|

|

|

|

|||||

|

|

|

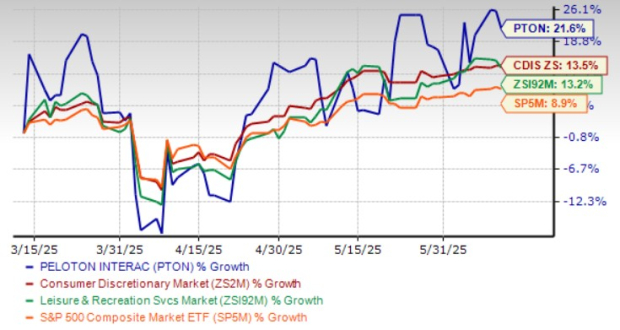

Shares of Peloton Interactive, Inc. PTON have gained 21.6% in the past three months compared with the Zacks Leisure and Recreation Products industry’s 13.2% growth. The stock has outperformed the Zacks Consumer Discretionary sector’s and the S&P 500’s rise of 13.5% and 8.9%, respectively.

Investor sentiment surrounding Peloton has turned more optimistic in recent weeks, supported by the company’s ongoing turnaround efforts and strategic focus on cost efficiency. The launch of its “Repowered” marketplace for refurbished bikes and treadmills has signaled a practical approach to addressing excess inventory while broadening its customer base, particularly among value-seeking consumers.

Investors appear encouraged by signs of improving margins and disciplined cost control, which have helped offset concerns about demand softness and competitive pressures. Additionally, clarity around minimal tariff exposure has further alleviated fears of supply chain disruption. The uptick in institutional interest and bullish options activity suggests rising confidence that Peloton’s recovery strategy may be taking hold.

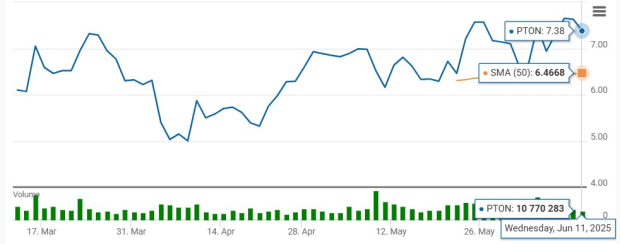

Currently, Peloton is trading 32.3% below its 52-week high of $10.90. So, should investors pour more capital into PTON shares now? Let’s take a closer look.

Peloton is showing meaningful signs of progress as it transitions from crisis management to a focused, profitability-driven recovery. The company continues to benefit from the stickiness of its connected fitness platform, with high-margin subscription revenues now contributing nearly 70% of total sales.

Subscription growth and retention continue to be pillars of Peloton’s turnaround. Despite broader macroeconomic headwinds and soft hardware sales, the company added 5,000 net Connected Fitness subscriptions during the fiscal third quarter and maintained a low churn rate of 1.2%. Enhanced personalization tools, such as the newly introduced Personalized Plans and strength-based content, have been instrumental in deepening member engagement. Peloton’s ability to maintain a loyal customer base reinforces the durability of its recurring revenue stream.

Peloton’s marketing discipline and renewed brand positioning are also beginning to bear fruit. The company’s “Find Your Power” campaign has expanded its appeal to a broader audience, especially male users, driving both higher attach rates for Tread sales and improved customer acquisition metrics. With marketing spend down 46% year over year and LTV-to-CAC improving by over 30%, Peloton is attracting new subscribers efficiently.

Strategic operational decisions are further reinforcing Peloton’s recovery narrative. The company is scaling new retail formats with strong early results, such as its high-performing micro-store in Nashville, and expanding through university partnerships and commercial installations via Precor. The initiatives likely support lower cost-per-acquisition while expanding brand presence across diverse channels.

Despite its recent operational improvements, Peloton continues to grapple with significant headwinds, particularly in its Connected Fitness hardware business. In the third quarter of fiscal 2025, hardware revenues declined 27% year over year, reflecting soft consumer demand for premium fitness equipment amid macroeconomic headwinds. Although initiatives like refurbished product offerings and equipment rentals aim to expand reach, they have yet to meaningfully offset losses from new hardware sales. This persistent weakness raises concerns, especially given Peloton’s historical reliance on hardware to drive initial subscriber acquisition.

Competitive pressure from digital fitness players like Apple Fitness+, Lululemon Studio, and free alternatives continues to mount, making subscriber growth increasingly difficult without significant innovation and marketing support.

Leadership transitions also cast a shadow over Peloton’s strategic direction. With multiple key executive roles still unfilled — including Chief Marketing Officer, Chief Communications Officer, and Chief Information Officer — the company is navigating critical brand repositioning and go-to-market changes without a fully staffed C-suite. As Peloton attempts to expand into new markets, relaunch its retail presence, and reposition its brand beyond cycling, these gaps in leadership may hinder effective execution and delay potential recovery.

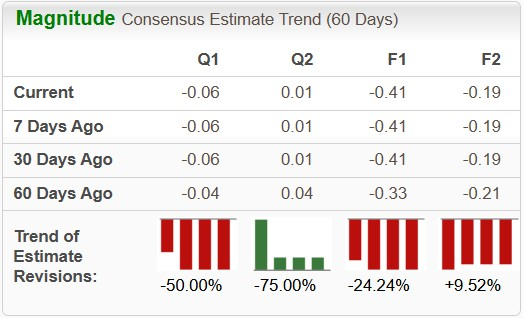

Peloton’s fiscal 2025 earnings per share (EPS) estimates have been revised downward, widening from a loss of 33 cents to a loss of 41 cents over the past 60 days. This downward trend reflects weakening analyst confidence in the stock’s near-term prospects.

Industry players like Planet Fitness, Inc. PLNT have increased their earnings estimates 0.3% in the past 60 days, while estimates for Xponential Fitness, Inc. XPOF have declined 50.6% in the same time frame. Meanwhile, estimates for YETI Holdings, Inc.’s YETI earnings have declined 29.9% in the past 60 days.

Peloton stock is currently trading at a discount. WYY is currently trading at a forward 12-month price-to-sales (P/S) multiple of 1.18X, well below the industry average of 4.95X, reflecting an attractive investment opportunity. Then again, other industry players, such as Planet Fitness, Xponential Fitness and YETI Holdings, have P/S ratios of 6.29X, 1.29X and 1.35X, respectively.

From a technical perspective, PTON is currently trading above its 50-day moving average, indicating solid upward momentum and price stability.

Peloton has made tangible progress in reshaping its business through disciplined cost control, growing subscription revenue, and strategic efforts to expand distribution and enhance brand engagement. The company's ability to generate consistent free cash flow and improve customer acquisition efficiency reflects meaningful operational improvement. With a loyal subscriber base, expanding wellness offerings, and a clear push toward profitability, Peloton’s turnaround appears to be gaining traction.

However, challenges persist. Weakness in hardware sales, intensifying competitive pressures, and gaps in senior leadership pose risks to the company’s recovery momentum. The recent downward revision in earnings estimates further clouds the near-term outlook. While Peloton is trading at an attractive valuation and showing technical strength, uncertainty around execution and top-line growth warrants caution. Given the mixed picture, investors may find it prudent to hold existing positions rather than chase the recent rally.

Peloton currently has a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 15 hours | |

| Jul-15 | |

| Jul-15 | |

| Jul-11 | |

| Jun-25 | |

| Jun-25 | |

| Jun-23 | |

| Jun-23 | |

| Jun-18 | |

| Jun-05 | |

| Jun-05 | |

| Jun-05 | |

| Jun-03 | |

| Jun-03 | |

| May-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite