|

|

|

|

|||||

|

|

|

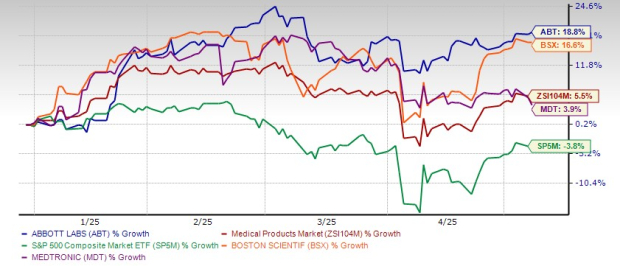

Despite facing a challenging industry-wide investment climate driven by tariffs, Abbott ABT has managed to achieve an 18.8% gain so far in 2025, outperforming the industry, its benchmark, and the company’s main competitors. During this period, while the broader Medical Products industry grew 5.5%, the S&P 500 index declined 3.8%.

Year to date, the company’s archrivals like Boston Scientific BSX and Medtronic MDT have risen 16.6% and 3.9%, respectively.

The escalating tariff environment is beginning to weigh heavily on the financial outlook of key MedTech players, with Abbott, Boston Scientific and Medtronic all facing varying degrees of exposure. Abbott expects “a few hundred million dollars” in tariff-related costs for 2025, which it currently considers manageable. However, its reliance on a global supply chain and imported high-margin devices could lead to rising cost pressure from the third quarter onward. While strong early-year performance offers a buffer, prolonged tariffs pose risks to margins and supply chain stability.

Boston Scientific, on the other hand, expects a $200 million tariff impact in 2025 but aims to offset it through sales growth, spending cuts and a minor FX gain. With reaffirmed EPS guidance and margin expansion plans, Boston Scientific shows operational confidence. However, the delayed tariff impact in the second half may challenge its ability to maintain momentum and cost discipline.

Medtronic, with a major manufacturing presence in Mexico and Canada, is perhaps the most geopolitically entangled. The upcoming May 21 earnings release may shed light on how exposed the company is to cross-border tariff disruptions. Given its diverse portfolio, which ranges from insulin delivery systems to surgical robots, Medtronic could face not only higher production costs but also potential delays in market access if retaliatory tariffs or regulatory bottlenecks emerge.

Despite trade policy challenges, Abbott’s global footprint and 90 manufacturing sites offer flexibility to manage regional risks and reroute supply chains. Management is exploring long-term strategies to reduce tariff exposure, including localizing production, optimizing supplier contracts, while potentially offsetting costs through pricing adjustments.

Abbott’s Diagnostics segment, accounting for 20% of first-quarter 2025 revenues, is showing strong long-term growth potential, driven by rising global demand for routine testing, particularly for respiratory diseases like flu, strep, and RSV across diverse healthcare settings. A recent major account win supports continued momentum. Core Lab Diagnostics (excluding China) grew 6.5% in the first quarter. Abbott’s $0.5 billion investment in new manufacturing and R&D facilities in Illinois and Texas aims to expand its U.S. transfusion diagnostics business. Moreover, the upcoming launch of the Alinity m system marks Abbott's entry into the molecular nucleic acid testing segment — a $1 billion market opportunity.

Within Established Pharmaceuticals Division (EPD), the company is progressing strategically. EPD operates solely in emerging geographies, with leading positions in many of the largest and fastest-growing pharmaceutical markets for branded generics in the world. Banking on the successful execution of its Branded Generic operating model, EPD is well-positioned for sustained growth in many of these growing pharmaceutical markets. Focusing on the therapies most needed in the faster-growing markets, Abbott continues to sustain its long track record of delivering strong growth, which includes a five-year CAGR for EPD of 8%. Further, Abbott’s strategic focus on biosimilars strengthens its prospects, with the company now securing rights to 15 biosimilar products across key therapeutic areas.

Abbott’s Medical Devices business also shows strong long-term growth potential, supported by solid sales across key areas. Diabetes Care led the way with more than 20% growth in glucose monitors, especially in the United States. Structural Heart and Electrophysiology also posted strong gains, helped by the early launch of the Volt PFA system and increasing use of TriClip. Abbott is expanding in Heart Failure with broader coverage for CardioMEMS and growing its Vascular business with new trials like its coronary lithotripsy system. The company is also entering new markets, such as neuromodulation for treatment-resistant depression, a $1 billion opportunity.

Overall, Abbott’s innovation and broad product portfolio position it well for future growth.

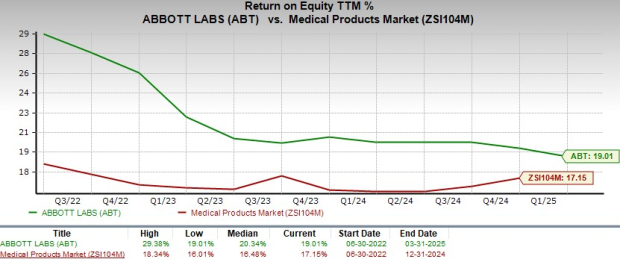

ABT’s trailing 12-month return on equity (ROE) of 19.01% outpaces the average earned by companies in the Medical Products industry (17.15%). This superior ROE underscores Abbott’s efficient management and ability to generate strong returns for shareholders, further reinforcing its investment appeal.

Further, Abbott is currently trading above both its 50-day simple moving average (SMA) and 200-day SMA. Despite its short-term bearishness in the form of macro complexities, this technical setup indicates that the stock is performing well in both the short and long term. These favorable SMAs may now serve as important support levels, providing a cushion against potential price pullbacks due to external pressure.

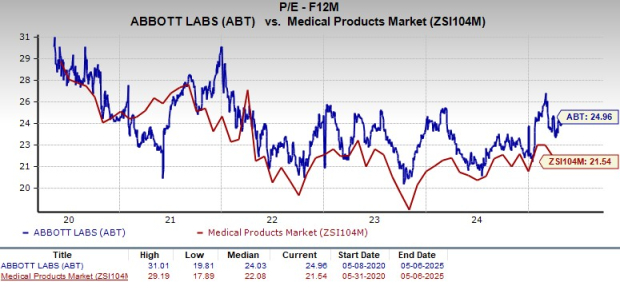

From a valuation standpoint, Abbott’s forward 12-month price-to-earnings (P/E) is 24.96X, a premium to the industry average of 21.54X.

The company is also trading at a significant premium to industry players like Medtronic, with its current P/E being 14.1. However, Boston Scientific, with a current P/E of 34.34X, appears more stretched.

Despite its adaptive strategies, Abbott's stock price has not fully reflected the company’s underlying strength. The subdued market reaction to its positive first-quarter results suggests that investors remain cautious amid geopolitical uncertainty, mainly in the form of retaliating tariffs.

The current stretched valuation suggests that investors may be paying a higher price relative to the company's expected earnings growth. While the impressive performance in the first quarter boosted investor sentiment, this might not be the ideal time to invest in Abbott. The short-term hiccups in the form of international trade challenges are limiting the stock’s near-term gains.

Accordingly, while current shareholders should hold their positions, new investors should wait for a better entry point.

Abbott currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 2 hours | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite