|

|

|

|

|||||

|

|

|

Over the past six months, Fidelity National Financial’s stock price fell to $49.21. Shareholders have lost 17.9% of their capital, which is disappointing considering the S&P 500 has climbed by 4.8%. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Fidelity National Financial, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Despite the more favorable entry price, we're cautious about Fidelity National Financial. Here are three reasons why FNF doesn't excite us and a stock we'd rather own.

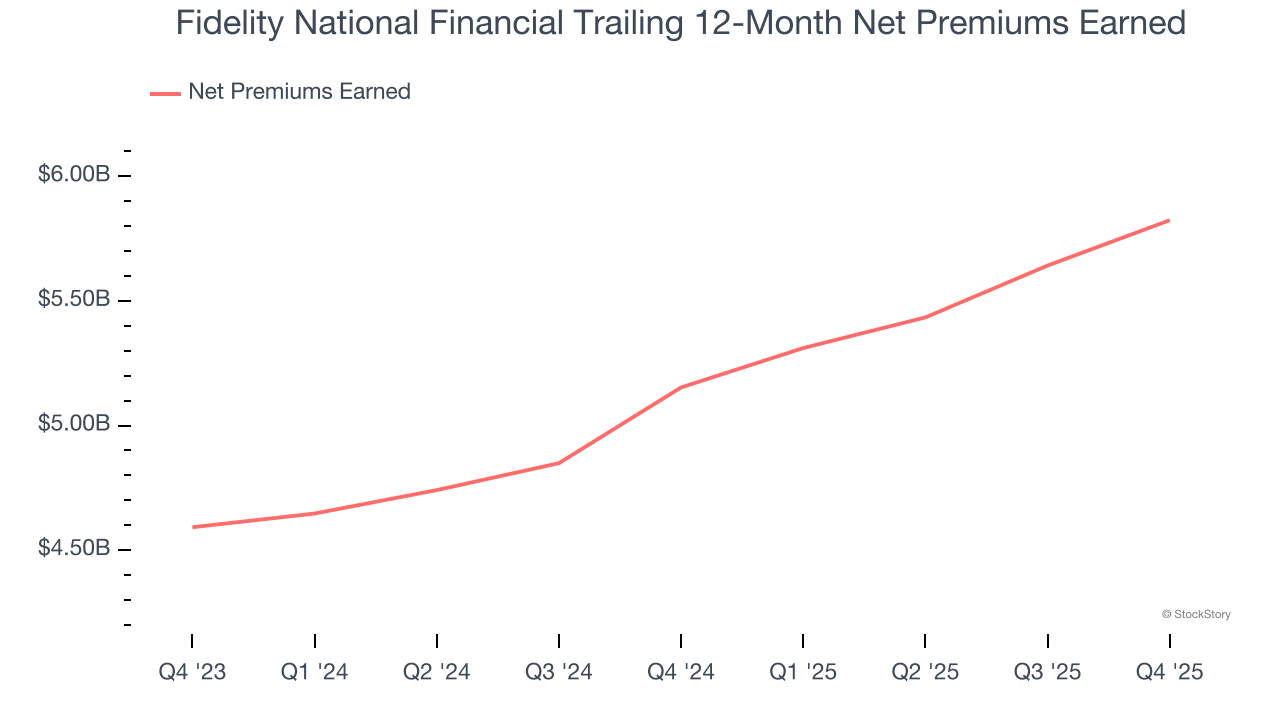

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are therefore gross premiums less what’s ceded to reinsurers as a risk mitigation and transfer strategy.

Fidelity National Financial’s net premiums earned has declined by 1.6% annually over the last five years, much worse than the broader insurance industry. This shows that policy underwriting underperformed its other business lines.

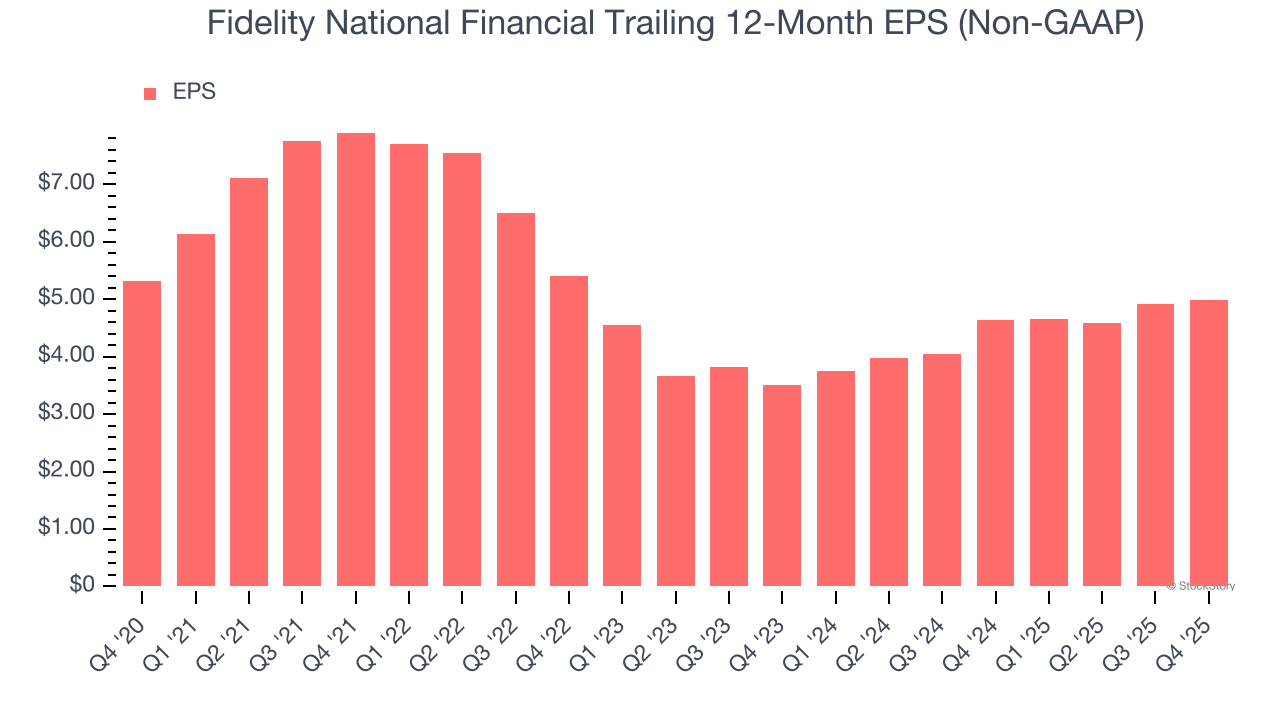

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Fidelity National Financial, its EPS declined by 1.3% annually over the last five years while its revenue grew by 6%. This tells us the company became less profitable on a per-share basis as it expanded.

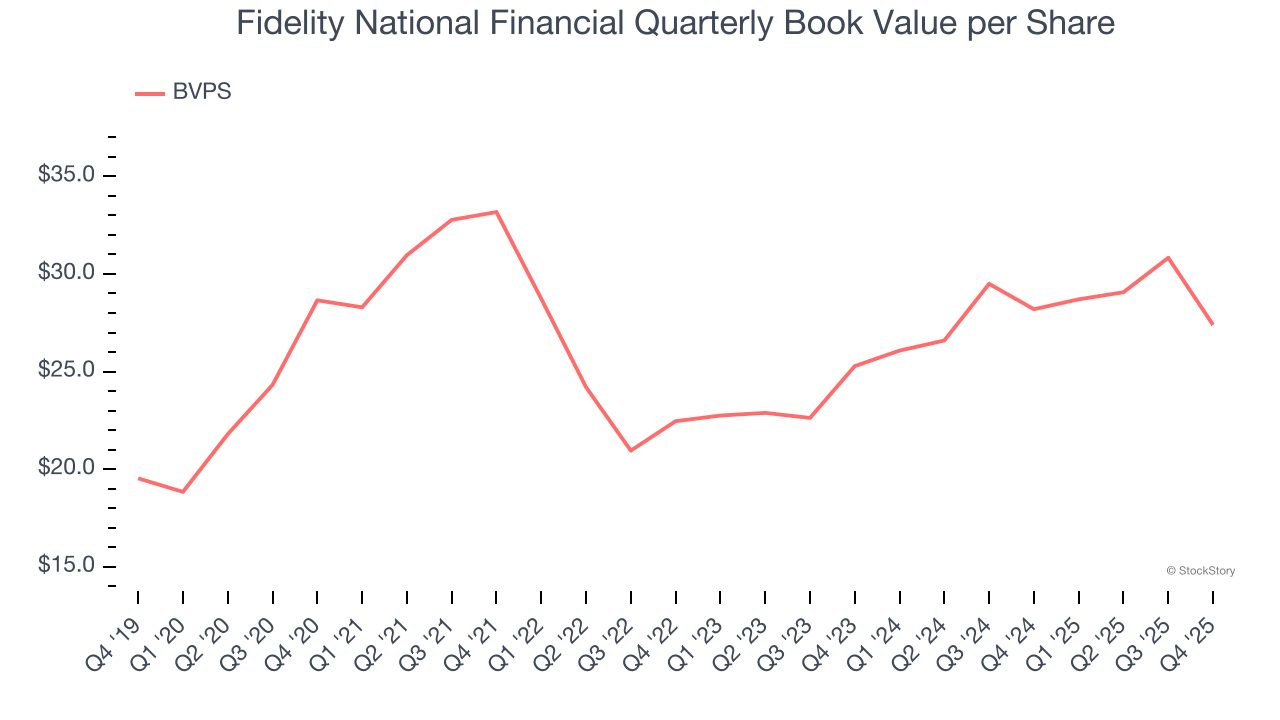

For insurers, book value per share (BVPS) is a vital measure of financial health, representing the total assets available to shareholders after accounting for all liabilities, including policyholder reserves and claims obligations.

Disappointingly for investors, Fidelity National Financial’s BVPS grew at a sluggish 4.1% annual clip over the last two years.

Fidelity National Financial’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 1.4× forward P/B (or $49.21 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. We’d recommend looking at the most dominant software business in the world.

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-24 | |

| Jul-22 | |

| Jun-03 | |

| May-07 | |

| May-07 | |

| May-06 | |

| May-06 | |

| Apr-22 | |

| Mar-25 | |

| Mar-09 | |

| Mar-09 | |

| Mar-03 | |

| Feb-25 | |

| Feb-23 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite