|

|

|

|

|||||

|

|

|

Watsco currently trades at $393.14 per share and has shown little upside over the past six months, posting a small loss of 2.2%. The stock also fell short of the S&P 500’s 4.8% gain during that period.

Is now the time to buy Watsco, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

We don't have much confidence in Watsco. Here are three reasons there are better opportunities than WSO and a stock we'd rather own.

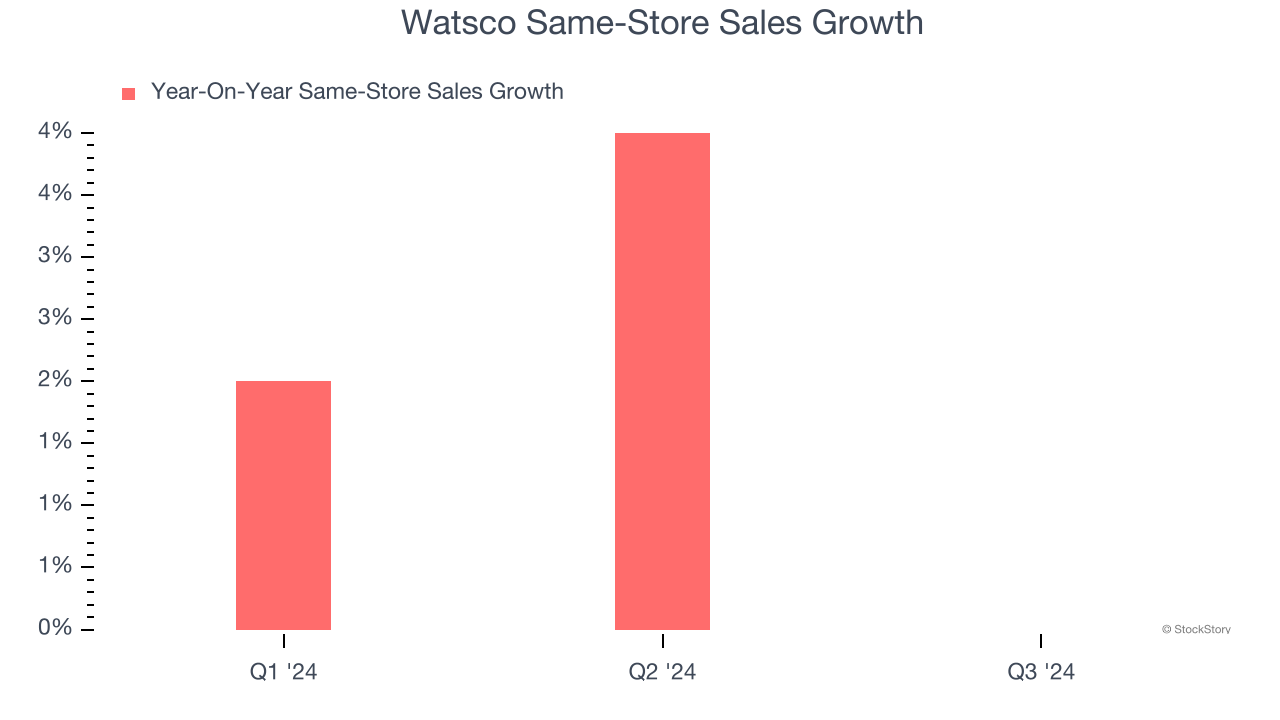

In addition to reported revenue, same-store sales are a useful data point for analyzing Infrastructure Distributors companies. This metric measures the change in sales at brick-and-mortar locations that have existed for at least a year, giving visibility into Watsco’s underlying demand characteristics.

Over the last two years, Watsco’s same-store sales averaged 2% year-on-year growth. This performance was underwhelming and suggests it might have to change its strategy or pricing, which can disrupt operations.

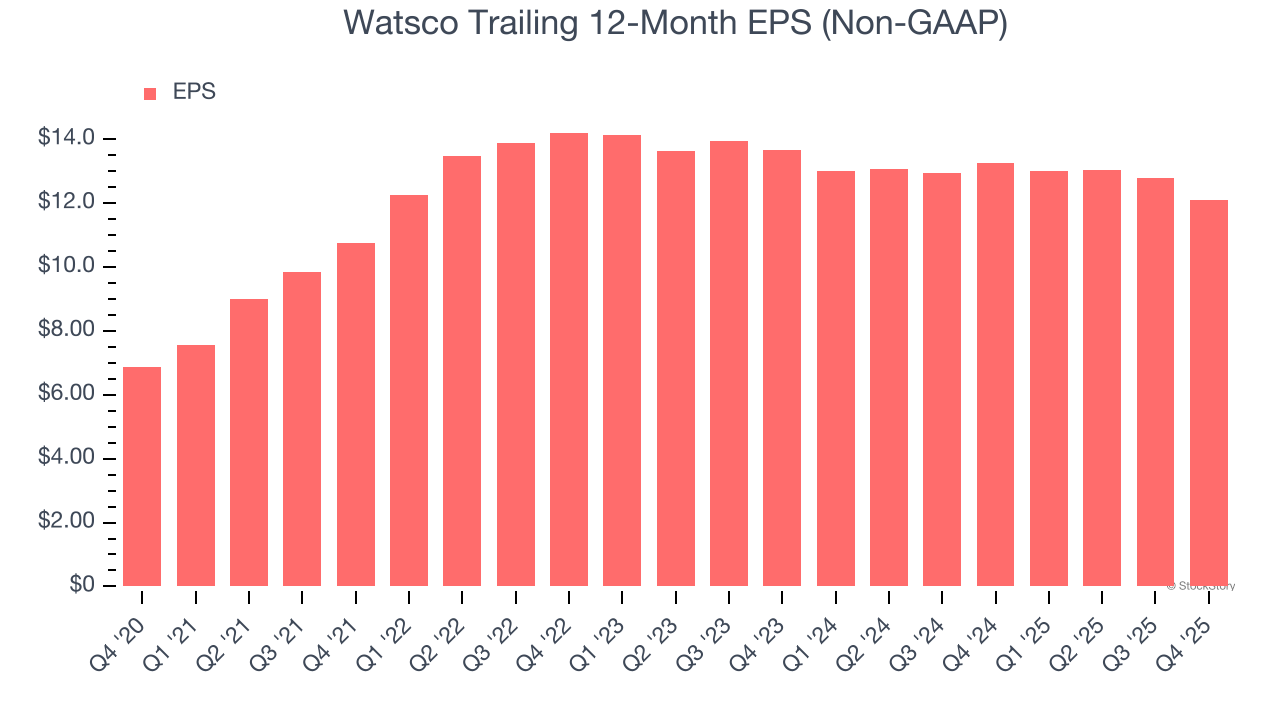

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Watsco, its EPS declined by 5.8% annually over the last two years while its revenue was flat. This tells us the company struggled to adjust to choppy demand.

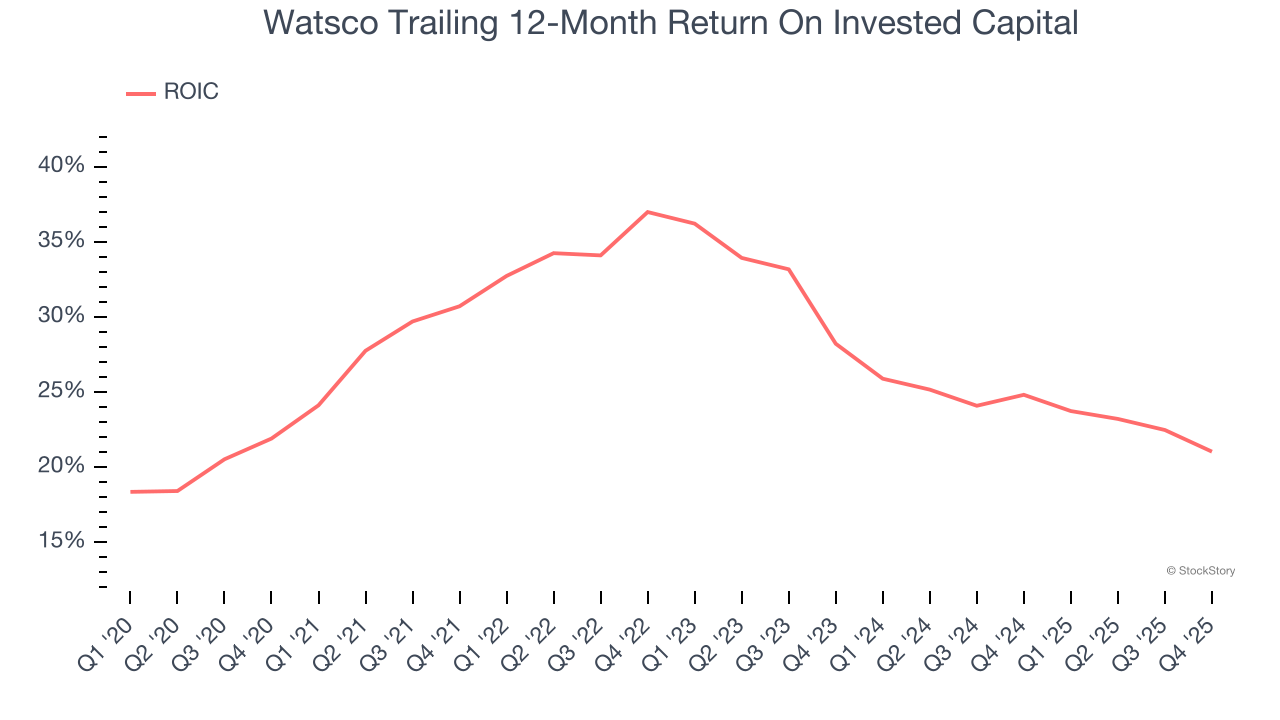

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Watsco’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

We cheer for all companies making their customers lives easier, but in the case of Watsco, we’ll be cheering from the sidelines. With its shares trailing the market in recent months, the stock trades at 32.1× forward P/E (or $393.14 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. We’d suggest looking at an all-weather company that owns household favorite Taco Bell.

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-16 | |

| Jul-01 | |

| Jun-16 | |

| Jun-02 | |

| Apr-29 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-10 | |

| Apr-01 | |

| Mar-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite