|

|

|

|

|||||

|

|

|

Ruger trades at $36.03 per share and has stayed right on track with the overall market, losing 6.5% over the last six months while the S&P 500 is down 2.4%. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Ruger, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Even though the stock has become cheaper, we don't have much confidence in Ruger. Here are three reasons why we avoid RGR and a stock we'd rather own.

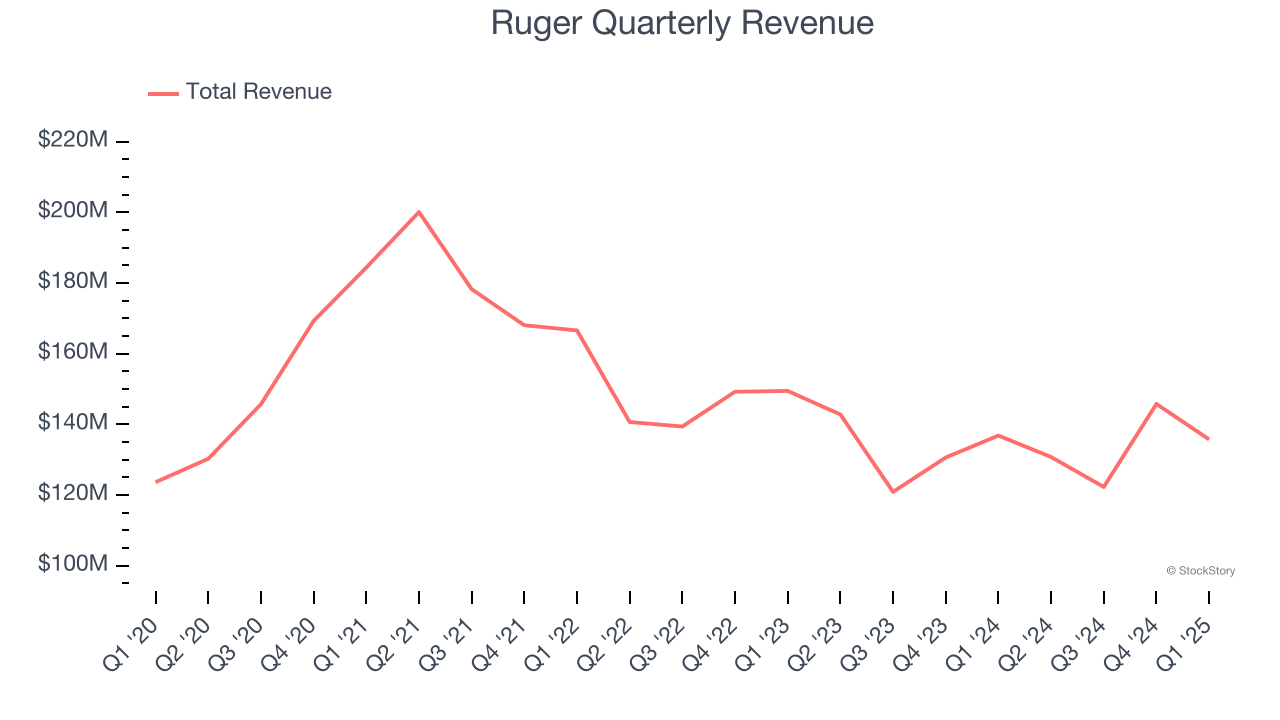

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Ruger’s sales grew at a sluggish 4.9% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector.

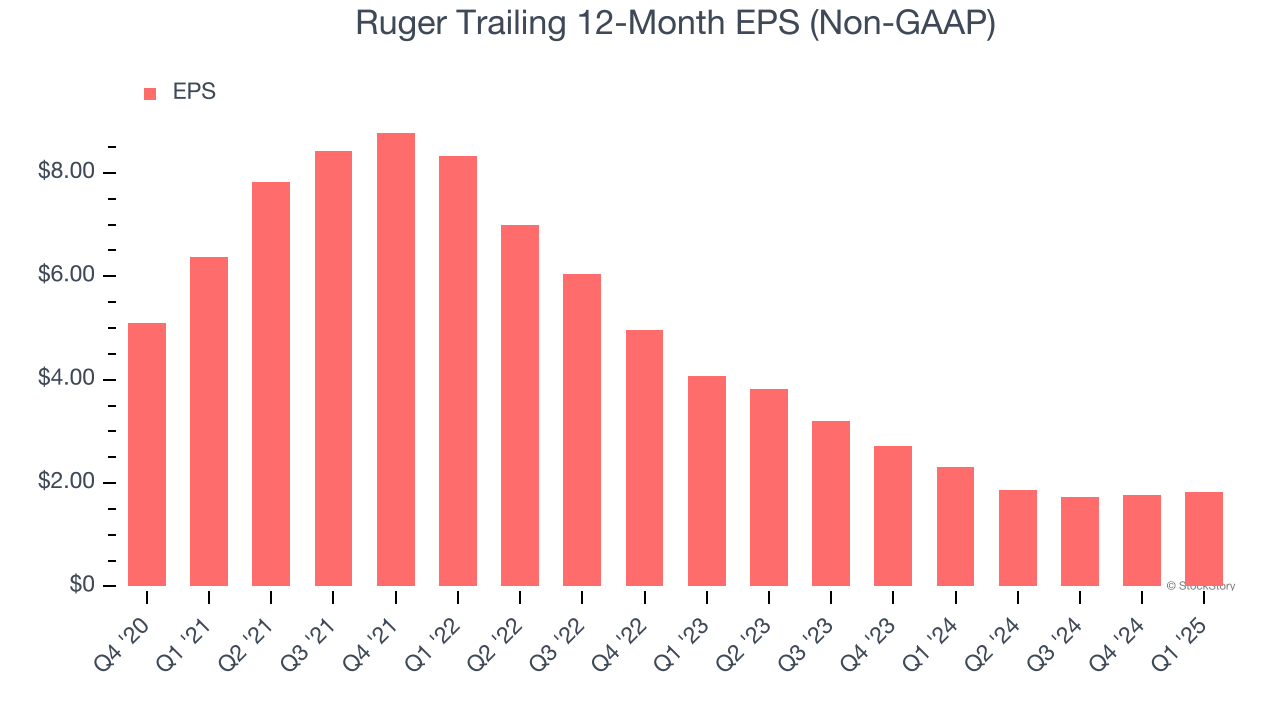

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Ruger’s full-year EPS dropped 159%, or 26.8% annually, over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. Consumer Discretionary companies are particularly exposed to this, and if the tide turns unexpectedly, Ruger’s low margin of safety could leave its stock price susceptible to large downswings.

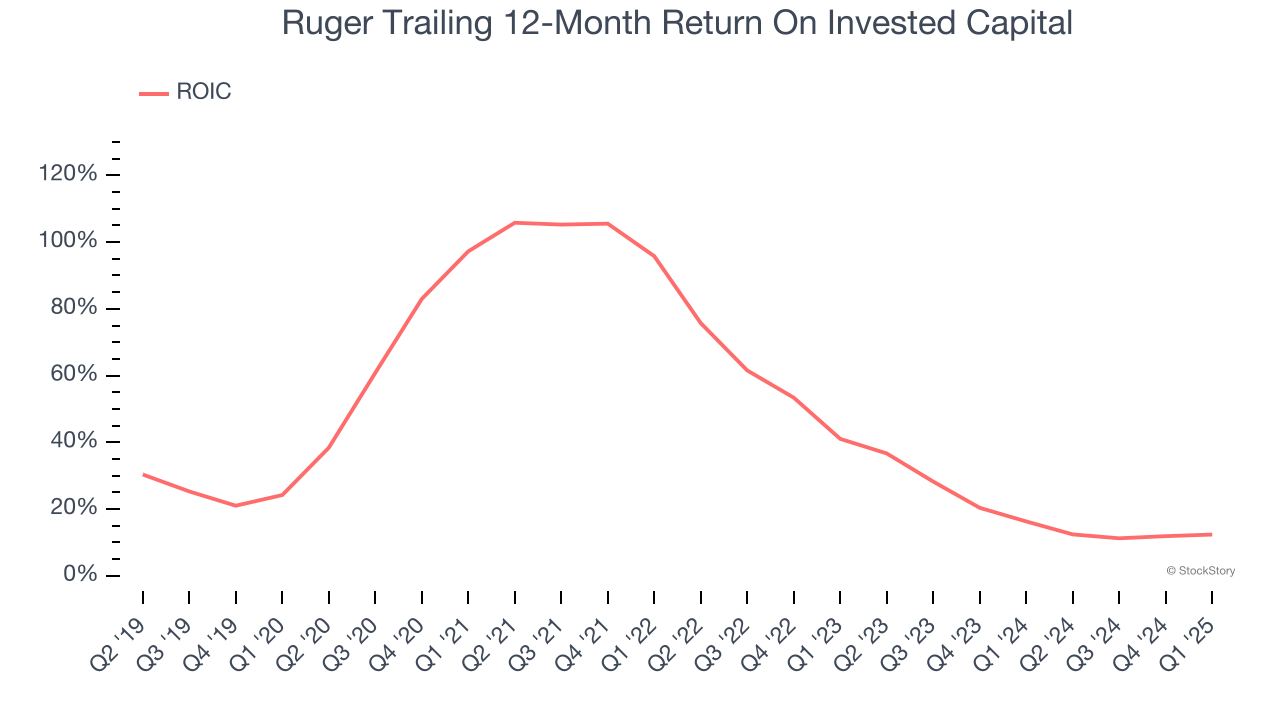

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Ruger’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Ruger doesn’t pass our quality test. After the recent drawdown, the stock trades at 11.1× forward EV-to-EBITDA (or $36.03 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d recommend looking at the Amazon and PayPal of Latin America.

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-15 | |

| Jun-18 | |

| May-15 | |

| May-08 | |

| May-07 | |

| May-06 | |

| May-06 | |

| May-05 | |

| May-04 | |

| Apr-22 | |

| Apr-21 |

Inside the Nasty Fight Between Two of the World's Most Storied Gun Makers

RGR

The Wall Street Journal

|

| Mar-31 | |

| Mar-27 | |

| Mar-25 | |

| Mar-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite