|

|

|

|

|||||

|

|

|

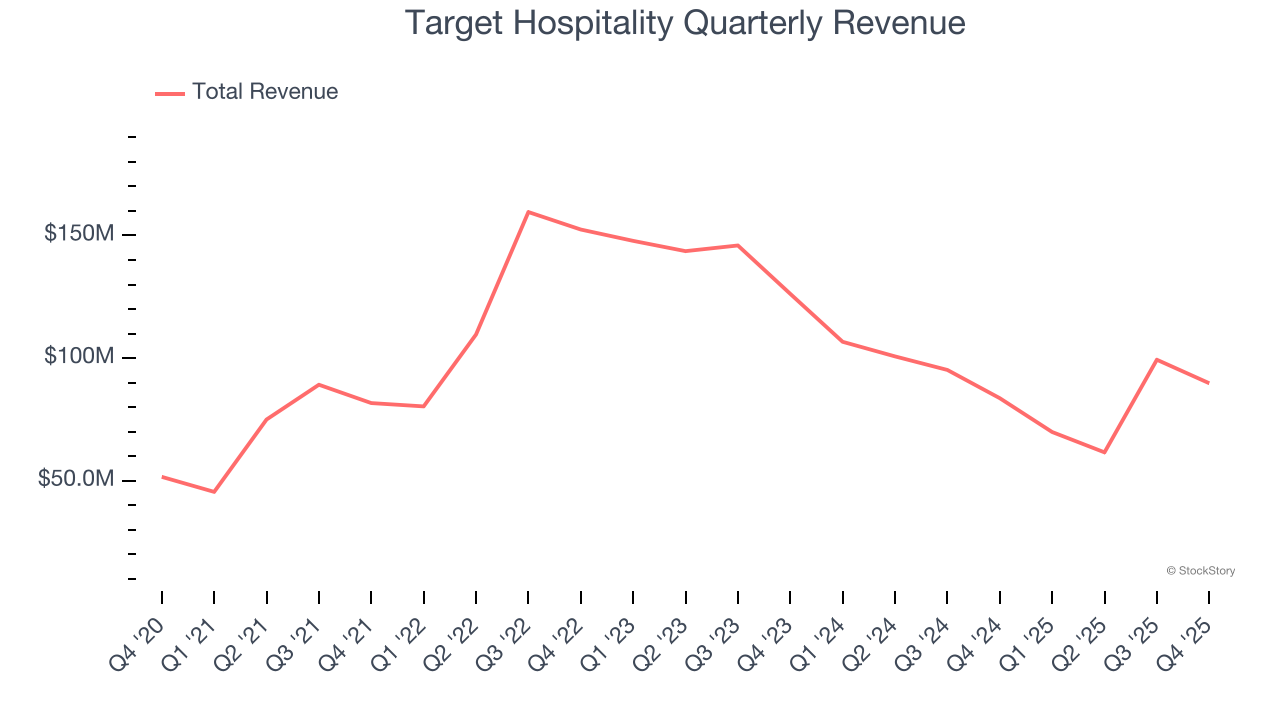

Workforce housing company Target Hospitality (NASDAQ:TH) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 7.3% year on year to $89.78 million. The company’s full-year revenue guidance of $325 million at the midpoint came in 17.7% above analysts’ estimates. Its GAAP loss of $0.15 per share was 45.2% below analysts’ consensus estimates.

Is now the time to buy Target Hospitality? Find out by accessing our full research report, it’s free.

"During 2025 we executed on a clear mandate to advance our strategic agenda—broadening our contract portfolio and accelerating expansion into high-growth end markets. Through disciplined execution, we secured more than $740 million in new multiyear awards since February 2025, underscoring strong demand for our capabilities and validating our entry into high‑value strategic markets," stated Brad Archer, President and Chief Executive Officer.

Building mini-communities at places such as oil drilling sites, Target Hospitality (NASDAQ:TH) is a provider of specialty workforce lodging accommodations and services.

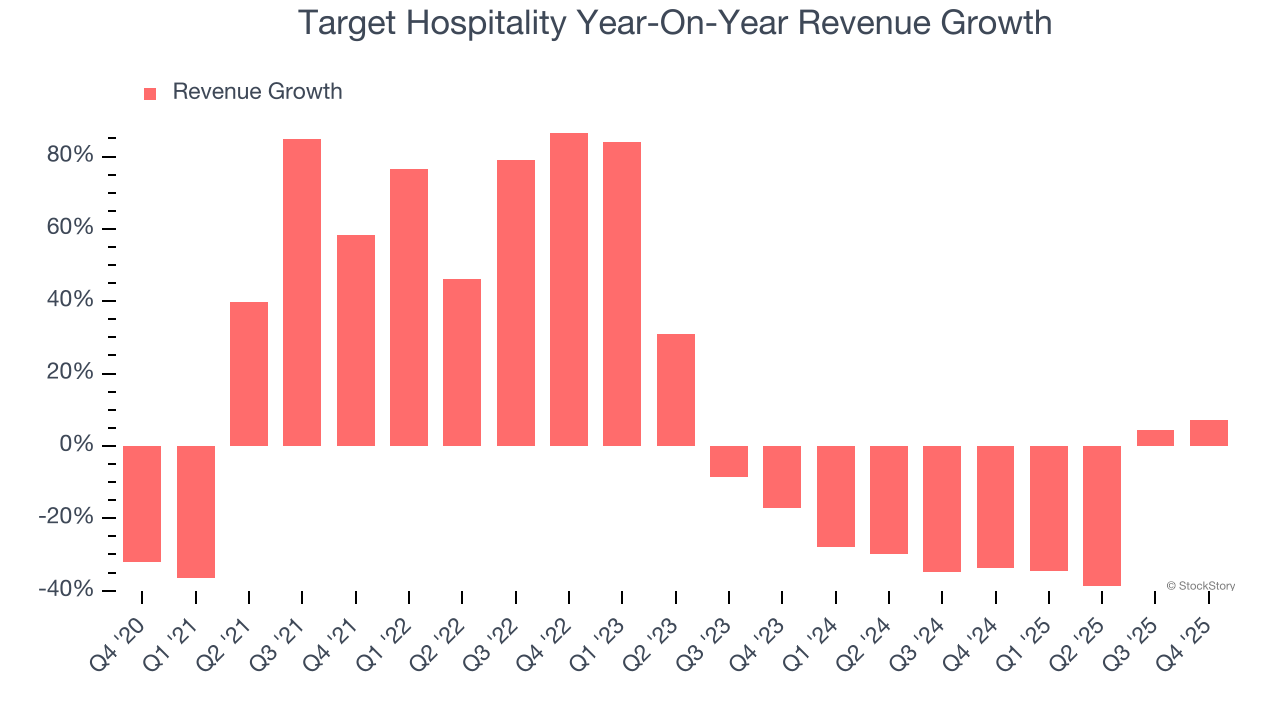

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Target Hospitality’s sales grew at a weak 7.3% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Target Hospitality’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 24.6% annually.

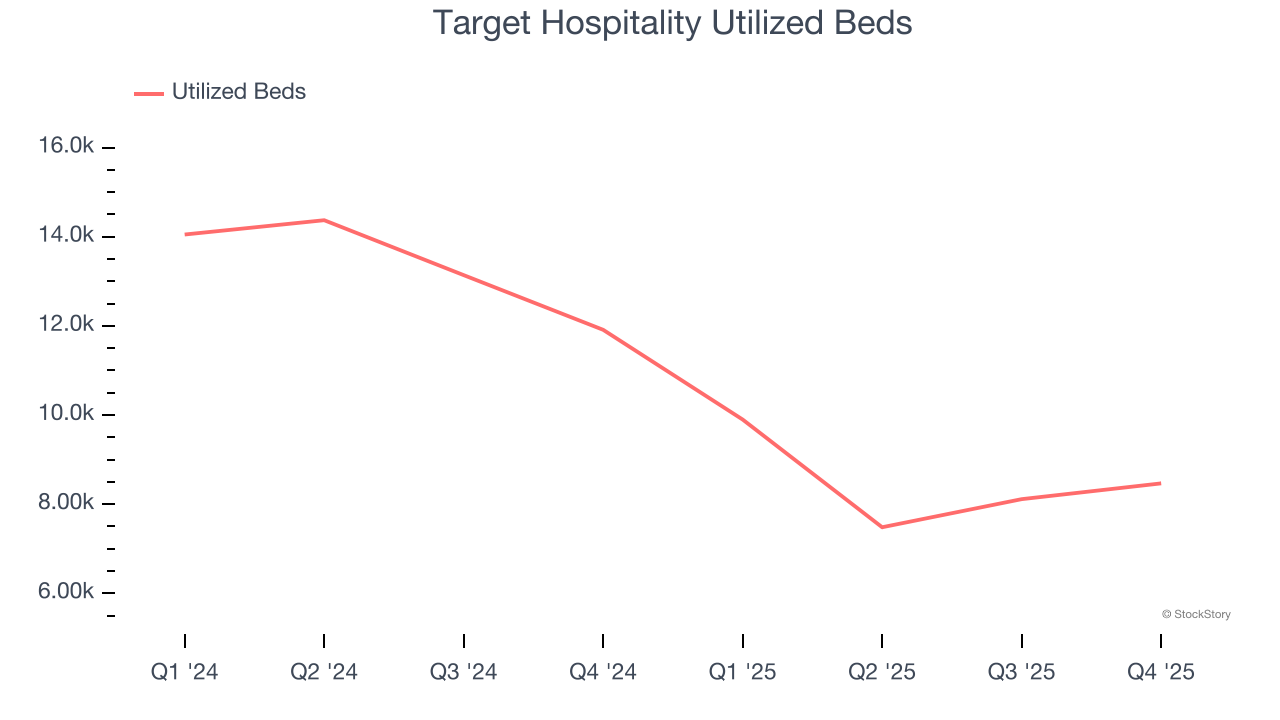

Target Hospitality also discloses its number of utilized beds, which reached 8,466 in the latest quarter. Over the last two years, Target Hospitality’s utilized beds averaged 36.2% year-on-year declines. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Target Hospitality reported year-on-year revenue growth of 7.3%, and its $89.78 million of revenue exceeded Wall Street’s estimates by 4.6%.

Looking ahead, sell-side analysts expect revenue to decline by 11.2% over the next 12 months. Although this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Target Hospitality’s operating margin has shrunk over the last 12 months and averaged 10.5% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q4, Target Hospitality generated an operating margin profit margin of negative 18.7%, down 43.6 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

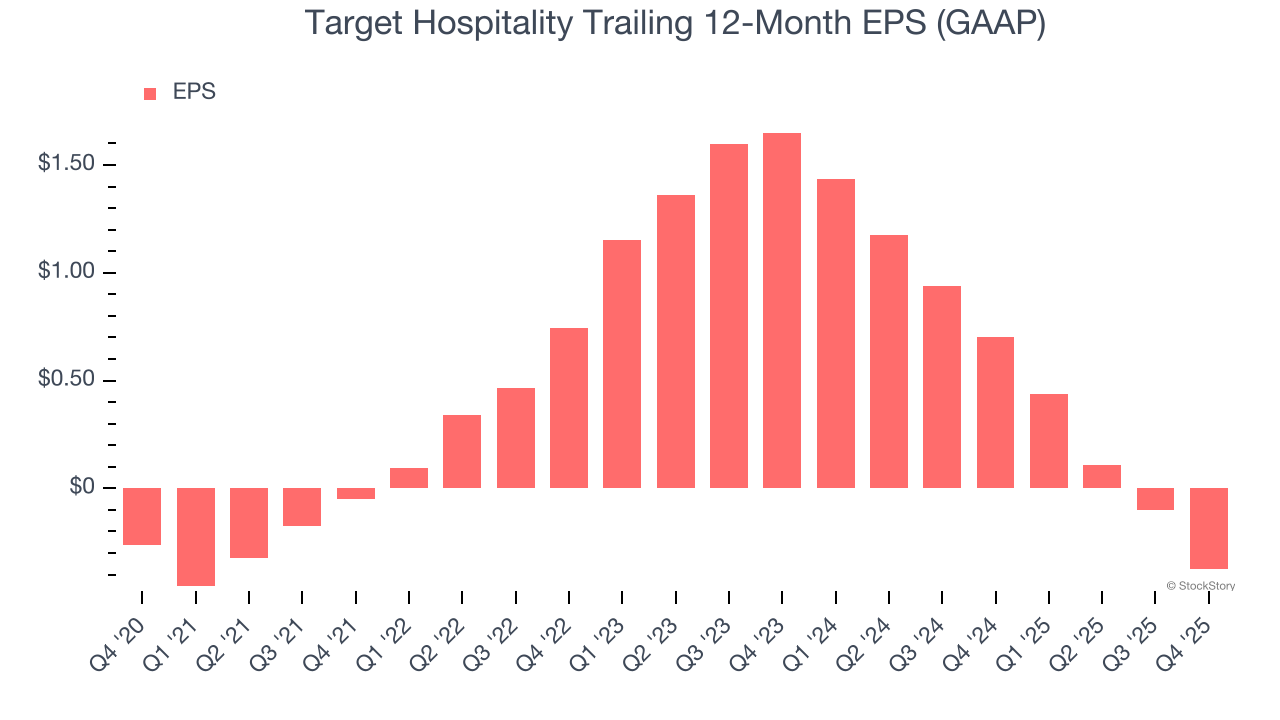

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Target Hospitality’s earnings losses deepened over the last five years as its EPS dropped 7.4% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. Consumer Discretionary companies are particularly exposed to this, and if the tide turns unexpectedly, Target Hospitality’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Target Hospitality reported EPS of negative $0.15, down from $0.12 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Target Hospitality to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.37 will advance to negative $0.21.

Revenue beat convincingly, which is a good start. We were also impressed by Target Hospitality’s optimistic full-year revenue and EBITDA guidance, both of which exceeded analysts’ expectations. On the other hand, its EPS missed and its EBITDA fell short of Wall Street’s estimates. Still, we think this was still a decent quarter with some key metrics above expectations. The stock traded up 4.7% to $8.35 immediately after reporting.

Target Hospitality had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-27 | |

| May-29 | |

| May-12 | |

| May-11 | |

| May-11 | |

| May-08 | |

| May-07 | |

| May-05 | |

| May-05 | |

| Apr-23 | |

| Apr-22 | |

| Apr-21 | |

| Apr-21 | |

| Apr-03 | |

| Apr-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite