|

|

|

|

|||||

|

|

|

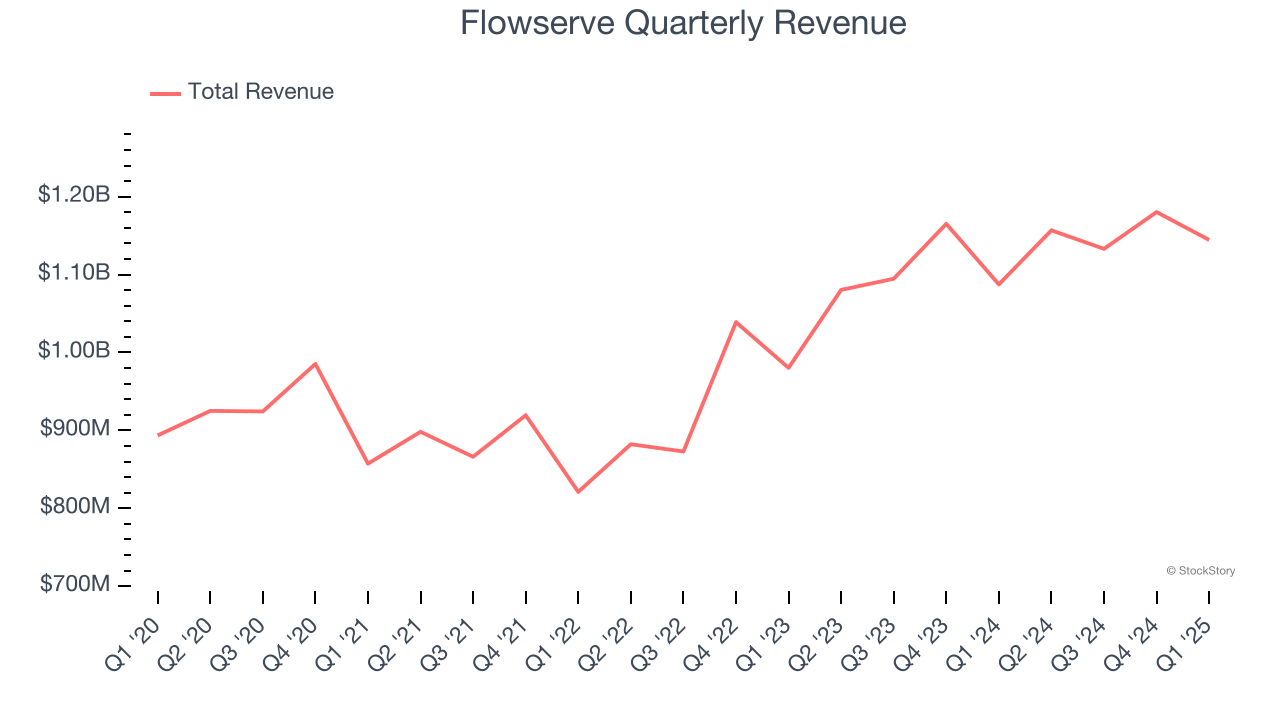

Flow control equipment manufacturer Flowserve (NYSE:FLS) announced better-than-expected revenue in Q1 CY2025, with sales up 5.2% year on year to $1.14 billion. Its non-GAAP profit of $0.72 per share was 19.6% above analysts’ consensus estimates.

Is now the time to buy Flowserve? Find out by accessing our full research report, it’s free.

“Our first quarter results were a strong start to the year, with robust bookings growth, margin expansion, and earnings acceleration all driven by healthy end markets and improved execution. These results demonstrate the strength of our diversified portfolio and the exceptional performance of our associates around the world operating under the Flowserve Business System,” said Scott Rowe, Flowserve’s President and Chief Executive Officer.

Manufacturing the largest pump ever built for nuclear power generation, Flowserve (NYSE:FLS) manufactures and sells flow control equipment for various industries.

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

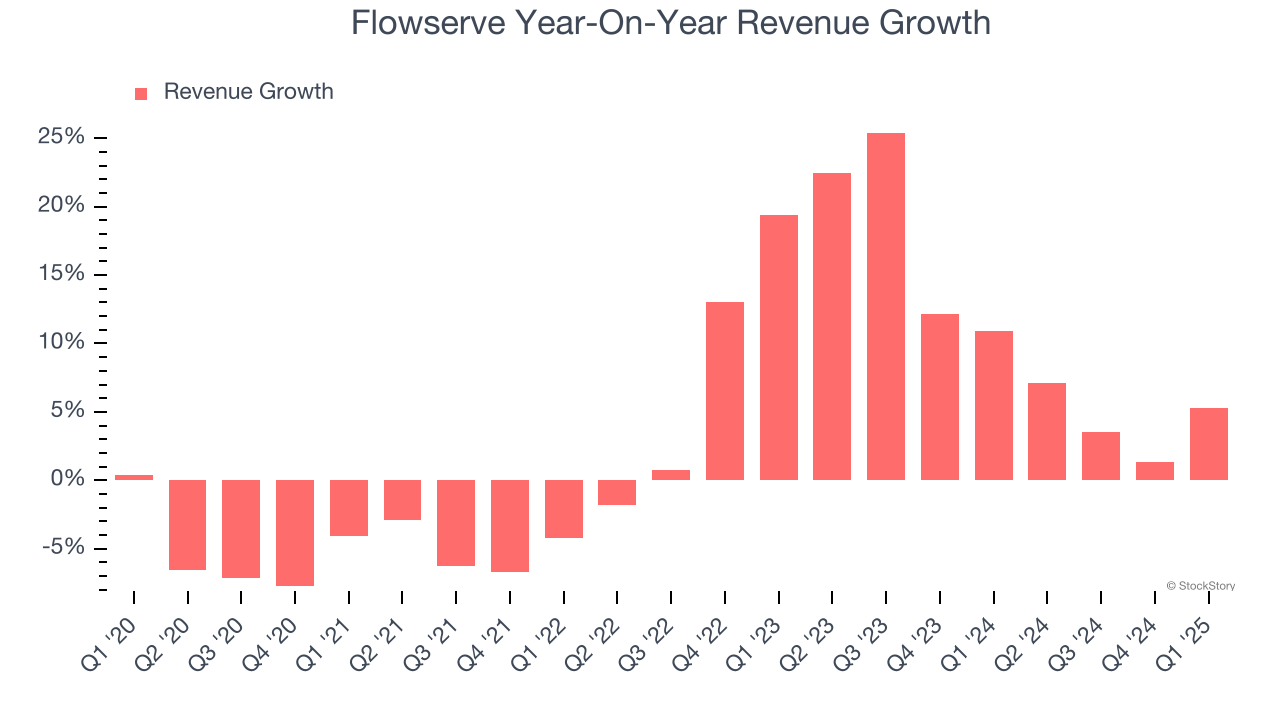

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Flowserve’s sales grew at a sluggish 3.2% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Flowserve’s annualized revenue growth of 10.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

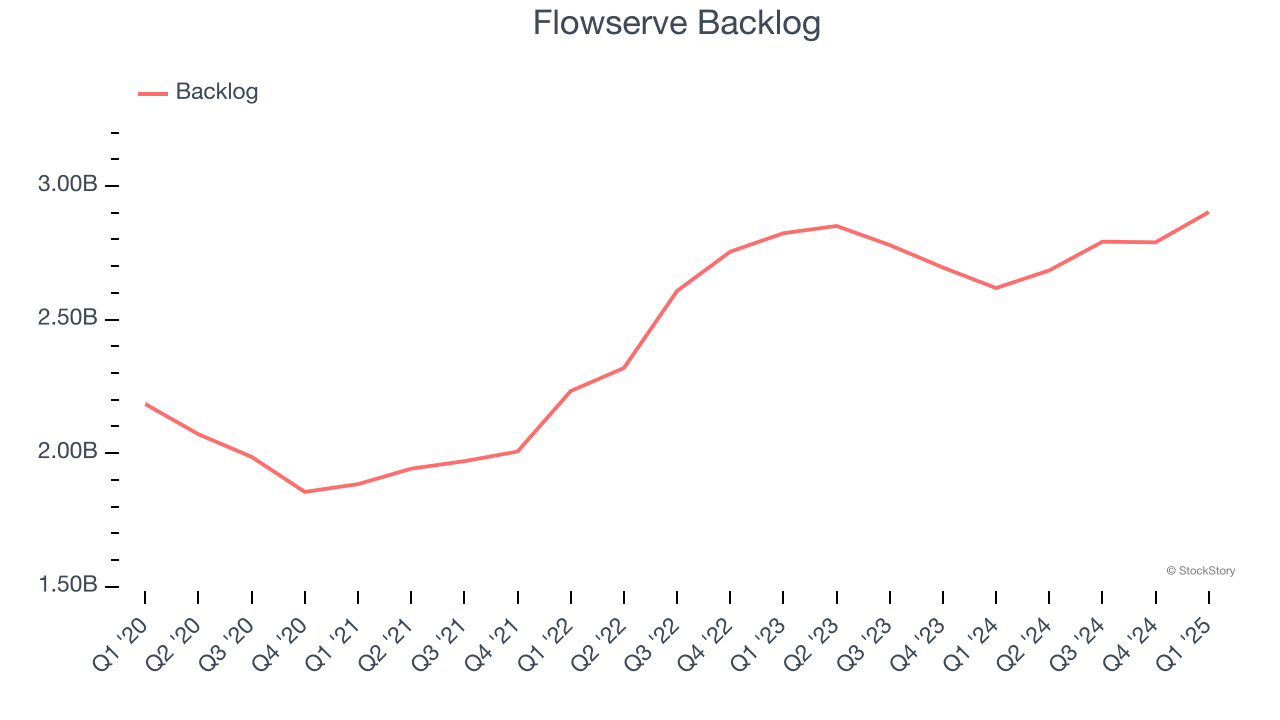

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Flowserve’s backlog reached $2.9 billion in the latest quarter and averaged 3.6% year-on-year growth over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies Flowserve was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, Flowserve reported year-on-year revenue growth of 5.2%, and its $1.14 billion of revenue exceeded Wall Street’s estimates by 3.6%.

Looking ahead, sell-side analysts expect revenue to grow 4.7% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

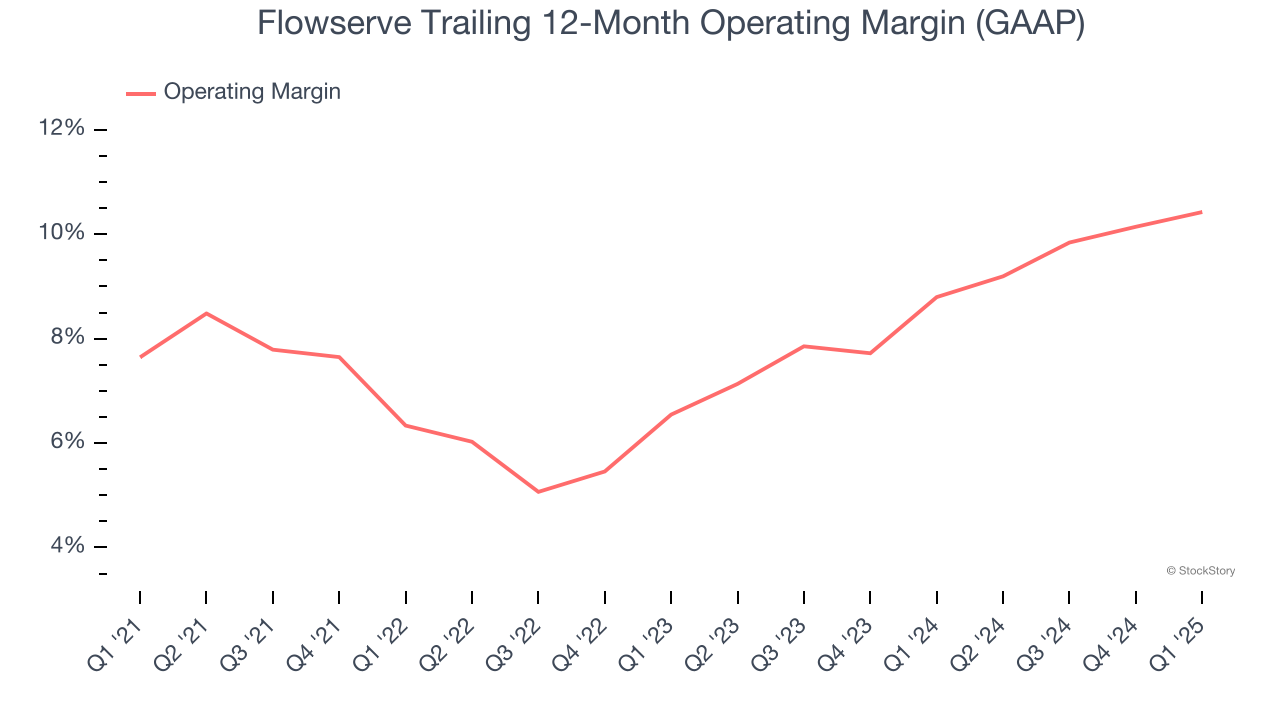

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Flowserve has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.1%, higher than the broader industrials sector.

Looking at the trend in its profitability, Flowserve’s operating margin rose by 2.8 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, Flowserve generated an operating profit margin of 11.5%, up 1.1 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

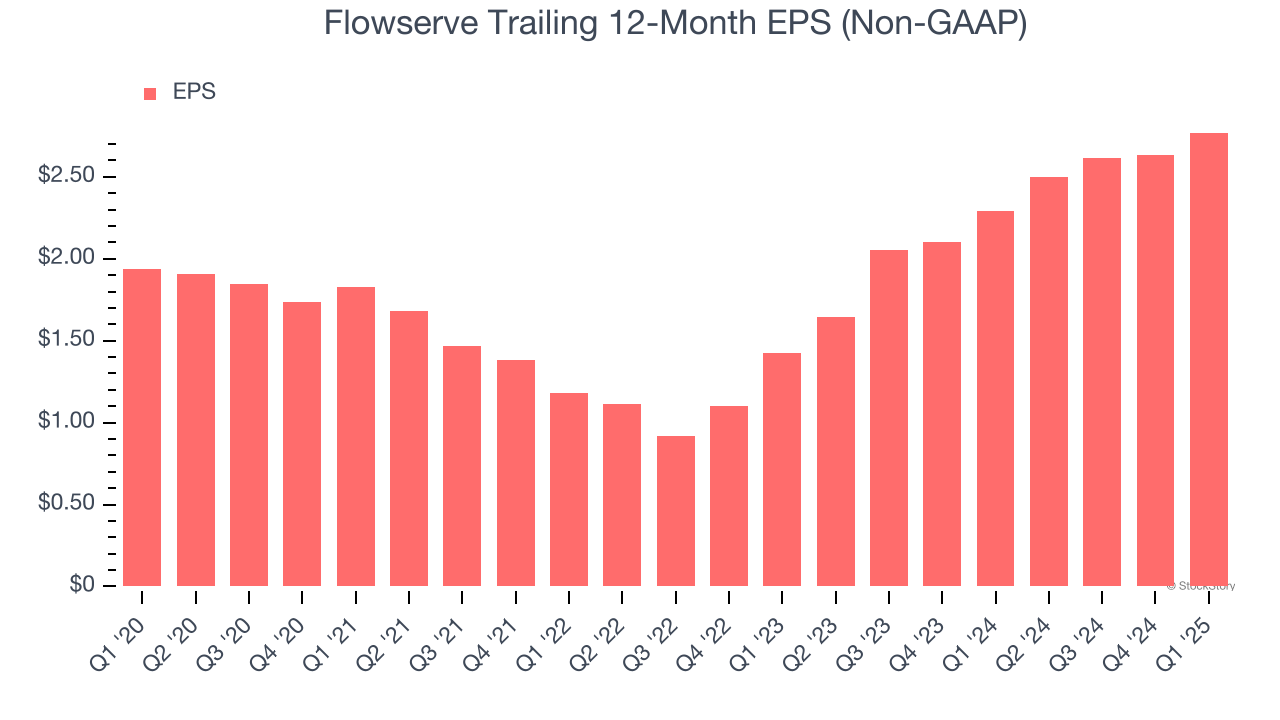

Flowserve’s EPS grew at an unimpressive 7.4% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 3.2% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Flowserve’s earnings can give us a better understanding of its performance. As we mentioned earlier, Flowserve’s operating margin expanded by 2.8 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Flowserve, its two-year annual EPS growth of 39.4% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q1, Flowserve reported EPS at $0.72, up from $0.58 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Flowserve’s full-year EPS of $2.77 to grow 16.5%.

We were impressed by how significantly Flowserve blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a good quarter with some key areas of upside. The stock traded up 7.4% to $48.19 immediately after reporting.

Flowserve had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-15 | |

| Feb-13 | |

| Feb-12 | |

| Feb-09 | |

| Feb-09 | |

| Feb-06 | |

| Feb-06 | |

| Feb-06 | |

| Feb-06 | |

| Feb-06 | |

| Feb-06 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite