|

|

|

|

|||||

|

|

|

Amazon.com AMZN delivered a strong operational finish to 2025, posting record quarterly revenues and accelerating cloud growth, yet the stock has struggled to build on that momentum. The company’s aggressive investment posture, while strategically compelling over the long term, is compressing near-term cash flows and widening the gap between its premium multiple and current earnings power.

From a valuation standpoint, AMZN stock appears overvalued, trading at a forward 12-month price/earnings ratio of 26.46X, higher than the industry’s 21.77X. Amazon has a Value Score of C.

For investors weighing their options, the evidence tilts toward holding existing positions rather than adding aggressively — or waiting for a more favorable entry point to emerge in 2026.

Amazon’s fourth-quarter 2025 results demonstrated the depth of its growth engine. Net sales rose 14% year over year to a record $213.4 billion, comfortably beating the consensus estimate. Amazon Web Services (“AWS”) was the standout performer, growing 24% year over year to $35.6 billion — its fastest pace in 13 quarters — fueled by enterprises accelerating their shift to cloud and AI workloads. Operating income rose to $25 billion from $21.2 billion in the year-ago period.

However, diluted earnings per share came in at $1.95, a modest miss versus expectations, and free cash flow contracted sharply to $11.2 billion from $38.2 billion, weighed down by a year of record capital investment.

The most consequential detail from Amazon’s fourth-quarter report was its 2026 capital expenditure guidance of approximately $200 billion — a roughly 53% increase from the $131.8 billion deployed in 2025 — with the bulk directed toward AWS AI infrastructure. For first-quarter 2026, the company guided net sales of $173.5 billion to $178.5 billion, representing 11% to 15% year-over-year growth, and operating income of $16.5 billion to $21.5 billion. The wide guidance range reflects incremental headwinds, including roughly $1 billion in added year-over-year costs tied to Amazon Leo, its satellite Internet constellation, as well as investments in quick commerce and sharper pricing in international stores.

Beyond earnings, Amazon has been active on multiple fronts in early 2026. In February, the company successfully launched 32 satellites for Amazon Leo aboard an Arianespace Ariane 64 rocket — the largest Leo payload to date — bringing the total constellation to over 200 satellites in orbit. In March, AWS introduced Amazon Connect Health, a purpose-built agentic AI solution designed to automate administrative tasks for healthcare providers, including patient scheduling, medical coding and clinical documentation. The company also announced a record $340 billion investment in U.S. infrastructure, employees and communities in 2025, spanning AI and cloud infrastructure, rural delivery expansion and employee compensation increases, underscoring the breadth of its long-term ambitions.

The Zacks Consensus Estimate for AMZN’s 2026 earnings is pegged at $7.78 per share, implying an 8.51% increase from the prior year — a solid growth trajectory that reflects confidence in the business.

Amazon.com, Inc. price-consensus-chart | Amazon.com, Inc. Quote

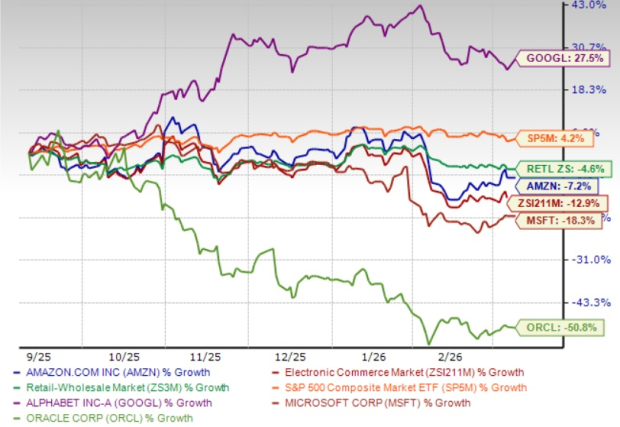

Amazon shares have lost 7.2% over the past six months compared with the Zacks Internet – Commerce industry and the Zacks Retail-Wholesale sector’s decline of 12.9% and 4.6%, respectively.

In the cloud space, Alphabet GOOGL-owned Google Cloud and Microsoft MSFT Azure continue to outpace Amazon in growth rates. According to new data from Synergy Research Group, Amazon, Microsoft and Alphabet held fourth-quarter worldwide cloud market shares of 28%, 21% and 14%, respectively. Microsoft and Alphabet are steadily narrowing the gap, applying sustained competitive pressure on AWS. Oracle ORCL, the world’s fifth-largest cloud infrastructure provider, held a 3% share of the global cloud market in fourth-quarter 2025.

Amazon’s long-term investment thesis remains intact across e-commerce, cloud, advertising and emerging technologies. However, the enormous capital commitment required to sustain that growth compresses free cash flow and introduces execution risk in the near term. Investors who currently own AMZN are likely best served by holding, given the company’s formidable structural advantages across its core businesses and diversified revenue streams. That said, prospective buyers may find the current risk-reward less compelling given near-term earnings and cash flow dynamics. A pullback — perhaps triggered by broader market weakness — could offer a more attractive entry point for new investors in 2026. Amazon currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

AMZN MSFT

Investor's Business Daily

|

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

What to watch next week: Big Tech earnings, the Fed, and Consumer Confidence

GOOGL MSFT

Yahoo Finance Video

|

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite