|

|

|

|

|||||

|

|

|

Caterpillar Inc. CAT is anticipated to witness year-over-year declines in the top and bottom lines when it reports first-quarter 2025 results on April 30, before the opening bell.

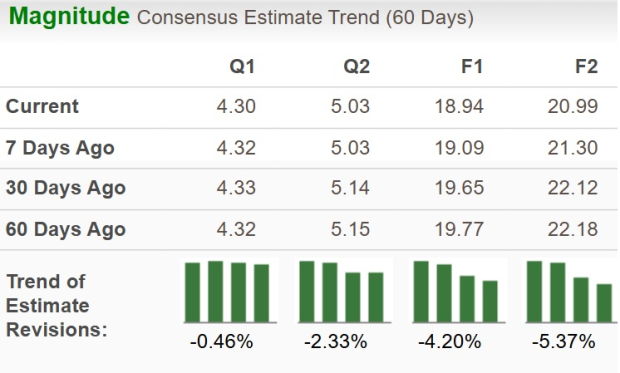

The Zacks Consensus Estimate for CAT’s first-quarter 2025 earnings has moved down 0.46% over the past 60 days to $4.30 per share. The consensus mark implies a 23% decline from the year-ago actual. The Zacks Consensus Estimate for revenues is pegged at $14.54 billion, suggesting an 8% year-over-year decline.

CAT’s earnings outpaced the Zacks Consensus Estimates in three of the trailing four quarters while missing once, the average surprise being 4.53%. This is depicted in the following chart. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

Our proven model does not conclusively predict an earnings beat for Caterpillar this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that is not the case here.

Earnings ESP: CAT has an Earnings ESP of -0.62%. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank of 3. You can see the complete list of today’s Zacks #1 Rank stocks here.

After a prolonged contraction, the manufacturing sector showed signs of recovery at the start of the first quarter of 2025 but soon lost momentum. This was reflected in the Institute for Supply Management’s manufacturing index, with a 50.9% reading in January and 50.3% in February (above 50% indicated expansion) before slipping to 49% in March.

The New Orders Index, which showed expansion with a 55.1% reading in January, dropped sharply to 48.6% in February and further to 45.2% in March (the lowest level since May 2023). Rising concerns over tariffs led customers to scale back orders, a trend likely to be reflected in Caterpillar’s first-quarter order volumes.

Also, CAT’s substantial backlog of $30 billion at the beginning of the first quarter 2025, and higher aftermarket parts and service-related revenues are likely to have supported its first-quarter top line. However, volumes are expected to have been impacted by weak demand in some of its markets.

Overall, lower volumes and pricing are expected to have weighed on CAT’s top-line performance in the quarter under review.

Caterpillar has been witnessing moderate input cost inflation lately. We, thus, expect the company’s cost of sales to decline 6.6% in the first quarter. We, however, anticipate a slight 0.1% increase in selling general and administrative, and research and development costs to be in line with the prior-year quarter.

Our model projects a 25% year-over-year decrease in operating income to $2.55 billion. This factors in the expected decline in revenues, somewhat offset by lower manufacturing costs. We expect the operating margin to be 18.8% in the fourth quarter, implying a decrease from the 22.8% reported in the fourth quarter of 2024.

Our model projects the Resource Industries segment's external sales at $2.72 billion for the first quarter, indicating a 12% year-over-year decline. We expect an 8% dip in volume for the segment and an unfavorable 4.3% pricing. The projection for lower volumes primarily reflects the ongoing weakness in demand.

The segment is expected to report an operating profit of $621 million, suggesting a 15% year-over-year decline. The segment’s operating margin is projected to be 22.8% lower than the 23.6% reported in first-quarter 2024.

The Construction segment’s external sales are projected at $5.38 billion, indicating a decline of 16% from the year-ago quarter’s actual, led by an 11% drop in volume and a 5.3% drop in pricing.

The segment’s operating profit is projected to be $1.39 billion, indicating a year-over-year decline of 21%. We project the segment’s margins to be 25.9%, implying a dip from the year-ago quarter’s actual of 27.5%.

For the Energy and Transportation segment, we expect external sales to be $5.5 billion, suggesting a 0.5% rise from the year-ago quarter’s actual. Volume growth is projected to be 0.1% as improved demand in Power Generation is expected to have been offset by declines in Oil and Gas, Industrial, and Transportation. Pricing is expected to contribute 0.4% to the segment’s sales growth.

Our estimate for the segment’s operating profit is at $1.3 billion for the first quarter of 2025, suggesting a slight dip of 0.3% year over year. The operating margin is projected to be 23.5% for the first quarter of 2025, whereas it registered 23.7% in the first quarter of 2024.

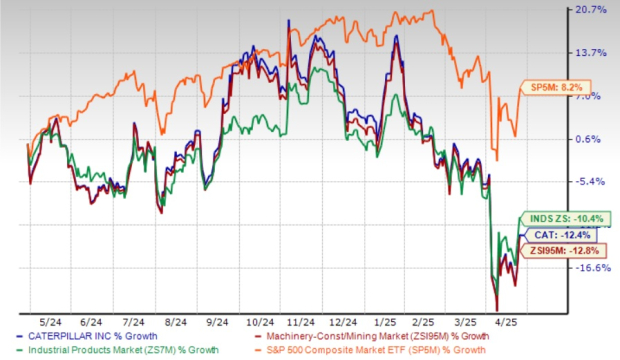

CAT has lost 12.4% in the past year compared with its industry’s 12.8% decline. It has also underperformed the broader Zacks Industrial Products sector’s 10.4% dip and the S&P 500’s climb of 8.2%.

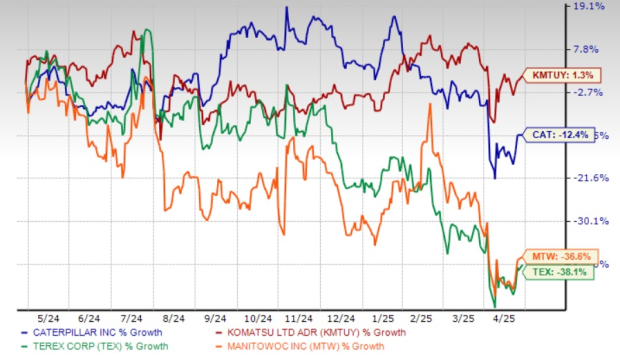

The CAT stock’s performance has been upbeat compared with other companies in the industry, like Terex TEX and The Manitowoc Company MTW, which declined 36.6% and 38.1%, respectively. However, Komatsu KMTUY has fared better with a 1.3% rise.

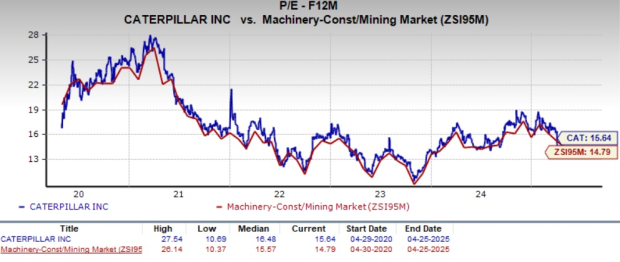

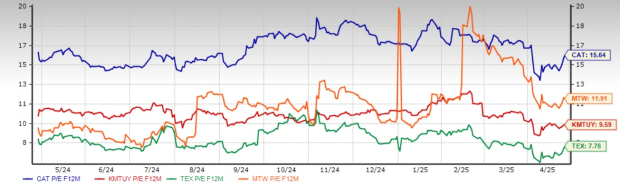

Caterpillar is currently trading at a forward 12-month P/E of 15.64, at a premium compared with the industry’s 14.79X.

The stock is also not cheap when compared with Komatsu, Terex and Manitowoc, all of which are trading at 9.59, 7.76 and 11.91, respectively. Notably, Komatsu, Terex and Manitowoc are trading below the industry’s average.

Despite the current market weakness, Caterpillar’s long-term demand prospects are supported by increased infrastructure spending and the ongoing shift toward clean energy. Its strong market presence, diverse portfolio and innovation position it for improved performance going forward. Expanding its service revenues, which generate higher margins, is a strategic move. A strong balance sheet enables it to invest in growth while making share repurchases and paying dividends. While tariffs are expected to raise costs, CAT’s pricing and cost-cutting efforts can help counter the impacts. Conversely, tariffs on imported goods will boost demand for U.S.-manufactured products. Given Caterpillar’s significant manufacturing presence, it can capitalize on this surge. The company recently announced that COO Joseph Creed would succeed James Umpleby as CEO on May 1. Creed’s ability to navigate CAT through the current challenges will be closely watched.

CAT's performance has always been closely watched by investors, as it serves as a key economic barometer for the sector. Caterpillar’s first-quarter revenues are expected to have been dampened by weaker volumes in the Construction and Resource Industries segments, somewhat offset by improved volumes in the Energy and Transportation segment. Earnings are anticipated to have declined due to weak volumes despite favorable manufacturing costs. This is likely to have been the third quarter of decline in earnings for the company after an enviable stint of growth for 14 straight quarters.

No matter how the upcoming quarterly results play out, investors who already own CAT should retain its shares in their portfolios to benefit from its solid long-term fundamentals. However, given its premium valuation and the ongoing decline in revenues and earnings, new investors can wait for a better entry point.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite