|

|

|

|

|||||

|

|

|

Carter's, Inc. CRI announced its first-quarter 2025 results, wherein the top and bottom lines beat the Zacks Consensus Estimate. However, on a year-over-year basis, the company’s sales and earnings declined.

Carter’s shares plummeted more than 10% on Friday after the company reported weak first-quarter 2025 results and announced the suspension of its financial guidance. This decline was also attributed to the recent CEO transition, as the new leadership team is likely to take time to fully assess the business and establish a strategic path for sustainable growth.

In addition, the current tariff environment has introduced significant uncertainty, making it difficult to predict the company’s future financial performance. As a result, Carter’s has decided to suspend providing guidance until there is more clarity on the internal operational direction and external market conditions.

Carter’s adjusted earnings per share (EPS) of 66 cents per share surpassed the Zacks Consensus Estimate of 53 cents per share. However, the bottom line fell 36.5% from $1.04 reported in the prior-year quarter. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

Carter's, Inc. price-consensus-eps-surprise-chart | Carter's, Inc. Quote

The company reported consolidated net sales of $629.8 million, which beat the Zacks Consensus Estimate of $621 million. The metric declined 4.8% from $661.5 million posted in the year-ago period. The decline was due to macroeconomic pressures, including inflation, elevated interest rates and weakening consumer confidence, which reduced demand across segments. Additionally, unfavorable foreign currency translation impacted consolidated net sales by approximately $6.4 million, or 1.0%.

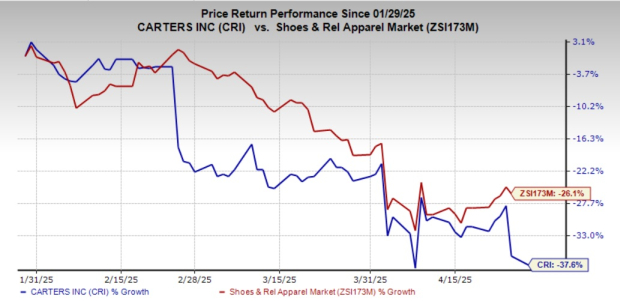

Shares of this Zacks Rank #5 (Strong Sell) company have lost 37.6% in the past three months compared with the industry’s 26.1% decline.

Sales of the U.S. Retail segment decreased 4.3% year over year to $294.4 million. The segment’s comparable net sales fell 5.2% in the first quarter. Our model predicted sales of $289.3 million for the segment.

The U.S. Wholesale segment’s sales fell 5.3% year over year to $250.1 million due to differences in the timing of shipments as compared to the last year. We expected net sales of $245.9 million for the segment.

The International segment witnessed a 4.9% year-over-year drop in sales to $85.3 million. We expected net sales of $86.1 million for the segment.

Gross profit fell 7.6% year over year to $291.1 million. The gross margin contracted 140 basis points (bps) to 46.2% compared with 47.6% in the first quarter of 2025. The decline was largely due to competitive pricing within the U.S. Retail segment and the negative impact of FX on product costs in Canada and Mexico. However, the impact of lower prices was mostly offset by reduced product costs and a favorable channel mix with a lower mix of wholesale sales.

Adjusted operating income decreased 35.7% year over year to $35.4 million. The adjusted operating margin decreased 270 bps to 5.6%, impacted by investments in pricing, fixed cost deleverage, and costs related to leadership transition and operating model improvement initiatives.

Adjusted Selling, general and administrative (SG&A) expenses declined 2% year over year to $261 million in the quarter. As a percentage of net sales, SG&A expenses increased 130 bps year over year to 41.4%.

Carter’s ended first-quarter 2025 with cash and cash equivalents of $320.9 million, long-term debt of $498.3 million and shareholders’ equity of $847.3 million.

In the first quarter of 2025, the company returned $29 million to its shareholders through cash dividends. It paid a cash dividend of 80 cents per common share in the quarter. There were no share repurchases in the first quarter.

We have highlighted three better-ranked stocks, namely, Under Armour UAA, G-III Apparel Group, Ltd. GIII and Duluth Holdings DLTH.

Under Armour is one of the leading designers, marketers and distributors of authentic athletic footwear, apparel and accessories for a wide variety of sports and fitness activities in the United States and internationally. It has a Zacks Rank of 2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for UAA’s fiscal 2024 sales and earnings indicates declines of 9.8% and 44.4%, respectively, from the year-ago reported figures. Under Armour delivered an earnings surprise of 98.6% in the trailing four quarters, on average.

G-III Apparel is a manufacturer, designer and distributor of apparel and accessories under licensed brands, owned brands and private label brands. It carries a Zacks Rank #2 at present.

The Zacks Consensus Estimate for GIII’s fiscal 2025 earnings and revenues implies declines of 4.5% and 1.2%, respectively, from the year-ago actuals. GIII delivered a trailing four-quarter average earnings surprise of 117.8%.

Duluth Holdings, a casual wear, workwear and accessories dealer, currently carries a Zacks Rank #2. Duluth Holdings has a trailing four-quarter earnings surprise of 37.2%, on average.

The Zacks Consensus Estimate for DLTH’s current financial-year EPS indicates growth of 5.6% from the year-ago figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-13 | |

| Jul-08 | |

| Jul-01 | |

| Jul-01 | |

| Jun-30 | |

| Jun-26 | |

| Jun-25 | |

| Jun-22 | |

| Jun-18 | |

| Jun-17 | |

| Jun-17 | |

| Jun-16 | |

| Jun-15 | |

| Jun-12 | |

| Jun-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite