|

|

|

|

|||||

|

|

|

Medical Properties Trust, Inc. MPW — also known as MPT — and Praemia REIM announced that its 50/50 joint venture (“JV”) has refinanced its maturing seven-year debt agreement at a 5.1% fixed rate.

This €702.5 million debt, which is non-recourse and spans a duration of 10 years without amortization, is secured by a portfolio of German rehabilitation hospitals run/operated by MEDIAN, recognized as the largest operator of rehabilitation hospitals across Europe.

The primary purpose of the newly secured loan is to fund the repayment of the €655 million secured loan that was arranged during the JV formation in 2018.

The increased size of the new financing amount indicates a rise in the underwritten value of the facilities over the previous seven years, rather than a rise in the loan-to-value ratio. Importantly, since its formation, the annual cash rent generated by the JV has grown by approximately €20 million, which is roughly equivalent to the expected rise in market interest expense from the new loan.

Per Edward K. Aldag, Jr., chairman, president and CEO of MPT, “Given the tremendous market demand for MPT’s hospital real estate from sophisticated institutional investors, we continue to benefit from access to low-cost capital. This transaction, along with others recently executed, reinforces the value of $15 billion in hospital real estate around the world, the importance of our CPI-linked rent escalators as a natural hedge against inflation, and our confidence in the balance sheet flexibility available to us moving forward.”

This refinancing offers Medical Properties enhanced financial flexibility. The extended maturities of the assumed debt will help the company improve its maturity profile and enjoy greater liquidity for day-to-day operations.

MPW has been making efforts to enhance its liquidity position and alleviate bottom-line pressure. Further, it focuses on strengthening its balance sheet position. As of May 7, 2025, the company had approximately $1.3 billion of liquidity, including cash on hand and availability under its $1.28 billion revolving credit facility.

Its access to diverse capital sources through capital recycling and internal cash flow provides ample financial flexibility and is likely to support its growth endeavors.

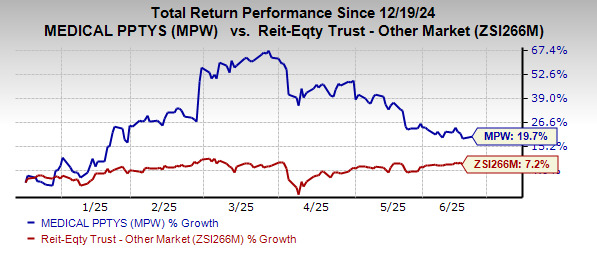

In the past six months, shares of this Zacks Rank #2 (Buy) company have gained 19.7% compared with the industry's upside of 7.2%.

Some other top-ranked stocks from the broader REIT sector are VICI Properties VICI and W.P. Carey WPC, each carrying a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for VICI’s 2025 FFO per share has moved one cent northward to $2.34 over the past two months.

The consensus estimate for WPC’s 2025 FFO per share has increased 1% to $4.88 over the past two months.

Note: Anything related to earnings presented in this write-up represents FFO, a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-12 | |

| Mar-12 | |

| Mar-11 | |

| Mar-11 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 | |

| Mar-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite