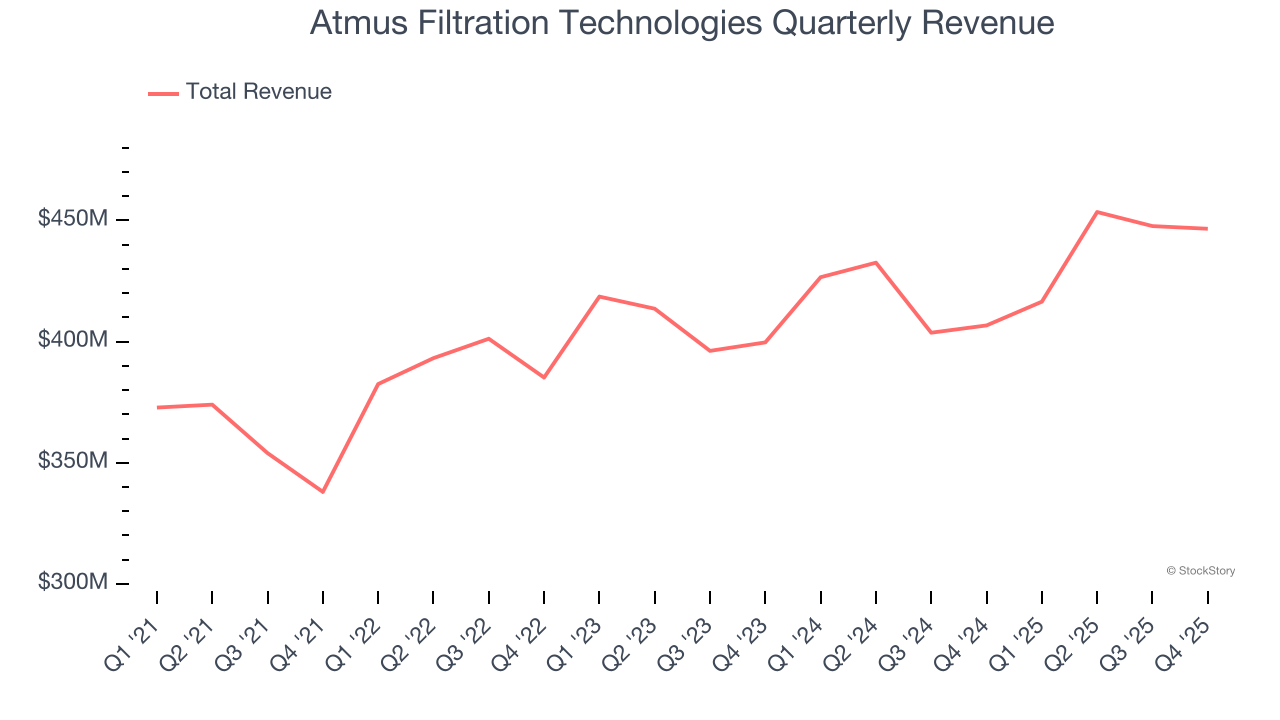

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last four years, Atmus Filtration Technologies grew its sales at a tepid 5.2% compounded annual growth rate. This was below our standard for the industrials sector.

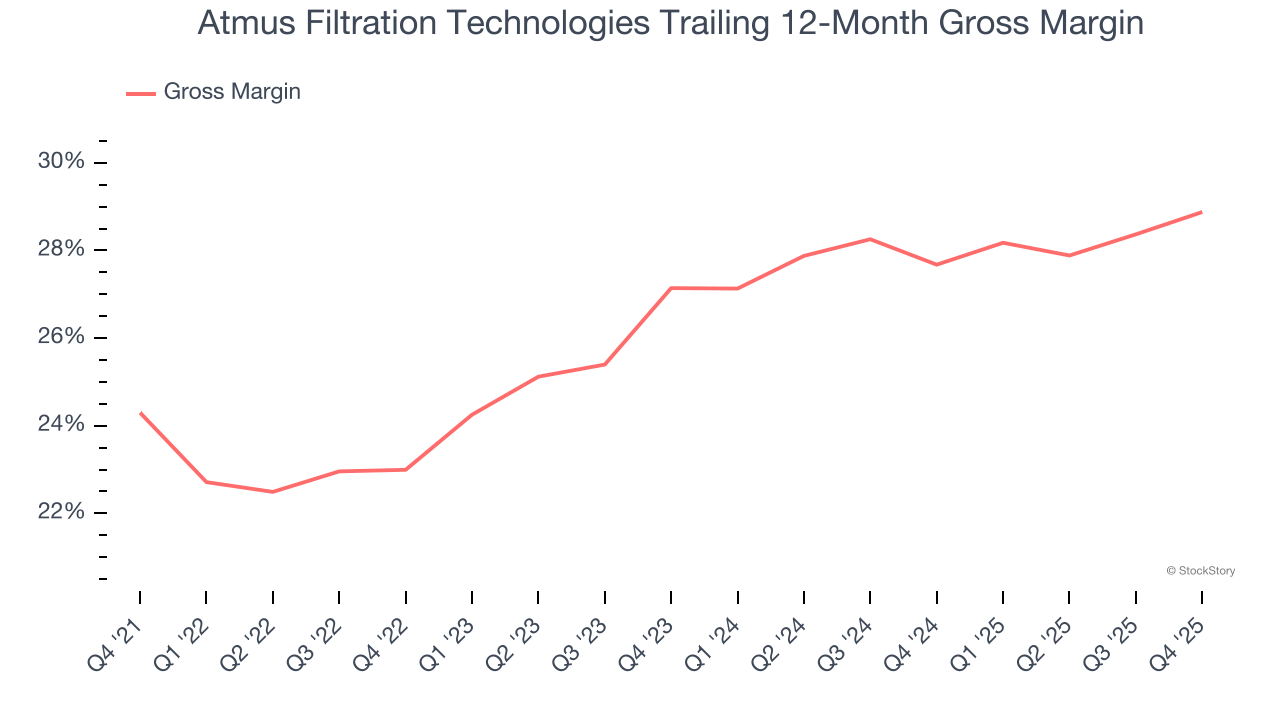

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Atmus Filtration Technologies has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 26.3% gross margin over the last five years. Said differently, Atmus Filtration Technologies had to pay a chunky $73.68 to its suppliers for every $100 in revenue.

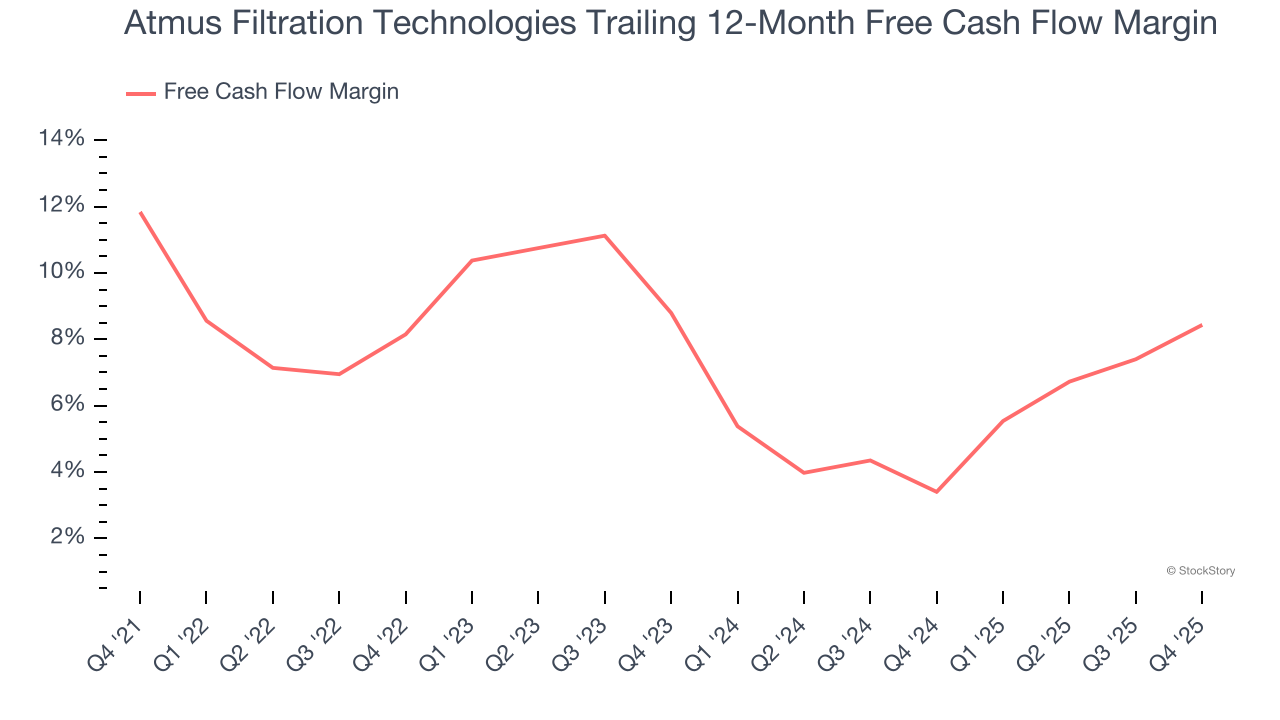

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Atmus Filtration Technologies’s margin dropped by 3.4 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal increasing investment needs and capital intensity. Atmus Filtration Technologies’s free cash flow margin for the trailing 12 months was 8.4%.

Atmus Filtration Technologies isn’t a terrible business, but it doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 21× forward P/E (or $58.66 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. Let us point you toward a top digital advertising platform riding the creator economy.

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| May-13 | |

| May-11 | |

| May-02 | |

| May-01 | |

| May-01 | |

| May-01 | |

| Apr-30 | |

| Apr-16 | |

| Apr-14 |

Stock Of The Day: New S&P 600 Firm, Old S&P 500 Parent Near Buy Points

ATMU

Investor's Business Daily

|

| Apr-02 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite