|

|

|

|

|||||

|

|

|

Earnings results often indicate what direction a company will take in the months ahead. With Q1 behind us, let’s have a look at Northrop Grumman (NYSE:NOC) and its peers.

Defense contractors typically require technical expertise and government clearance. Companies in this sector can also enjoy long-term contracts with government bodies, leading to more predictable revenues. Combined, these factors create high barriers to entry and can lead to limited competition. Lately, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression towards Taiwan–highlight the need for defense spending. On the other hand, demand for these products can ebb and flow with defense budgets and even who is president, as different administrations can have vastly different ideas of how to allocate federal funds.

The 13 defense contractors stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 1.6% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 1.5% on average since the latest earnings results.

Responsible for the development of the first stealth bomber, Northrop Grumman (NYSE:NOC) specializes in providing aerospace, defense, and security solutions for various industry applications.

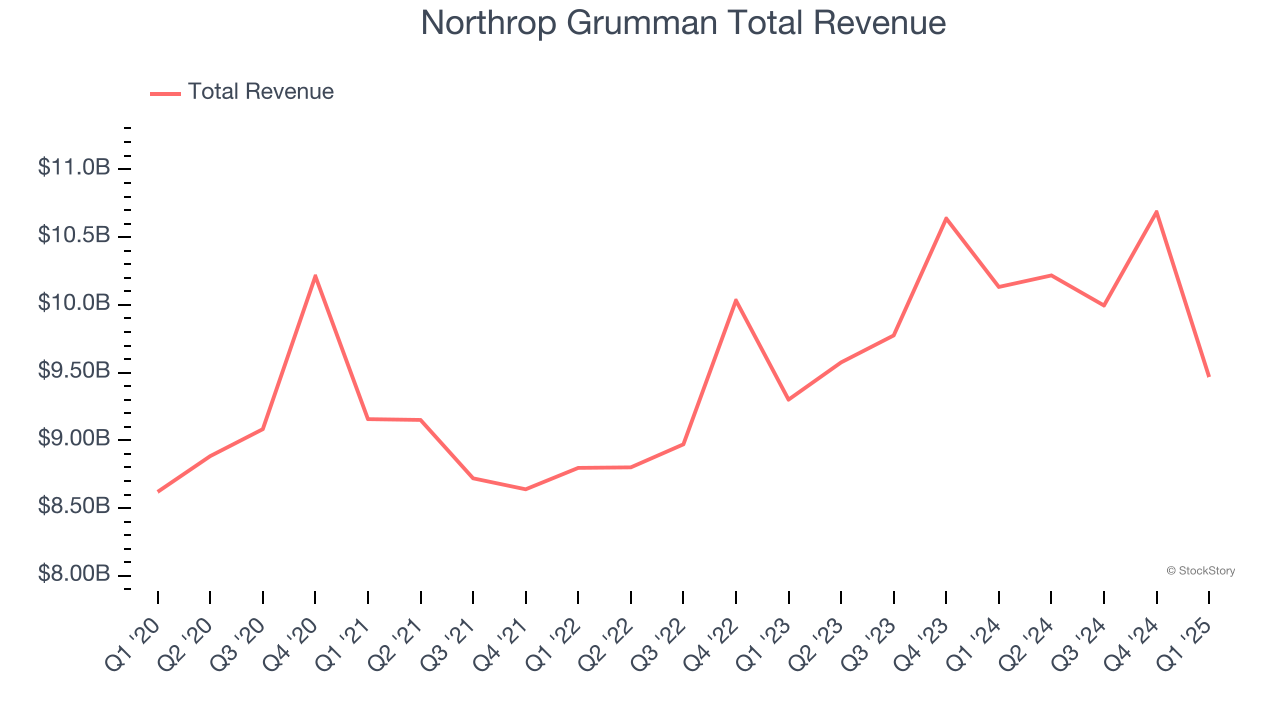

Northrop Grumman reported revenues of $9.47 billion, down 6.6% year on year. This print fell short of analysts’ expectations by 4.7%. Overall, it was a disappointing quarter for the company with full-year EPS guidance missing analysts’ expectations.

Northrop Grumman delivered the weakest performance against analyst estimates and slowest revenue growth of the whole group. The stock is down 9.9% since reporting and currently trades at $478.25.

Read our full report on Northrop Grumman here, it’s free.

Formed through the split of IT services company SAIC, Leidos (NYSE:LDOS) offers technology and engineering solutions such as military training systems for the defense, civil, and health markets.

Leidos reported revenues of $4.25 billion, up 6.8% year on year, outperforming analysts’ expectations by 3.6%. The business had a very strong quarter with an impressive beat of analysts’ backlog and EBITDA estimates.

However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $147.50.

Is now the time to buy Leidos? Access our full analysis of the earnings results here, it’s free.

Building Nimitz-class aircraft carriers used in active service, Huntington Ingalls (NYSE:HII) develops marine vessels and their mission systems and maintenance services.

Huntington Ingalls reported revenues of $2.73 billion, down 2.5% year on year, falling short of analysts’ expectations by 2.1%. It was a mixed quarter as it posted an impressive beat of analysts’ EPS estimates but a significant miss of analysts’ adjusted operating income estimates.

As expected, the stock is down 2.8% since the results and currently trades at $223.51.

Read our full analysis of Huntington Ingalls’s results here.

Known for projects like the construction of Guantanamo Bay, KBR provides professional services and technologies, specializing in engineering, construction, and government services sectors.

KBR reported revenues of $2.06 billion, up 13% year on year. This print lagged analysts' expectations by 1.4%. In spite of that, it was a strong quarter as it produced a solid beat of analysts’ EBITDA estimates.

The stock is up 1.2% since reporting and currently trades at $52.18.

Read our full, actionable report on KBR here, it’s free.

Developing submarine detection systems for the U.S. Navy, Leonardo DRS (NASDAQ:DRS) is a provider of defense systems, electronics, and military support services.

Leonardo DRS reported revenues of $799 million, up 16.1% year on year. This result surpassed analysts’ expectations by 9.2%. Overall, it was a very strong quarter as it also produced a solid beat of analysts’ adjusted operating income estimates and an impressive beat of analysts’ EPS estimates.

Leonardo DRS scored the biggest analyst estimates beat and fastest revenue growth among its peers. The stock is up 12.8% since reporting and currently trades at $41.68.

Read our full, actionable report on Leonardo DRS here, it’s free.

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

| 2 hours | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-22 | |

| Feb-20 |

Defense Funds Poised For Breakouts As Trump Readies Potential Iran Strike

NOC

Investor's Business Daily

|

| Feb-20 | |

| Feb-20 | |

| Feb-19 |

Boeing, Northrop Moving On Orders, Approvals; Plus Airbus' Engine Issue

NOC

Investor's Business Daily

|

| Feb-19 | |

| Feb-19 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite