|

|

|

|

|||||

|

|

|

As the Q1 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the consumer subscription industry, including Bumble (NASDAQ:BMBL) and its peers.

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

The 8 consumer subscription stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 1.9% while next quarter’s revenue guidance was in line.

Luckily, consumer subscription stocks have performed well with share prices up 16.6% on average since the latest earnings results.

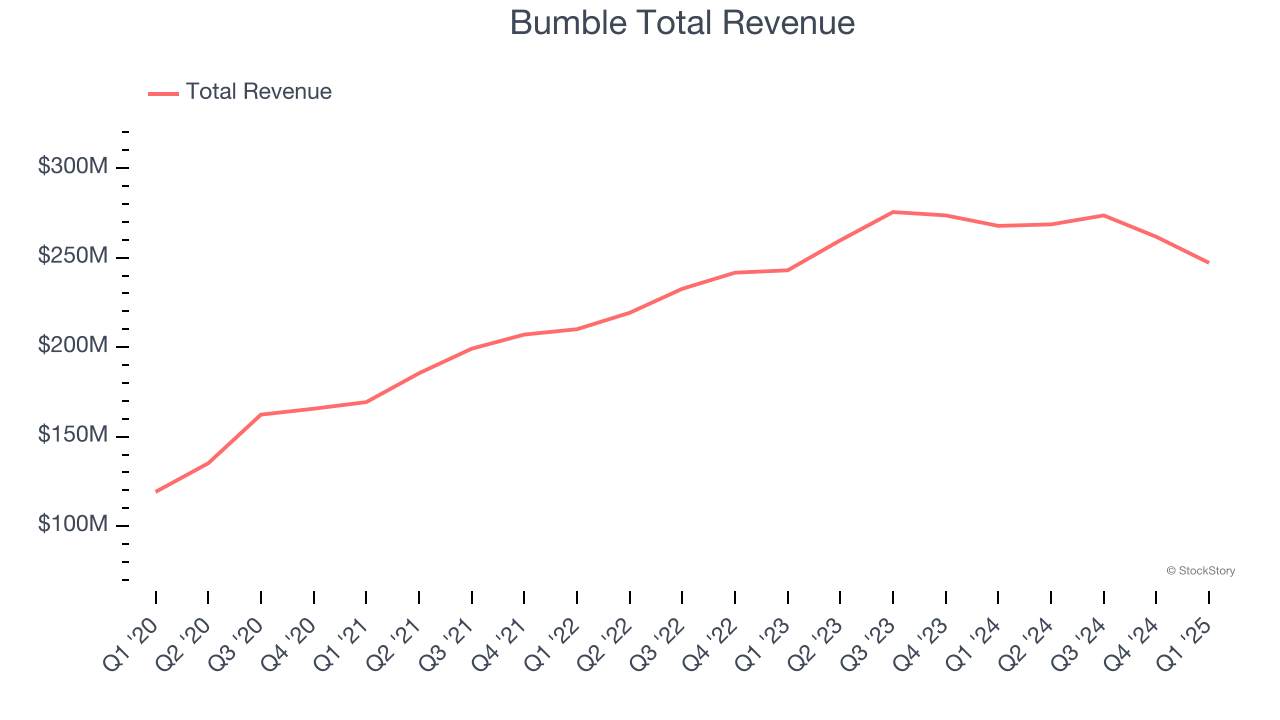

Started by the co-founder of Tinder, Whitney Wolfe Herd, Bumble (NASDAQ:BMBL) is a leading dating app built with women at the center.

Bumble reported revenues of $247.1 million, down 7.7% year on year. This print was in line with analysts’ expectations, and overall, it was a satisfactory quarter for the company with EBITDA guidance for next quarter exceeding analysts’ expectations.

“Since I returned in mid-March, we have set an accelerated path to return to sustainable, long-term growth,” said Whitney Wolfe Herd, Founder & CEO of Bumble Inc.

Bumble delivered the weakest performance against analyst estimates of the whole group. The company reported 4.01 million active buyers, down 0.2% year on year. Interestingly, the stock is up 30.3% since reporting and currently trades at $5.72.

Is now the time to buy Bumble? Access our full analysis of the earnings results here, it’s free.

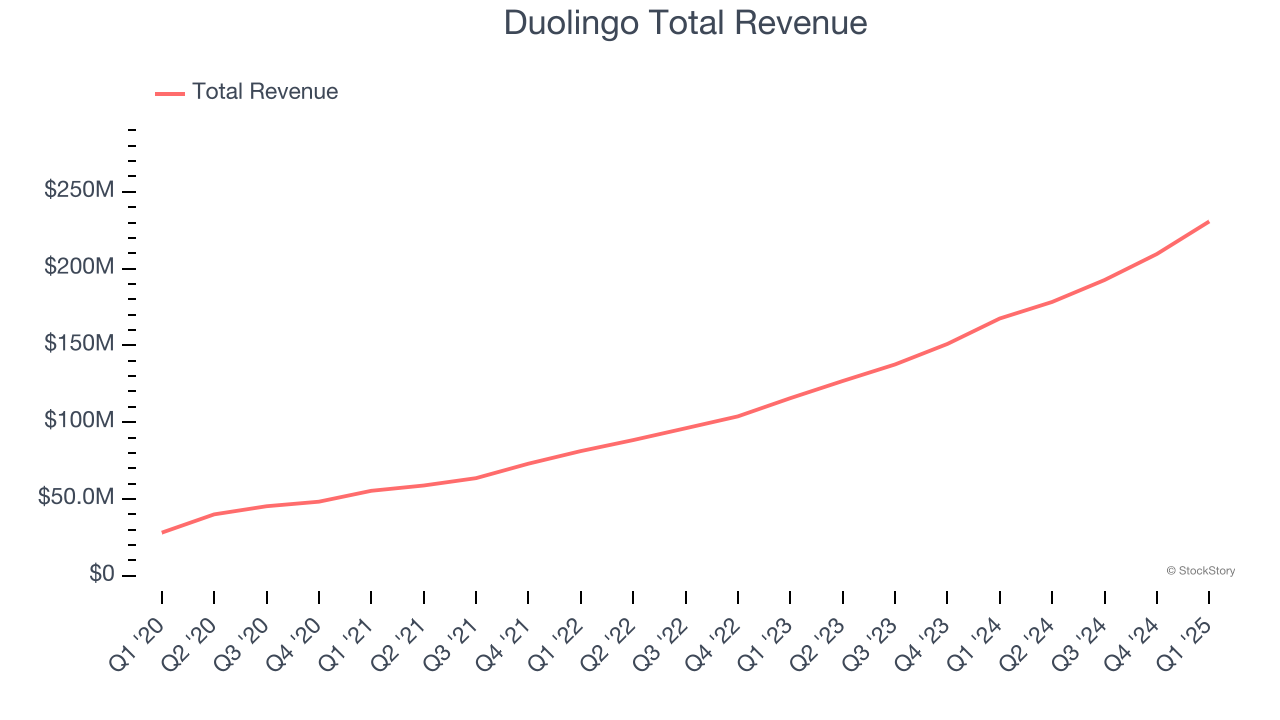

Founded by a Carnegie Mellon computer science professor and his Ph.D. student, Duolingo (NASDAQ:DUOL) is a mobile app helping people learn new languages.

Duolingo reported revenues of $230.7 million, up 37.7% year on year, outperforming analysts’ expectations by 3.4%. The business had a very strong quarter with an impressive beat of analysts’ EBITDA estimates.

Duolingo delivered the fastest revenue growth and highest full-year guidance raise among its peers. The company reported 130.2 million users, up 33.4% year on year. The market seems happy with the results as the stock is up 29.9% since reporting. It currently trades at $519.45.

Is now the time to buy Duolingo? Access our full analysis of the earnings results here, it’s free.

Spun out from Netflix, Roku (NASDAQ: ROKU) makes hardware players that offer access to various online streaming TV services.

Roku reported revenues of $1.02 billion, up 15.8% year on year, exceeding analysts’ expectations by 1.5%. Still, it was a slower quarter as it posted a slight miss of analysts’ number of total hours streamed estimates.

Interestingly, the stock is up 2.3% since the results and currently trades at $68.85.

Read our full analysis of Roku’s results here.

Started as a physical textbook rental service, Chegg (NYSE:CHGG) is now a digital platform addressing student pain points by providing study and academic assistance.

Chegg reported revenues of $121.4 million, down 30.4% year on year. This result topped analysts’ expectations by 5.8%. Aside from that, it was a mixed quarter as it also logged an impressive beat of analysts’ EBITDA estimates but a decline in its users.

Chegg delivered the biggest analyst estimates beat but had the slowest revenue growth among its peers. The company reported 3.19 million users, down 31.5% year on year. The stock is up 42.4% since reporting and currently trades at $0.97.

Read our full, actionable report on Chegg here, it’s free.

Founded by two Stanford University computer science professors, Coursera (NYSE:COUR) is an online learning platform that offers courses, specializations, and degrees from top universities and organizations around the world.

Coursera reported revenues of $179.3 million, up 6.1% year on year. This number surpassed analysts’ expectations by 2.3%. Overall, it was a strong quarter as it also logged EBITDA guidance for next quarter exceeding analysts’ expectations.

The company reported 175.3 million active customers, up 18% year on year. The stock is up 10.3% since reporting and currently trades at $8.47.

Read our full, actionable report on Coursera here, it’s free.

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

| Feb-12 | |

| Feb-10 | |

| Feb-03 | |

| Feb-03 | |

| Jan-27 | |

| Jan-14 | |

| Jan-13 | |

| Jan-12 | |

| Jan-06 | |

| Jan-05 | |

| Jan-04 | |

| Dec-30 | |

| Dec-28 | |

| Dec-26 | |

| Dec-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite