|

|

|

|

|||||

|

|

|

Over the past six months, SEI Investments’s stock price fell to $81.42. Shareholders have lost 6% of their capital, which is disappointing considering the S&P 500 has climbed by 4.8%. This may have investors wondering how to approach the situation.

Given the weaker price action, is now an opportune time to buy SEIC? Find out in our full research report, it’s free.

Founded in 1968 as Simulated Environments Inc. to train bank loan officers using computer simulations, SEI Investments (NASDAQ:SEIC) provides technology platforms, investment management, and operational solutions for financial institutions, wealth managers, and investors.

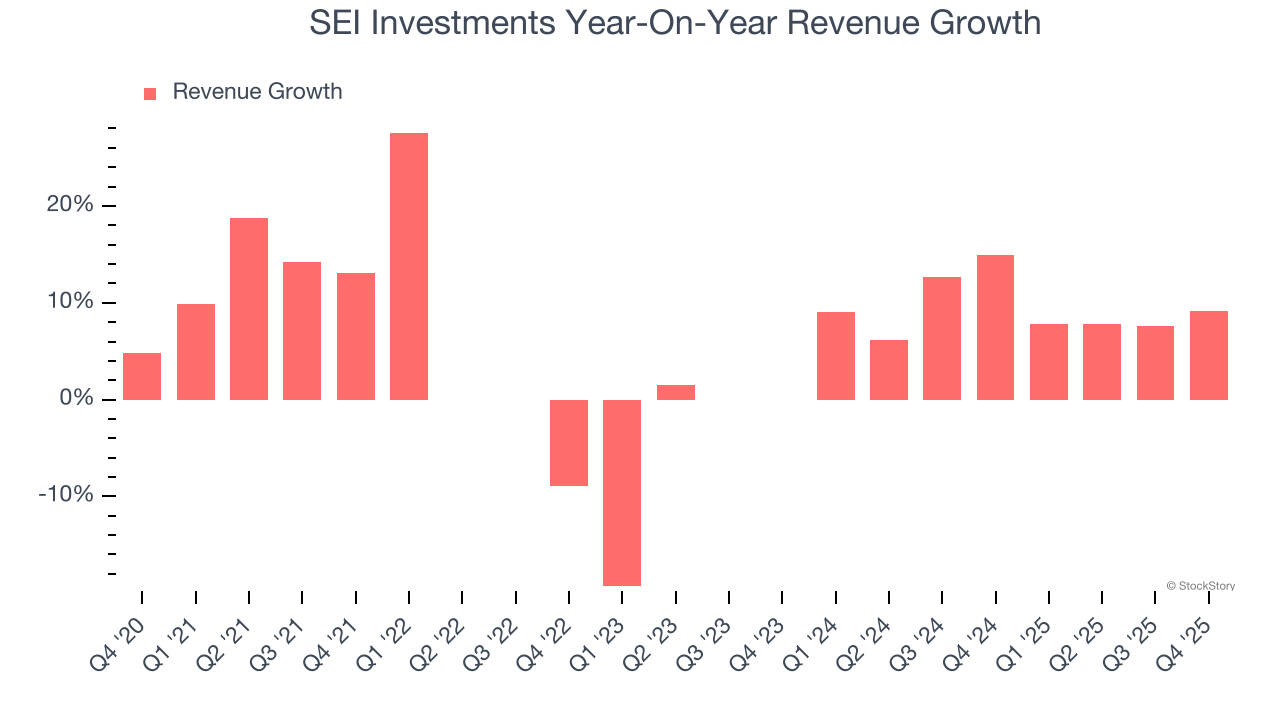

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. SEI Investments’s annualized revenue growth of 9.4% over the last two years is above its five-year trend, suggesting some bright spots.

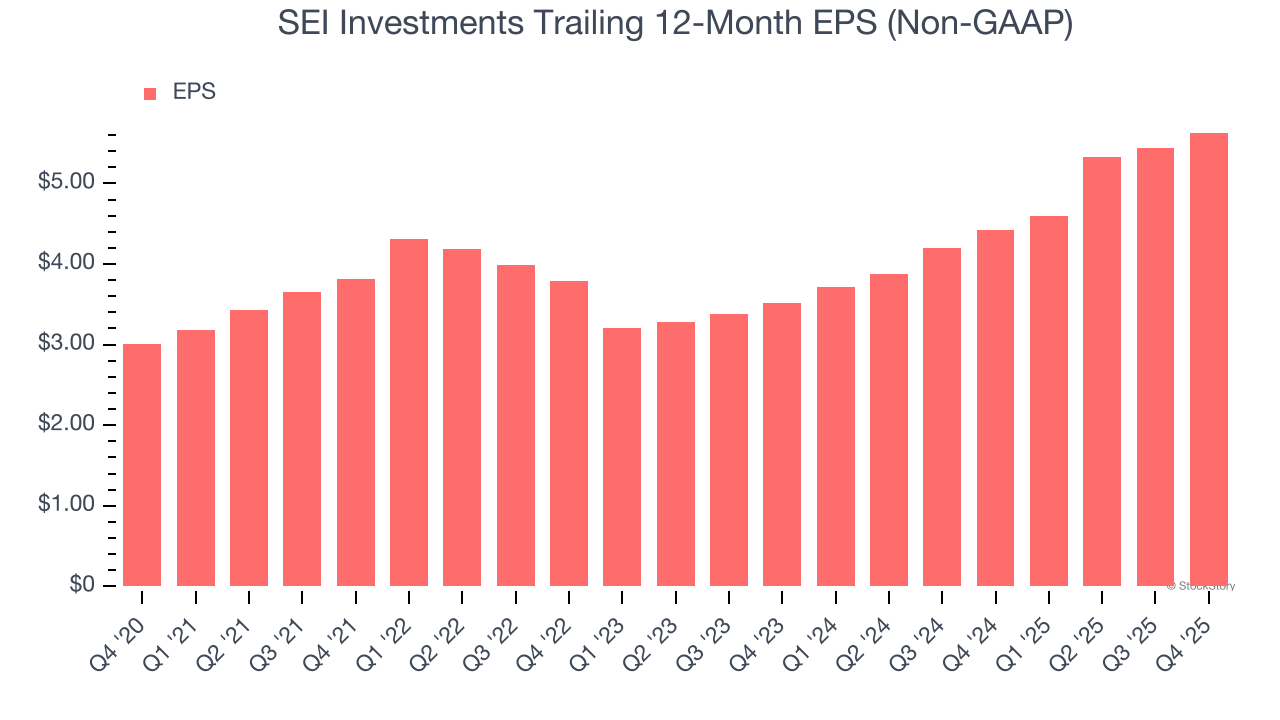

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

SEI Investments’s EPS grew at 13.3% compounded annual growth rate over the last five years, higher than its 6.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

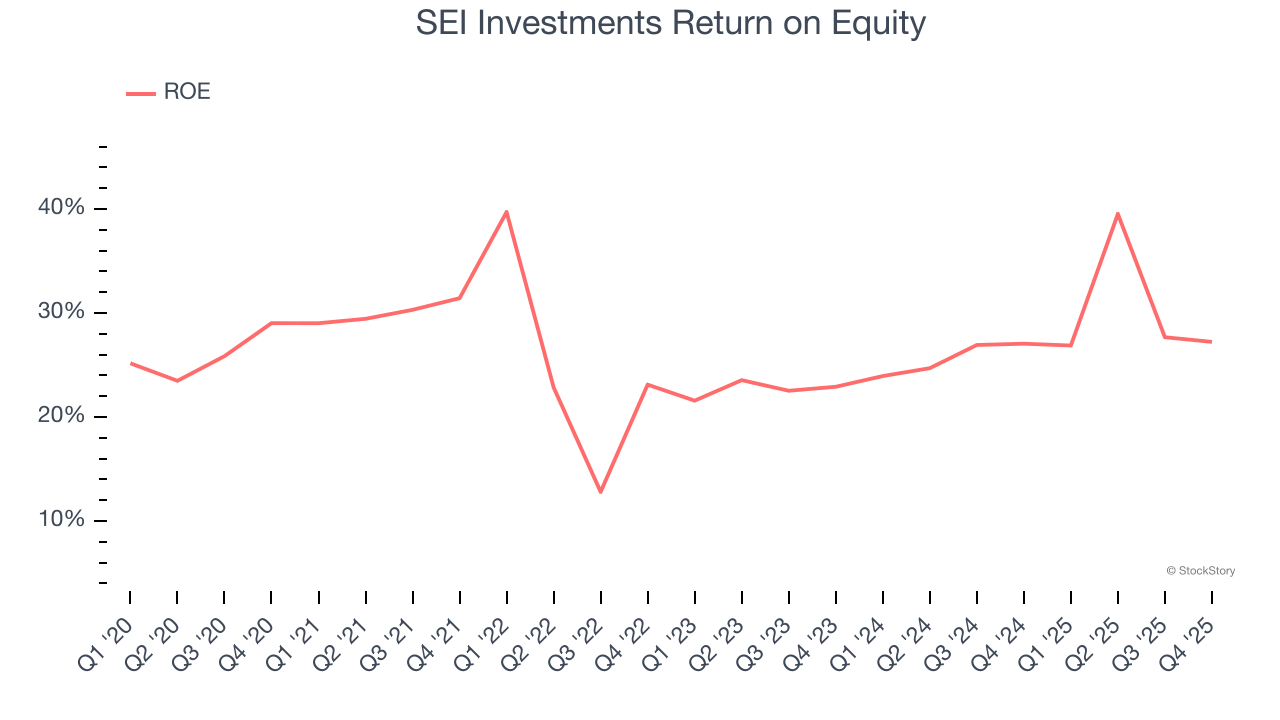

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, SEI Investments has averaged an ROE of 26.7%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows SEI Investments has a strong competitive moat.

These are just a few reasons SEI Investments is a high-quality business worth owning. With the recent decline, the stock trades at 14.5× forward P/E (or $81.42 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-14 | |

| Jul-08 | |

| Jun-30 | |

| Jun-23 | |

| Jun-18 | |

| Jun-16 | |

| Jun-11 | |

| Jun-09 | |

| May-27 | |

| May-27 | |

| May-26 | |

| May-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite