|

|

|

|

|||||

|

|

|

Since March 2021, the S&P 500 has delivered a total return of 72.6%. But one standout stock has more than doubled the market - over the past five years, CACI has surged 180% to $630.12 per share. Its momentum hasn’t stopped as it’s also gained 29.6% in the last six months thanks to its solid quarterly results, beating the S&P by 26.5%.

Is it too late to buy CACI? Find out in our full research report, it’s free.

Founded to commercialize SIMSCRIPT, CACI International (NYSE:CACI) offers defense, intelligence, and IT solutions to support national security and government transformation efforts.

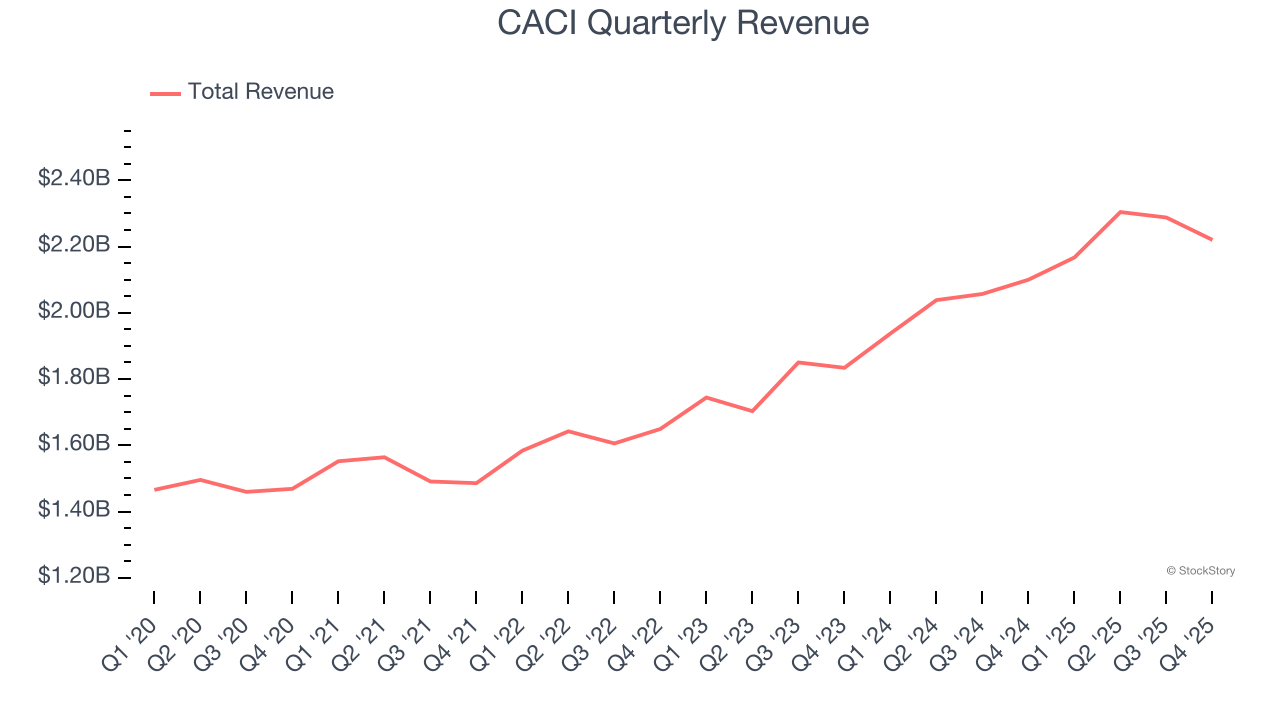

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, CACI’s sales grew at a decent 8.8% compounded annual growth rate over the last five years. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

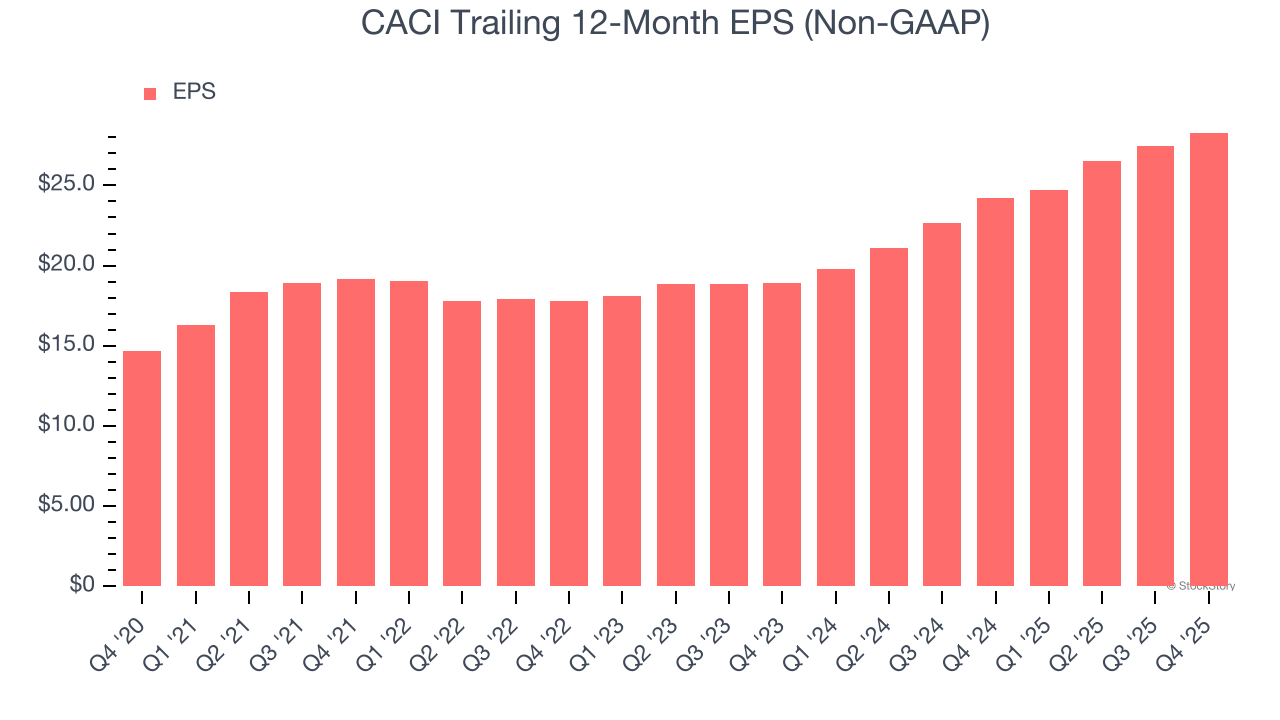

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

CACI’s EPS grew at 14% compounded annual growth rate over the last five years, higher than its 8.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

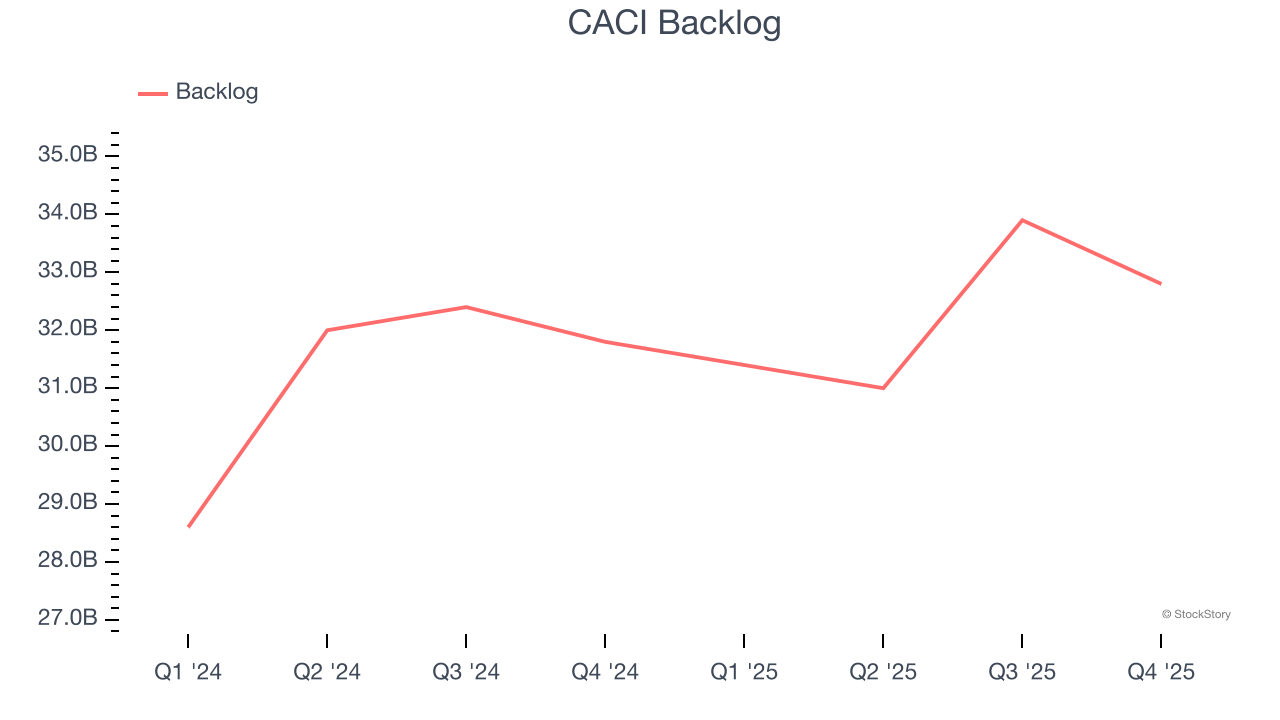

In addition to reported revenue, backlog is a useful data point for analyzing Defense Contractors companies. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into CACI’s future revenue streams.

CACI’s backlog came in at $32.8 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 3.6%. This performance was underwhelming and suggests that increasing competition is causing challenges in winning new orders.

CACI’s merits more than compensate for its flaws, and with its shares topping the market in recent months, the stock trades at 20.6× forward P/E (or $630.12 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| 6 hours | |

| Jul-13 | |

| Jul-13 | |

| Jul-09 | |

| Jul-08 | |

| Jul-07 | |

| Jul-02 | |

| Jul-01 | |

| Jun-22 | |

| Jun-04 | |

| Jun-03 | |

| Jun-02 | |

| May-20 | |

| May-14 | |

| May-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite