|

|

|

|

|||||

|

|

|

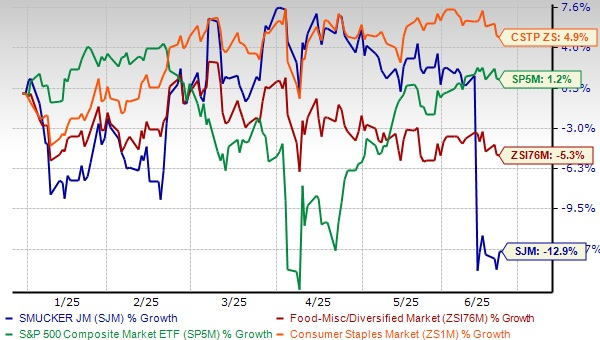

The J. M. Smucker Company SJM has endured a challenging run in 2025, with its stock down almost 13% year to date. This decline starkly contrasts with the S&P 500’s modest 1.2% gain and the Zacks Consumer Staples sector’s 4.9% growth. However, the industry’s average decline was just 5.3% during the same time frame.

As of the last trading session, SJM closed at $95.96, just above its 52-week low of $93.30 reached on the same day. Notably, the stock is currently trading below both its 50-day and 200-day moving averages, reflecting ongoing weakness in momentum and investor sentiment.

These developments raise a critical question for investors: Is SJM’s slump a short-term correction due to temporary headwinds, or does it reflect deeper structural issues within the company?

The J.M. Smucker stock has been under pressure due to persistent headwinds across several key business segments amid a tough operating landscape. One of the major drags has been its U.S. Retail Pet Foods segment, where net sales declined 13% year over year. This was largely due to retailer inventory adjustments, a drop in contract manufacturing sales related to divested brands and reduced demand in the dog snacks category.

Measured retail sales for dog snacks fell 7%, impacted by inflation-driven cutbacks in discretionary pet spending. The volume/mix had an 11-percentage-point adverse impact on net sales, while net price realization decreased the metric by 2 percentage points.

In addition, the Sweet Baked Snacks segment reported a sharp 26% decline in net sales and a 14% drop in comparable net sales during the fiscal fourth quarter. This was caused by a 9-percentage-point drop from unfavorable volume/mix — particularly in snack cakes, donuts and private label offerings — and a 4-percentage-point decline from lower net pricing across the portfolio. Segment profit fell sharply by 72%, reflecting the full impact of elevated input costs, weakened pricing power and continued volume softness.

Looking ahead to fiscal 2026, management expects comparable net sales in the Sweet Baked Snacks segment to decline in the low single digits, signaling continued challenges in consumer demand and pricing dynamics.

The J.M. Smucker continues to grapple with gross margin pressure as it navigates elevated costs and ongoing volume challenges. In the fourth quarter of fiscal 2025, the company reported a 9% year-over-year decline in adjusted gross profit, primarily due to elevated costs, an unfavorable product mix and volume, and the noncomparable impact of recent divestitures. Adjusted operating income also declined by 8%, reflecting the drop in gross profit.

Looking ahead, management expects the fiscal 2026 adjusted gross profit margin to range between 35.5% and 36%. This forecast reflects elevated commodity and manufacturing costs and negative volume/mix. Management also highlighted a roughly 50 basis point (bps) unfavorable impact from tariffs — most notably affecting the U.S. Retail Coffee segment — as a factor contributing to the margin outlook.

Compounding the margin challenges, The J.M. Smucker expects its selling, distribution and administrative (SD&A) expenses to rise approximately 3% year over year in fiscal 2026. The increase is primarily caused by elevated marketing investments aimed at supporting key growth brands. Total marketing spend is projected to reach 5.7% of net sales, up 30 bps from the prior year. While these investments are intended to fuel long-term growth, they contribute to near-term cost headwinds as The J. M. Smucker navigates a dynamic operating environment.

The J. M. Smucker continues to navigate a complex and rapidly evolving external environment, marked by ongoing tariff impacts, regulatory changes, persistent input cost inflation and shifting consumer behaviors — all of which are shaping its fiscal 2026 outlook. For the first quarter of fiscal 2026, management anticipates a low-single-digit decline in reported net sales.

On a comparable basis, net sales are expected to remain flat, with mid-single-digit pricing gains offset by unfavorable volume and mix dynamics. The adjusted earnings per share (EPS) are projected to decline approximately 25% in the fiscal first quarter due to decreased gross profit in the U.S. Retail Coffee and Sweet Baked Snacks segments.

These near-term headwinds underscore the complexity of the Zacks Rank #4 (Sell) company. Investors may want to stay cautious until clearer signs of recovery emerge.

Nomad Foods Limited NOMD manufactures, markets and distributes a range of frozen food products in the United Kingdom and internationally. It currently sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Nomad Foods' current fiscal-year sales and earnings implies growth of 4.6% and 7.3%, respectively, from the prior-year levels. NOMD delivered a trailing four-quarter earnings surprise of 3.2%, on average.

BRF S.A. BRFS raises, produces and slaughters poultry and pork for the processing, production and sale of fresh meat, processed products, pasta, margarine, pet food and other products. It currently carries a Zacks Rank of 2 (Buy). BRFS delivered a trailing four-quarter earnings surprise of 5.4%, on average.

The Zacks Consensus Estimate for BRF S.A.'s current fiscal-year earnings implies growth of 11.1%, respectively, from the prior-year levels.

Oatly Group AB OTLY, an oatmilk company, provides a range of plant-based dairy products made from oats. It presently carries a Zacks Rank of 2. OTLY delivered a trailing four-quarter earnings surprise of 25.1%, on average.

The consensus estimate for Oatly Group’s current fiscal-year sales and earnings implies growth of 2.3% and 63.8%, respectively, from the year-ago figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-15 | |

| Jul-09 | |

| Jul-07 | |

| Jun-28 | |

| Jun-25 | |

| Jun-24 | |

| Jun-17 | |

| Jun-09 |

The Corners of the Market Where Investors Are Riding Out Turbulence in Chip Stocks

SJM +10.44%

The Wall Street Journal

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite