|

|

|

|

|||||

|

|

|

Amid escalating global tensions and renewed geopolitical flashpoints — ranging from Eastern Europe to the Indo-Pacific — defense spending is currently under a bright spotlight. For investors, this presents a compelling opportunity in the defense sector, where industry giants like Lockheed Martin LMT and General Dynamics GD stand to benefit.

Lockheed, known for its fighter jets and missile systems, is the largest U.S. defense contractor with a broad portfolio. General Dynamics, with exposure to both commercial and defense markets, spans aerospace, marine systems and defense IT. As global defense spending rises, both firms are positioned for growth. But which stock presents a better investment opportunity today? Let’s dive deeper to find out.

Recent Achievements: The company ended the first quarter of 2025 with decent year-over-year sales growth of 4% and a solid 16.9% improvement in operating profit, which translated into a 15% enhancement in its quarterly bottom line.

Among its recent milestones, worth mentioning is Lockheed’s Sikorsky division signing a long-term agreement in April 2025 with Bristow Group Inc. to support the world’s largest S-92 helicopter fleet. The same month, LMT announced plans to acquire Amentum’s Rapid Solutions business, a proven multi-domain provider of technologies, such as airborne and space ISR, advanced communications and tactical systems. These contract wins and acquisitions are likely to strengthen LMT’s position in the defense industry and help maintain its strong quarterly performance (like its latest results).

Financial Stability: Lockheed generated cash and cash equivalent of $1.80 billion as of March 30, 2025. Its current debt was $1.64 billion, while its long-term debt totaled $18.66 billion. So, we may safely conclude that the company holds a moderate solvency position, at least in the near term. This should allow it to continue investing in new defense technologies, a critical growth catalyst for defense primes like LMT (to help maintain their competitive position in the industry).

Challenges to Note: In April 2025, the U.S. Government implemented sweeping new tariffs, including a baseline 10% on all imports, a 25% duty on steel and aluminum from all countries, and significantly higher rates on imports from select nations like Canada and Mexico. Additionally, U.S. actions concerning rare earth minerals (critical to LMT’s products), such as import restrictions and China’s export controls, may limit material availability over time.

These trade measures, along with potential retaliatory tariffs by other nations, could lead to shortages of essential raw materials and adversely impact LMT’s manufacturing capabilities and operating performance. Furthermore, U.S. sanctions on specific Turkish entities expose LMT to the risk of incurring substantial reach-forward losses tied to its involvement in the Turkish Utility Helicopter Program.

Recent Achievements: The company ended the first quarter of 2025 with a decent year-over-year sales growth rate of 13.9% and a solid 22.4% improvement in operating profit. This translated into a 27.1% enhancement in its quarterly bottom line.

Among its recent milestones, worth mentioning is General Dynamics’ all-new Gulfstream G800, the world’s longest-range business aircraft, which earned type certification from the Federal Aviation Administration (FAA) and certification from the European Union Aviation Safety Agency (EASA) in April 2025. In March, the company won a contract modification worth $1 billion, allowing its Electric Boat unit to purchase long-lead-time materials for Virginia Class Block VI submarines. While such contract wins bolster GD’s backlog count, the certifications awarded for its jet should allow it to market its products commercially, both of which boost the company’s revenue prospects.

Financial Stability: General Dynamics generated a cash and cash equivalent of $1.24 billion as of March 31, 2025. Its current debt was $2.35 billion, while its long-term debt totaled $7.26 billion. So, we may safely conclude that the company holds a weak solvency position, which might restrict this defense prime’s ability to invest in technological advancement of its products, thereby limiting its long-term growth value.

Challenges to Note: A shortage in the supply of aircraft parts, ranging from small hardware like nuts and bolts to specialized items like cockpit windows and engine components, has been adversely impacting the aerospace sector. The majority of industry analysts currently expect the shortage of aircraft parts to persist throughout 2025. Such lingering supply-chain constraints may lead to a delay in the delivery of products from General Dynamics, thereby adversely impacting its future results of operations.

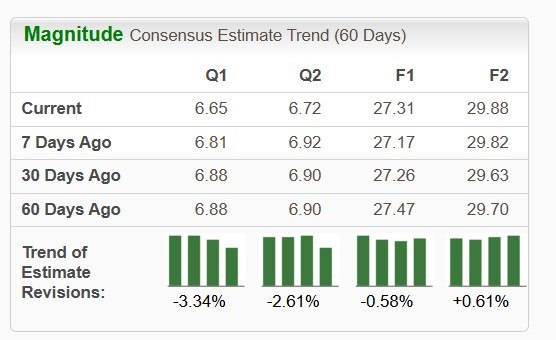

The Zacks Consensus Estimate for Lockheed’s 2025 sales suggests a rise of 5.2% from the year-ago quarter’s reported figure, while that for its earnings per share (EPS) implies a decline of 4.1%. The stock’s bottom-line estimates have been trending downward over the past 60 days, except for 2026.

The Zacks Consensus Estimate for General Dynamics’ 2025 sales implies a year-over-year improvement of 5.8%, while that for its EPS suggests a 9.4% rise. The stock’s near-term bottom-line estimates, however, have been trending southward over the past 60 days, except for the second quarter of 2025.

LMT (up 2.8%) has underperformed GD (up 5.9%) over the past three months but has outpaced the same in the past year. Shares of LMT have surged 3%, while those of GD have lost 5.1% over the past year.

LMT is trading at a forward earnings multiple of 16.91X, below GD’s 17.49X.

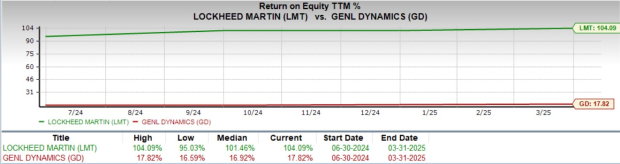

A comparative analysis of both these stocks’ Return on Equity (ROE) suggests that GD is less efficient at generating profits from its equity base than LMT.

In today’s volatile geopolitical climate, both Lockheed and General Dynamics are well-positioned to benefit from increased global defense spending.

Lockheed offers a more diversified defense portfolio, stronger return on equity and better valuation metrics, while recent acquisitions and contract wins enhance its growth prospects. General Dynamics, despite strong recent earnings and achievements in both aerospace and defense segments, faces greater solvency concerns and persistent supply-chain disruptions.

While both stocks currently carry a Zacks Rank #3 (Hold), Lockheed’s financial stability, strategic positioning and track record of operational efficiency make it the more compelling investment choice. That said, investors should monitor evolving risks and market conditions closely before making a final decision.

You can see the complete list of today’s Zacks Rank #1 (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite