|

|

|

|

|||||

|

|

|

Since March 2021, the S&P 500 has delivered a total return of 72.6%. But one standout stock has doubled the market - over the past five years, BNY has surged 148% to $113.77 per share. Its momentum hasn’t stopped as it’s also gained 9.4% in the last six months thanks to its solid quarterly results, beating the S&P by 6.3%.

Is there a buying opportunity in BNY, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Despite the momentum, we're swiping left on BNY for now. Here are three reasons why BK doesn't excite us and a stock we'd rather own.

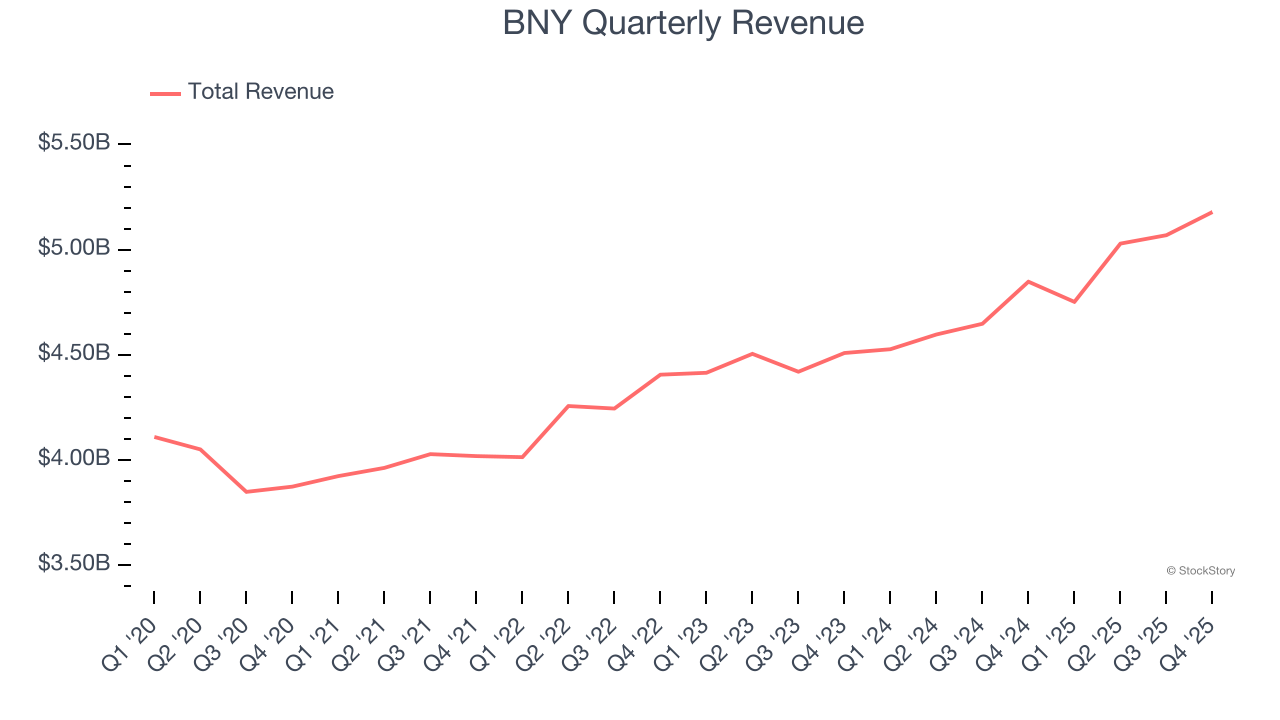

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

Regrettably, BNY’s revenue grew at a tepid 4.7% compounded annual growth rate over the last five years. This was below our standard for the financials sector.

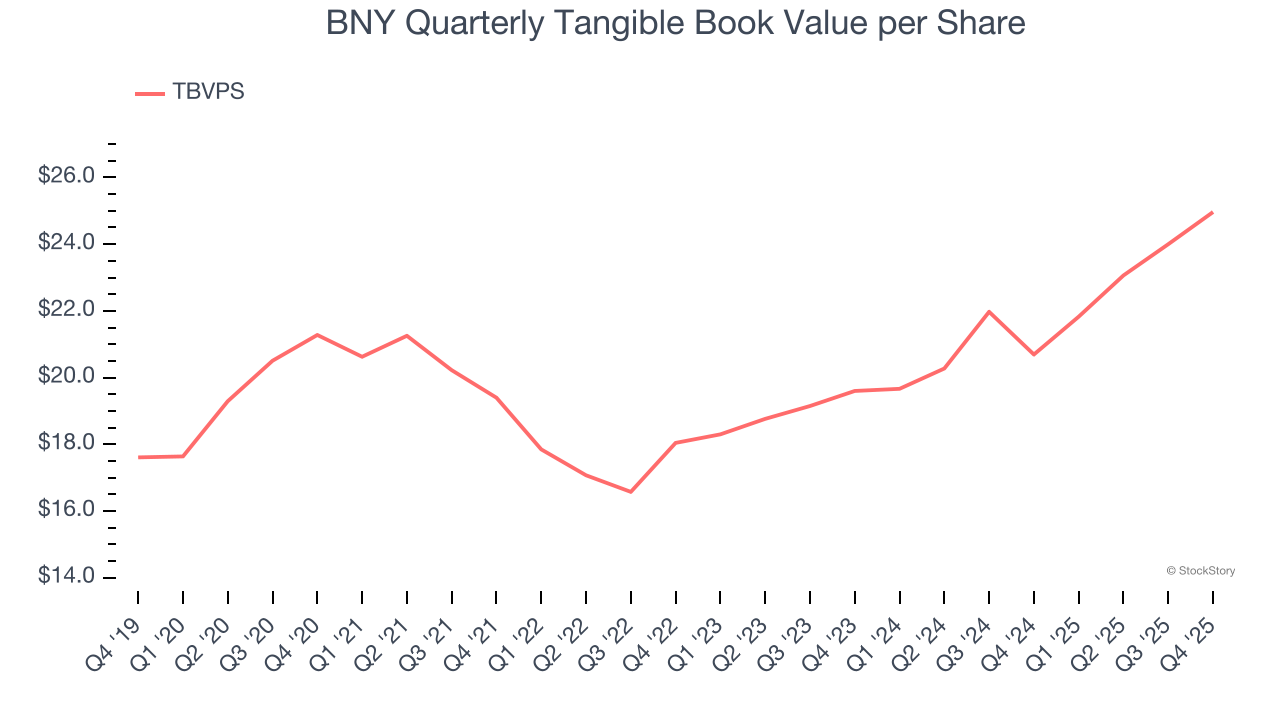

In the financials industry, tangible book value per share (TBVPS) provides the clearest picture of shareholder value, as it focuses on concrete assets while excluding intangible items that may not hold value during challenging times.

Although BNY’s TBVPS increased by a meager 3.2% annually over the last five years, the good news is that its growth has recently accelerated as TBVPS grew at an impressive 12.9% annual clip over the past two years (from $19.60 to $24.96 per share).

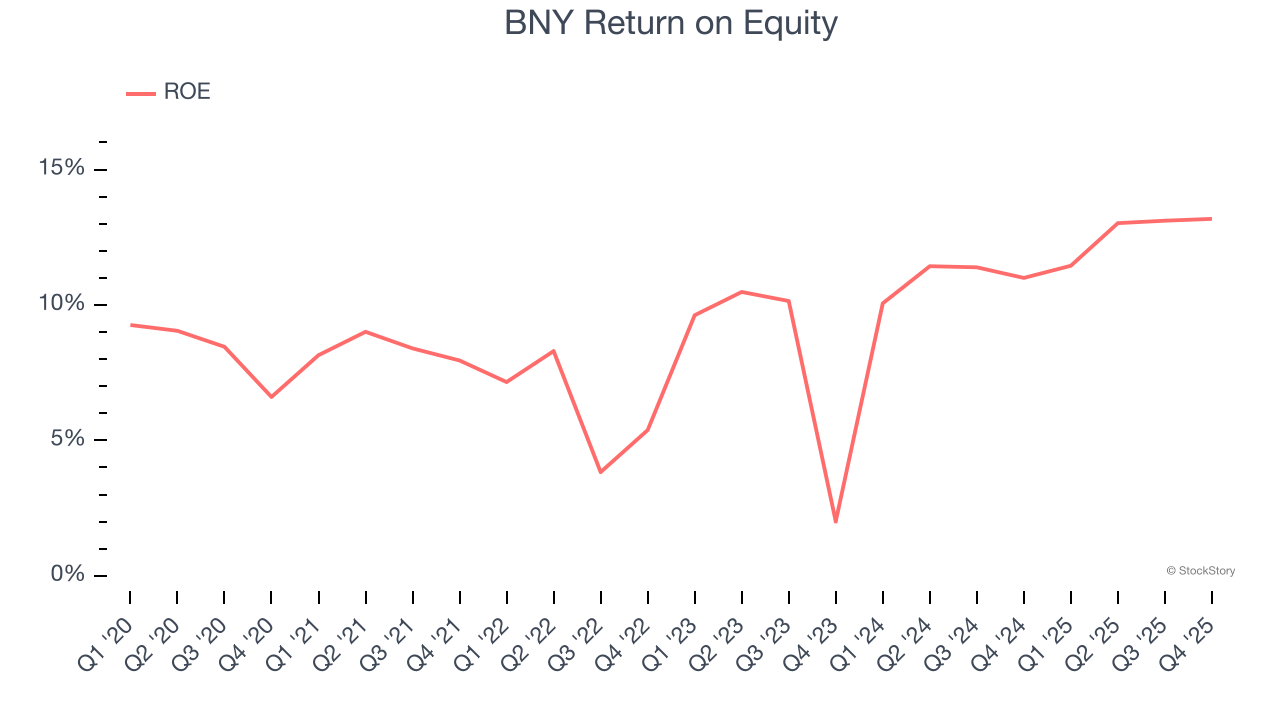

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, BNY has averaged an ROE of 9.3%, uninspiring for a company operating in a sector where the average shakes out around 10%.

BNY isn’t a terrible business, but it isn’t one of our picks. With its shares topping the market in recent months, the stock trades at 13.8× forward P/E (or $113.77 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| May-19 |

BNY Announces ETF Share Splits

Business Wire

|

| May-14 | |

| May-11 | |

| May-11 | |

| May-09 | |

| May-07 | |

| May-05 |

BNY Shares Jump 65% As AI Hiring Push Accelerates

GuruFocus.com

|

| May-01 | |

| Apr-29 | |

| Apr-27 | |

| Apr-23 | |

| Apr-23 |

BNY Mellon High Yield Strategies Fund Declares Dividend

Business Wire

|

| Apr-23 | |

| Apr-22 | |

| Apr-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite