|

|

|

|

|||||

|

|

|

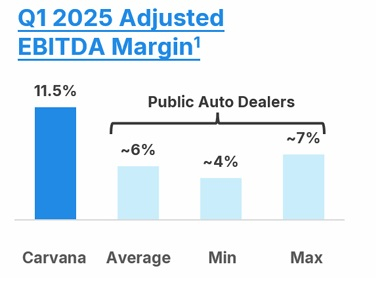

Carvana Co. CVNA achieved a record-breaking adjusted EBITDA of $488 million in the first quarter of 2025, which increased $253 million year over year. The company's adjusted EBITDA margin reached 11.5%, up 3.8 percentage points. This margin not only reflects operational efficiency but also leads the auto retail industry, nearly doubling the performance of many peers.

Carvana’s adjusted EBITDA quality is notably high when compared to other fast-growing companies due to its relatively low non-cash expenses. CVNA is also focusing on enhancing operational efficiency across the business, with several technology, process, and product initiatives underway.

Improvement in adjusted EBITDA margin compared to peers positions it well for long-term growth compared to many other high-growth technology companies.

In the second quarter, Carvana anticipates sequential growth in adjusted EBITDA and expects to set new company records. It expects significant growth in adjusted EBITDA in 2025 as well. Over the longer term, the company aims to reach adjusted EBITDA margins of 13.5% within the next five to ten years. Carvana sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

While CVNA is putting its best foot forward to improve margins, the road ahead for other auto retailers like Lithia Motors, Inc. LAD and AutoNation, Inc. AN looks bumpy as they struggle to maintain healthy margins.

Lithia reported an adjusted EBITDA margin of 4.4% in the first quarter of 2025 compared to 4% in the year-ago period. High tariffs could cause automakers and parts suppliers to raise prices, forcing Lithia to pass those higher costs on to customers. More expensive vehicles could discourage buyers, leading to lower sales volumes. To stay competitive, Lithia might need to offer discounts or incentives, which would pressure profit margins.

AutoNation had been operating below 60% selling, general and administrative (SG&A) as a percentage of gross profit in 2021 and 2022. However, in 2023 and 2024, its SG&A as a percentage of gross profit increased to 63.4% and 66.6%, respectively. The company’s degrading operational efficiency is worrisome. Adjusted SG&A was 67.5% of gross profit in the first quarter. The company expects SG&A as a percentage of gross profit in the band of 66-67% for the full year, which is likely to take a hit on its margin.

Carvana has outperformed the Zacks Internet-Commerce industry year to date. CVNA shares have surged 67.3% compared with the industry’s growth of 1.6%.

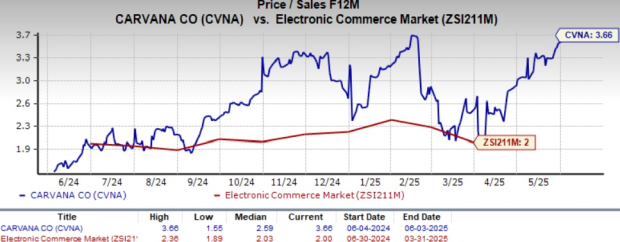

From a valuation perspective, Carvana appears overvalued. Going by its price/sales ratio, the company is trading at a forward sales multiple of 3.66, higher than its industry’s 2.

The Zacks Consensus Estimate for 2025 and 2026 EPS has moved up 83 cents each in the past 30 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-11 | |

| Mar-11 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-08 | |

| Mar-08 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite