|

|

|

|

|||||

|

|

|

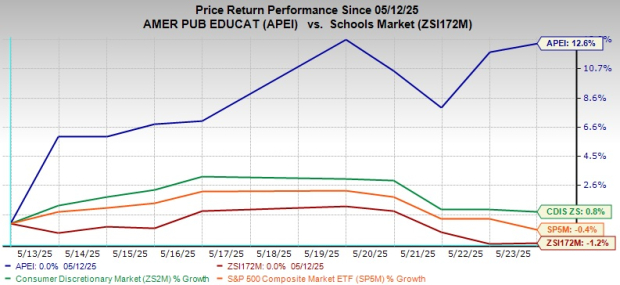

American Public Education, Inc.’s APEI shares have moved up 12.6% since it released its first-quarter 2025 results on May 12, 2025, significantly outperforming the Zacks Schools industry, the broader Zacks Consumer Discretionary sector and the S&P 500 Index. The detailed price performance is shown in the chart below.

The reported quarter’s adjusted earnings and total revenues topped the Zacks Consensus Estimate and grew year over year. Owing to the quarterly results and the favorable market trends, the company laid out an upbeat second-quarter 2025 outlook, with the 2025 full-year view indicating year-over-year growth. (read more: APEI Q1 Earnings & Revenues Beat Estimates, Both Up Y/Y, Stock Gains)

Notably, so far this year, APEI grew 35.9%, outperforming some of the other industry players, namely Laureate Education, Inc. LAUR, Grand Canyon Education, Inc. LOPE and Strategic Education, Inc. STRA. During the said time frame, shares of Laureate and Grand Canyon grew 19.4% and 18.5%, respectively, while Strategic Education tumbled 6.4%.

Diversified Product Offerings: American Public’s growth momentum lies in its focus on diversified educational offerings and keeping the offerings updated per the market's latest trends, to prepare its students with a real-world experience. It strives to be the best in what it does by providing higher education to working adults, including the military service members, veterans, nurses and other professionals.

Through technological transformation, the company consistently engages in increasing demand for online offerings and the utilization of technology to enhance student learning, and increasing use of Artificial Intelligence technologies. Currently, the market demand for post-secondary education is elevated, especially for an online alternative, which runs in favor of APEI. Underlying these strong market trends, the company aims to continue offering accessible and affordable higher education and training programs across a diverse range of subjects.

Robust Enrollment Trends: American Public has been registering impressive enrollment growth across its top revenue-contributing segments, American Public University System (APUS) and Hondros College of Nursing (HCN). Although Rasmussen University (RU) had a setback in 2024, it bounced back in 2025. The uptick in HCN and RU segments is fostered by the growing demand for nursing and other clinical roles in the health care ecosystem in the United States. Besides, APUS continues to get support from the continued strength in military and growing enrollments from veterans and military-affiliated families.

During the first quarter of 2025, the APUS segment’s net course registrations grew 3.5% year over year, with enrollment growth in the HCN and RU segments being 9.6% and 7.4%, respectively.

Strategic Optimization Efforts: American Public has undertaken several initiatives to address increasing cost pressure, with the most recent initiative being the combination of APUS, HCN and RU segments as one. In January 2025, this education provider announced a strategic move that supposedly will help it realize revenues and cost synergies over the long term. It aims to combine the three degree-granting institutions, APUS, RU and HCN, into a single consolidated institution, offering simpler operations. APEI believes that by combining and expanding its nursing campus footprint, it will have the ability to address the growing demand in the healthcare system of the country. Furthermore, offering RU’s programs at HCN’s campuses will accelerate growth and profitability in the long term.

This strategic move is expected to be complete by 2025-end, upon the completion of all regulatory and accreditation steps. APEI believes that by strategically working on optimizing its costs and maintaining a healthy balance sheet, it can increase its earnings growth in 2025 and beyond.

Solid Q2 & 2025 Outlook: After witnessing robust trends throughout 2024, followed by top-line growth in the first quarter of 2025, backed by increased registrations, enrollments and favorable tuition and fee increases, American Public laid out an upbeat second-quarter view and raised its 2025 outlook, boosting investors’ sentiments. For the second quarter, it expects total revenues to increase 4-5% year over year to $160-$162 million, with APUS’ total net course registrations reflecting growth between 4% and 7% and HCN’s total to increase about 14%. Also, it expects RU’s student enrollment to be up 8% year over year, including on-ground healthcare enrollment increasing 3% to 6,400 and online enrollment rising 12% year over year to 8,300.

For 2025, APEI expects total revenues to grow 4-6% year over year to $650-$660 million. Adjusted EBITDA is now expected to be between $77 million and $87 million (up from the prior projected band of $75-$85 million), reflecting 7-20% growth year over year.

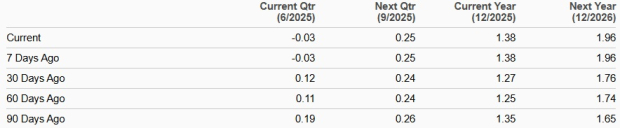

Backed by its in-house initiatives and favorable enrollment trends mentioned above, despite the lingering macro headwinds and regulatory hurdles, the earnings estimate trend for 2025 and 2026 has moved up in the past 30 days, indicating bullish sentiments amongst the analysts. The earnings estimate for 2025 and 2026 indicates 150.9% and 42% year-over-year growth.

EPS Estimate Revision

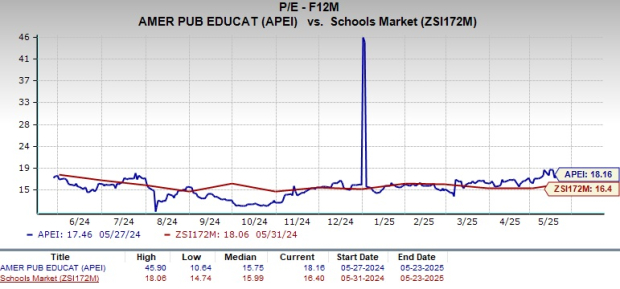

American Public is currently trading at a premium compared with the industry peers on a forward 12-month price-to-earnings (P/E) ratio basis. The premium valuation indicates that the stock is trading above its industry peers, making it difficult for investors to figure out a suitable entry point.

However, the overvaluation of APEI stock compared with its industry peers indicates its strong potential in the market, given the favorable trends backing it up. This trend justifies its valuation, validating its Value Score of A.

Per the discussion above, APEI’s performance is benefiting from the ongoing demand strength for nursing and other healthcare professionals. Furthermore, its diversified product offerings, digital penetration and marketing efforts are bearing fruit amid the market trends, reflecting increased contributions from its APUS, HCN and RU segments. The bounce back of the RU segment in the first quarter of 2025, in terms of enrollment and top-line growth, stands as an example of the underlying market’s strength, thus favoring the company as a whole.

Although the elevated inflationary scenario and other macro risks seem to be continuously taking a toll on the company, keeping it on its toes regarding cost management, its strategic efforts to counter the increasing costs and expenses are boding well.

Thus, after weighing both sides of the market scenario and considering APEI’s growth efforts, investors can consider adding this Zacks Rank #2 (Buy) stock to their portfolio for now.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite