|

|

|

|

|||||

|

|

|

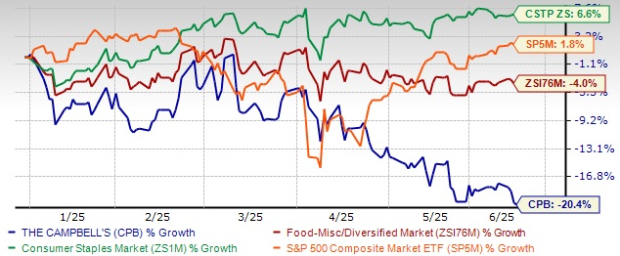

The Campbell's Company CPB has endured a challenging run in 2025, with its stock down 20.4% year to date. This sharp decline starkly contrasts with the broader market, underperforming the S&P 500’s modest 1.8% growth, the Zacks Consumer Staples sector’s 6.6% return. However, the industry’s average decline was just 4% during the same time frame.

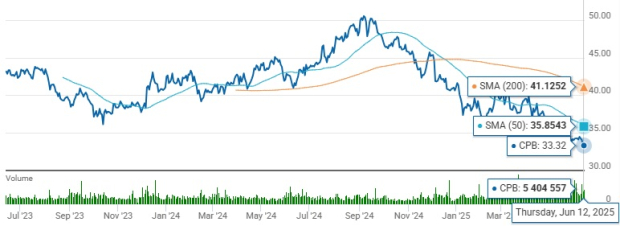

As of the last trading session, CPB closed at $33.32, just above its 52-week low of $32.83 reached on the same day. Notably, the stock is currently trading below both its 50-day and 200-day moving averages, reflecting ongoing weakness in momentum and investor sentiment.

These developments raise a critical question for investors: Is CPB’s slump a short-term correction due to temporary headwinds, or does it reflect deeper structural issues within the company?

Campbell's has been experiencing weaker-than-expected performance in the Snacks business amid shifting consumer trends and competitive dynamics within the market. The performance of its Snacks business was mixed in the third quarter of fiscal 2025, reflecting ongoing category softness and heightened competition within the snacking market. The macroeconomic environment remains dynamic and consumers are becoming increasingly deliberate with their spending, especially on discretionary snack items. Many are continuing to cook at home and prioritize food purchases that offer better value, which has supported growth in the Meals & Beverages segment but created headwinds for the Snacks category.

The trend continued in the fiscal third quarter, wherein net sales in the division totaled $1,012 million, down 8% year over year. Excluding the impact of the Pop Secret divestiture, organic net sales were down 5%. The decline was caused by a 5% drop in volume/mix, with net price realization remaining flat. Looking ahead, management expects the recovery in the Snacks business to be slower than initially anticipated.

In addition to sluggish snack sales, Campbell’s is grappling with persistent cost inflation. In the third quarter of fiscal 2025, the company faced cost inflation and related headwinds that weighed on its profitability. Its adjusted gross profit margin declined 110 bps to 30.1%, impacted by cost inflation, supply-chain expenses, unfavorable net pricing and acquisition-related impacts. In addition, CPB’s adjusted marketing and selling expenses rose 5% to $207 million in the fiscal third quarter, primarily due to the impact of the recent acquisition.

In its last earnings call, management highlighted that it expects core inflation to rise in the second half of the fiscal year — both year over year and sequentially — with full-year core inflation to stay in the low single-digit range. The company’s ability to balance inflationary pressures with its strategic goals will be critical in maintaining its trajectory toward growth.

Campbell’s has been operating in a dynamic environment. Reflecting its performance so far in fiscal 2025, the company recently reaffirmed its full-year guidance originally issued on March 5, 2025, excluding the impact of tariffs. However, adjusted earnings before interest and taxes (EBIT) and adjusted earnings per share (EPS) are now projected to be at the lower end of the guidance range, primarily due to a slower-than-expected recovery in the Snacks segment. CPB forecasts fiscal 2025 organic net sales to range from a 2% decline to flat year over year. Adjusted EBIT is estimated to grow 3-5%. The adjusted EPS is expected to decline 4-1%, in the range of $2.95-$3.05, compared with $3.08 reported in fiscal 2024.

Campbell’s is navigating a tough operating landscape in 2025. Pressures in its core Snacks business, inflation-driven margin erosion and a subdued earnings outlook have all contributed to the stock’s notable underperformance. With shares trading near 52-week lows and momentum indicators pointing to continued weakness, investors will be closely watching the company’s ability to execute a turnaround. At present, CPB carries a Zacks Rank #5 (Strong Sell).

Nomad Foods Limited NOMD manufactures, markets and distributes a range of frozen food products in the United Kingdom and internationally. It currently sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Nomad Foods' current fiscal-year sales and earnings implies growth of 4.6% and 7.3%, respectively, from the prior-year levels. NOMD delivered a trailing four-quarter earnings surprise of 3.2%, on average.

BRF S.A. BRFS raises, produces and slaughters poultry and pork for the processing, production and sale of fresh meat, processed products, pasta, margarine, pet food and other products. It currently carries a Zacks Rank of 2 (Buy). BRFS delivered a trailing four-quarter earnings surprise of 5.4%, on average.

The Zacks Consensus Estimate for BRF S.A.'s current fiscal-year earnings implies growth of 11.1%, respectively, from the prior-year levels.

Oatly Group AB OTLY, an oatmilk company, provides a range of plant-based dairy products made from oats. It presently carries a Zacks Rank of 2. OTLY delivered a trailing four-quarter earnings surprise of 25.1%, on average.

The consensus estimate for Oatly Group’s current fiscal-year sales and earnings implies growth of 2.7% and 65.8%, respectively, from the year-ago figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-14 | |

| Jun-24 | |

| Jun-23 | |

| Jun-23 | |

| Jun-17 | |

| Jun-17 | |

| Jun-16 | |

| Jun-16 | |

| Jun-10 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite